DEEP RESEARCH · HanAll Biopharma

HanAll Biopharma: 2026 as the FcRn Data Year for a Global Biopharma Shift

A review of batoclimab, IMVT-1402, tanfanercept, the Osong capex cancellation, and 2026 clinical catalysts.

0. Bottom line first

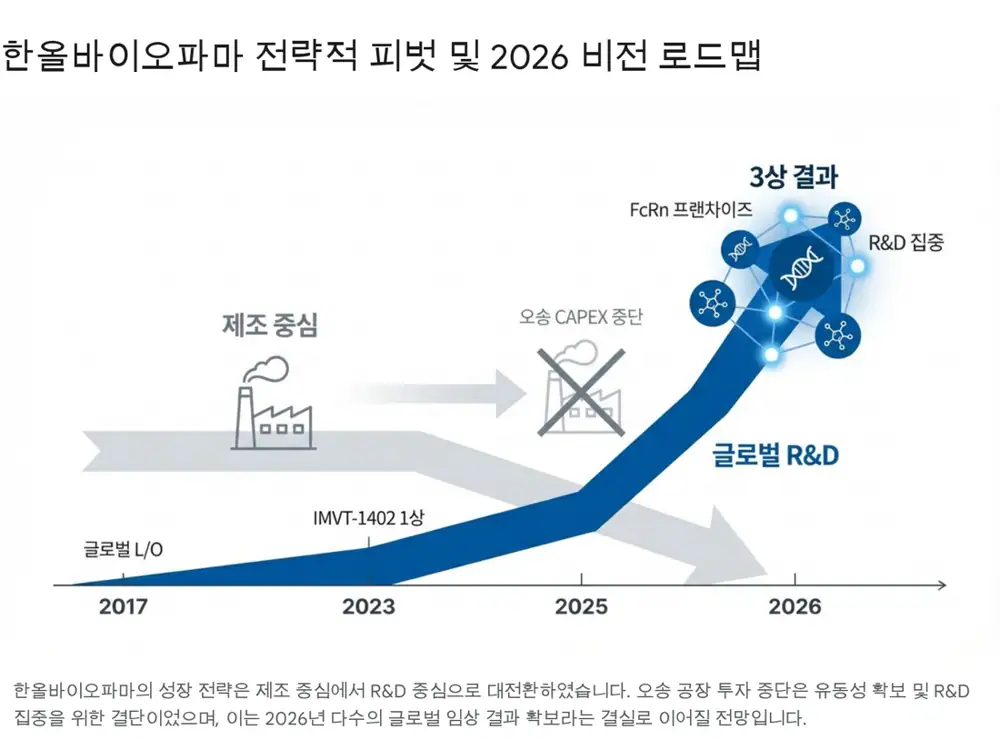

The source thesis is that 2026 is not just another fiscal year for HanAll Biopharma, but a harvest year in which FcRn pipeline data and global clinical execution could drive a fundamental valuation rerating.

Official fact: The source says HanAll is shifting from a generics and improved-drug pharma model into a biotech model centered on innovative pipelines and global partnerships.

Interpretation: The key items for me are batoclimab’s TED phase 3, IMVT-1402 data in difficult-to-treat rheumatoid arthritis and CLE, tanfanercept VELOS-4, and the capital-allocation flexibility created by stopping the Osong plant investment.

1. FcRn inhibitors: third-generation therapy that lowers autoantibodies directly

The autoimmune-therapy market is moving from first-generation steroids and nonspecific immunosuppressants, through second-generation biologics such as TNF-alpha inhibitors, into third-generation FcRn inhibitors that directly remove pathogenic autoantibodies.

Official fact: The source says the main indications targeted by FcRn inhibitors are expected to reach about USD 30bn, roughly KRW 40tn, by 2030. MG and CIDP alone are presented as about USD 10bn, roughly KRW 13tn, by 2030.

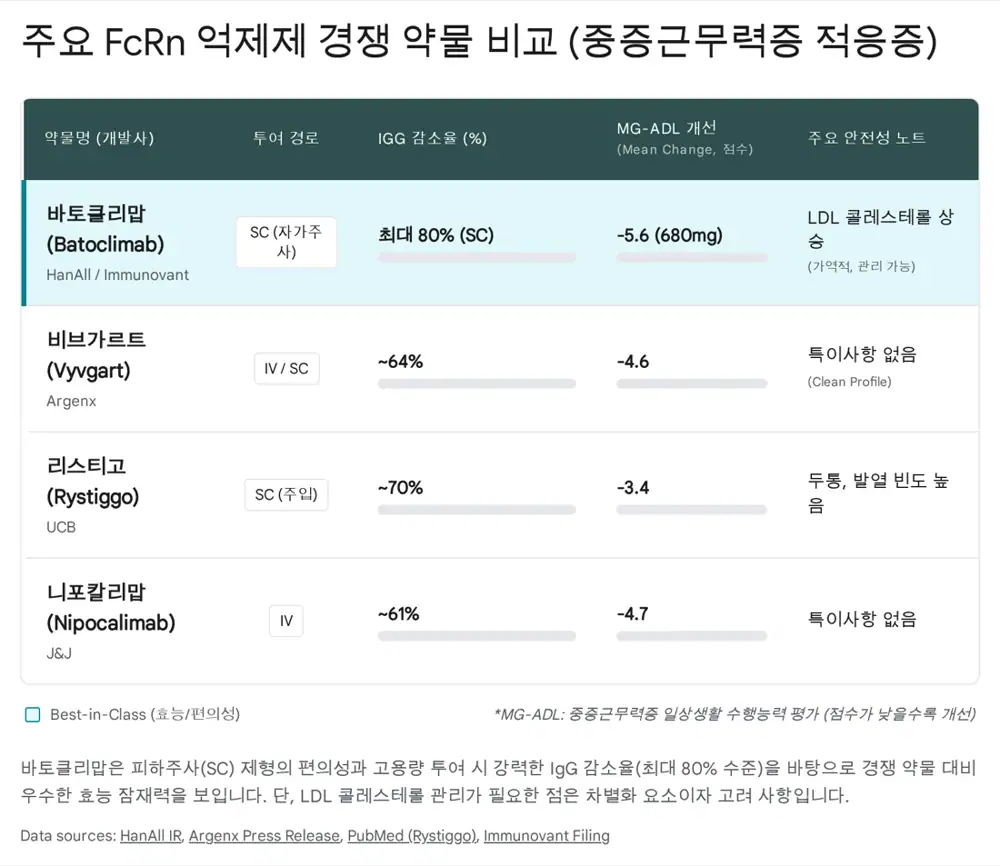

2. Competitive landscape and HanAll’s two-track strategy

| Drug/company | Source content | What to watch |

|---|---|---|

| Vyvgart / Argenx | First approved as IV, then added SC; about 60-70% IgG reduction | Market standard, but convenience and off-target issues leave room for improvement |

| Nipocalimab / J&J | FDA approval in May 2025, mainly dependent on IV-formulation data | Patient convenience and albumin-reduction concerns |

| Rystiggo / UCB | SC formulation, with relatively high headache and fever adverse-event frequency reported | Safety-profile competition |

| Batoclimab | Strong IgG reduction and SC self-administration convenience | Initial focus on severe and acute rare autoimmune diseases |

| IMVT-1402 | Next-generation molecule aiming to preserve efficacy while reducing albumin and LDL issues | Targets long-term chronic markets such as RA, GD, and CLE |

Batoclimab

The source frames it as a first wave for rare autoimmune diseases such as MG and TED, with up to roughly 80% IgG reduction and SC convenience.

Imeroprubart

IMVT-1402 is presented as a Best-in-Class candidate intended to keep batoclimab-like efficacy while reducing albumin binding and LDL cholesterol elevation.

Indication optimization

The core strategy is not relying on one asset for every disease, but splitting severe diseases and chronic long-term dosing markets.

3. Capital allocation: meaning of the Osong plant cancellation

Official fact: On December 19, 2025, HanAll disclosed that it would stop the Osong specialized plant construction investment. The source says the original KRW 41.7bn plan was reduced to KRW 4.3bn already spent on Shintanjin plant upgrades, with the remaining plan cancelled.

Interpretation: This cuts manufacturing capex and concentrates resources on global clinical development and new pipelines. By avoiding roughly KRW 37.4bn of remaining capex, the source argues HanAll preserves funding for 2026 phase 3 costs and next-generation pipeline acquisition.

4. Pipeline deep dive

| Pipeline | Source figure/fact | Meaning |

|---|---|---|

| Batoclimab | In MG phase 3, the 680mg high-dose SC group improved MG-ADL by an average of 5.6 points | The source emphasizes competitiveness versus Rystiggo’s MG-ADL improvement of -3.4 points. |

| Batoclimab | High-dose IgG reduction approached 80%; LDL elevation is reversible and management data with statins are accumulating | The logic is strong efficacy for refractory and severe patients. |

| IMVT-1402 | Phase 1 showed batoclimab-like IgG reduction with no observed albumin reduction or LDL elevation | Core candidate for large indications such as RA that require long-term dosing. |

| Tanfanercept / HL036 | VELOS-3 missed primary CCSS/EDS endpoints but showed significant Schirmer’s test improvement with p=0.002 | The source says VELOS-4 is optimized to demonstrate Schirmer’s test improvement under FDA guidance. |

| HL192 | Parkinson’s disease collaboration with NurrOn Pharmaceuticals | Bridge beyond autoimmune disease into neurodegenerative disease. |

| Turn Biotechnologies | Introduced mRNA-based rejuvenation technology | Explores innovative therapeutics in ophthalmology and ENT. |

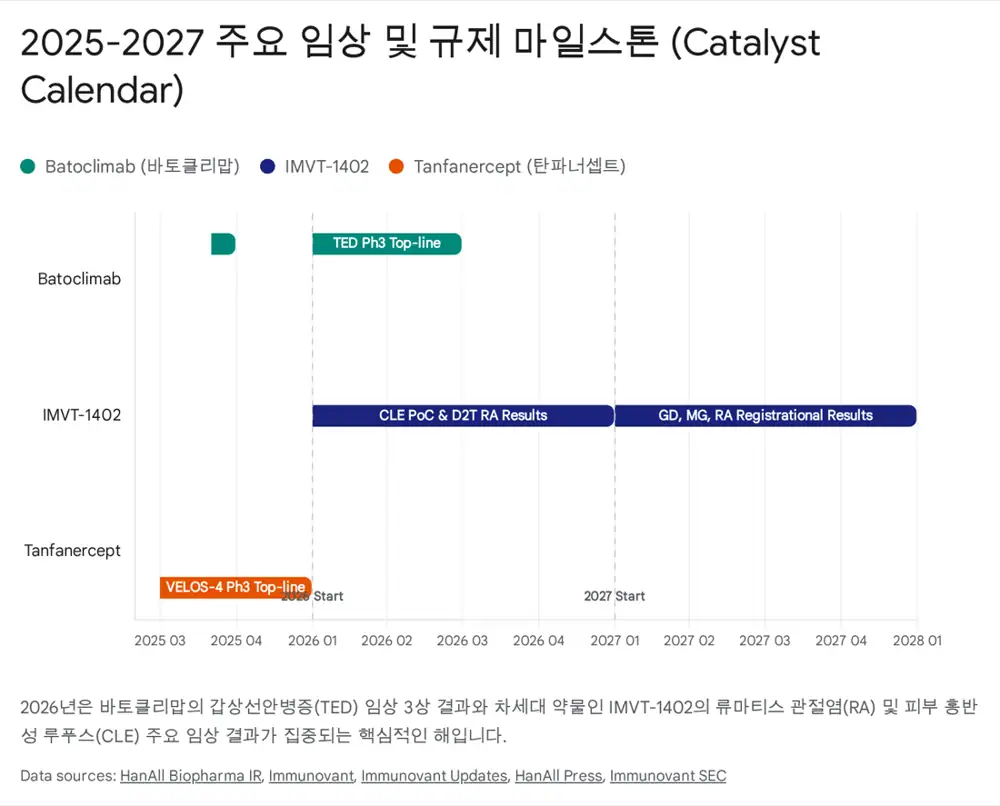

5. 2026 Catalyst Calendar

| Event | Expected timing | Background |

|---|---|---|

| Batoclimab TED phase 3 topline | First half 2026 | The source says two phase 3 studies are being analyzed together to improve data confidence and regulatory strategy. |

| IMVT-1402 difficult-to-treat RA phase 2/potential registrational data | 2026 | Efficacy in treatment-refractory RA would increase the chance of entering a major chronic disease market. |

| IMVT-1402 cutaneous lupus erythematosus PoC | 2026 | An event to test whether the FcRn mechanism can improve lupus skin symptoms. |

| Tanfanercept VELOS-4 | 2026 | Presented as a trial designed around the proportion of patients with at least 10mm Schirmer’s test improvement. |

Interpretation: 2026 is “high risk, high return.” Positive data could revalue HanAll from a technology-export company into a global immunology player, while weak TED or RA data could quickly compress expected value.

6. Financial position and risks

KRW 117.6bn Q3 2024 cumulative revenue

The source cites 14.7% year-over-year growth and KRW 1.1bn operating profit, with Normix, Eligard, and Biotop as cash cows.

No CB/BW balance

The source views the capital structure as clean, with no outstanding convertible bonds or bonds with warrants.

Harbour BioMed arbitration

HanAll filed ICC arbitration after judging that its partner did not use commercially reasonable efforts.

- Harbour BioMed risk: HanAll notified license termination and filed ICC arbitration after development delays in China. The source also views potential China-rights recovery and new partnering as an opportunity.

- Clinical-data volatility: Many clinical results are concentrated in 2026, so both positive and negative data can materially affect the stock.

- Competition: HanAll must compete with global pharma companies such as Argenx, J&J, and UCB, so IMVT-1402 needs to prove a Best-in-Class profile.

7. My conclusion

HanAll is a hybrid biotech with both existing-drug cash cows and an FcRn pipeline with global blockbuster potential. In 2026, data decides everything. If IMVT-1402 proves both safety and efficacy, the company can expand into long-term autoimmune markets; if it does not, expected value can adjust quickly.

Sources

- Source 1: Naver Blog original

- Source 2: Viridian Therapeutics 2024 Financial Results - SEC

- Source 3: FcRn Inhibitors in 20+ Indications

- Source 4: FcRn inhibitor market overview

- Source 5: Viridian Therapeutics Q1 2025 Financial Results

- Source 6: arGEN-X competitive landscape

- Source 7: Vyvgart market report

- Source 8: Immunovant phase 3 autoimmune article

- Source 9: Nipocalimab Vivacity-MG phase 2

- Source 10: Rozanolixizumab MycarinG phase 3

- Source 11: IMVT-1402 600 mg MAD results

- Source 12: IMVT-1402 phase 1 SAD and 300 mg MAD results

- Source 13: Immunovant $550 million offering and program updates

- Source 14: HanAll Q3 2024 results and business update

- Source 15: HanAll and Daewoong invest in Turn Biotechnologies

- Source 16: Batoclimab MG and CIDP study results

- Source 17: Immunovant 8-K filing

- Source 18: Nipocalimab Vivacity-MG3 phase 3

- Source 19: HanAll VELOS-4 phase 3 initiation

- Source 20: Immunovant Q2 FY2025 corporate updates

- Source 21: Immunovant SEC exhibit

- Source 22: Immunovant quarter ended June 30, 2025 update

- Source 23: HanAll Q3 2024 PR Newswire update

- Source 24: HanAll pulls plug on Harbour BioMed batoclimab deal

- Source 25: HL161 licensing agreement termination statement