DEEP RESEARCH · PEPTRON

Peptron: The 2026 Execution Roadmap for a Long-Acting Drug Platform

Lilly evaluation, Osong Plant 2, LeupONE, and the GLP-1 pipeline translated into 2026 KPIs.

0. Bottom line first

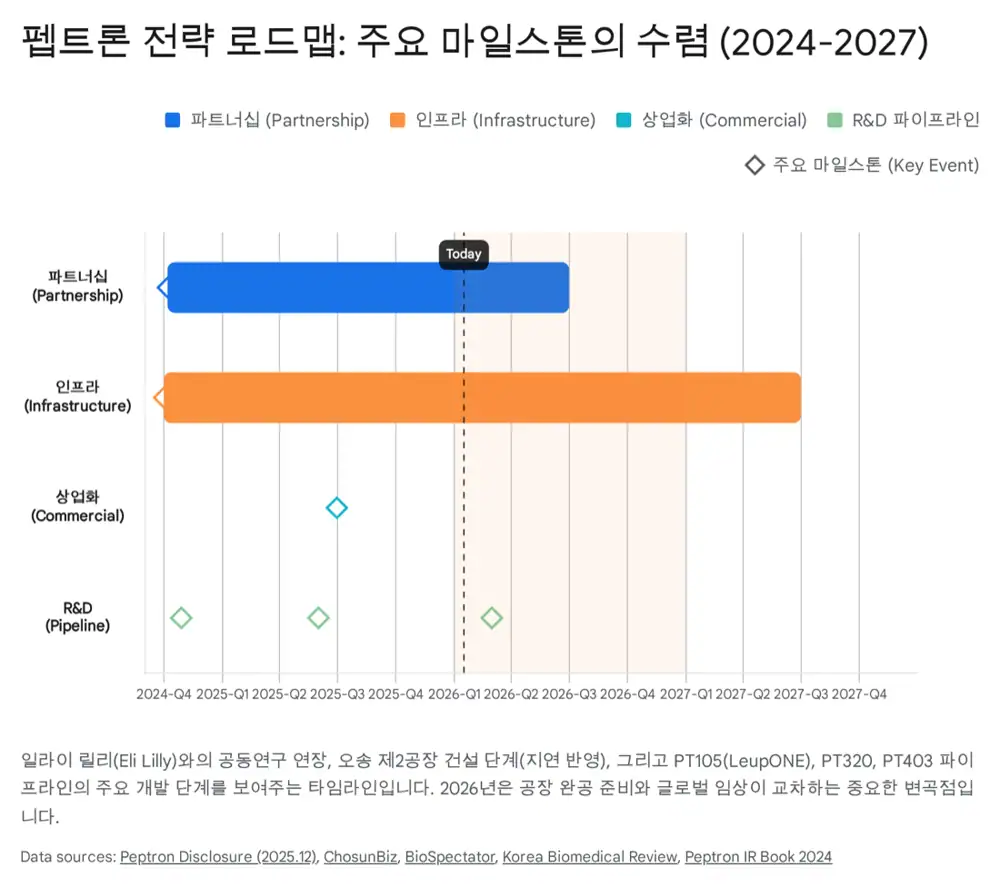

My view is that Peptron's 2026 question is whether it can move from R&D-oriented biotech venture to an industrialized long-acting drug platform company. Lilly evaluation, Osong Plant 2, LeupONE revenue, and PT403/404 clinical entry all need to point in the same direction.

Official fact: The source states that Peptron, founded in 1997, has developed the SmartDepot platform and frames 2026 as the year when the Eli Lilly partnership, Osong Plant 2, and LeupONE revenue contribution should start converting technology into corporate value.

Interpretation: If 2025 was about financing and IND preparation, 2026 is about execution. But the execution path is expensive. Without a main Lilly agreement and upfront payment, Osong CAPEX and PT403/404 clinical spending may remain a balance-sheet burden.

1. Eli Lilly evaluation: final validation in 2026

The source treats the platform evaluation contract with Eli Lilly as the most important variable for 2026 enterprise value. Signed in October 2024, the agreement tests SmartDepot technology with Lilly's peptide drugs to verify efficacy and stability.

Official fact: The evaluation period was initially expected to be about 14 months, but contract terms allow an extension to as long as 24 months. The source gives October 7, 2026 as the possible endpoint. Peptron and Lilly agreed to add in-vivo testing for a specific peptide SmartDepot formulation.

Interpretation: The extension is not just delay. It can be read as Lilly checking pharmacokinetics, immunogenicity, long-term dosing safety, initial-burst risk, and bioavailability more carefully before a commercial agreement. Success could convert a non-exclusive evaluation license into an exclusive commercial license for specific targets, with upfront and milestone payments changing the financial structure.

SmartDepot

The platform is being evaluated for converting weekly formulations into monthly or longer-acting formulations.

In-vivo expansion

After initial in-vitro work, the evaluation expands to biological PK and safety data.

Main agreement potential

The top 2026 strategic goal is a commercial license agreement.

2. Osong Plant 2: cGMP capacity built with KRW 89.0B

If the global partnership is the software, Osong Plant 2 is the hardware that supports it. The source says 2026 will be a peak construction and equipment-installation year rather than a full operating year.

Official fact: The Osong Plant 2 investment completion date changed from December 27, 2026 to June 30, 2027. Total investment increased from KRW 65.0B to KRW 89.0B, equal to 246.35% of Peptron's equity capital.

| Item | Before | After | Change | Note |

|---|---|---|---|---|

| Total investment | KRW 65.0B | KRW 89.0B | +KRW 24.0B | 246.35% of equity capital |

| Building construction | KRW 20.5B | KRW 44.5B | +KRW 24.0B | Design and GMP facility work included |

| Production equipment | KRW 44.5B | KRW 44.5B | - | Production and support equipment |

| Investment period | 2024.10~2026.12 | 2024.10~2027.06 | Six-month extension | Reflects construction-permit delay |

The investment is split between KRW 44.5B for building construction and KRW 44.5B for production equipment. The source highlights U.S. FDA cGMP design, advanced equipment such as ultrasonic spray dryers for long-acting drugs, annual capacity of 10M vials, and about 10 times the scale of Plant 1.

Interpretation: Plant 2 is not just capacity expansion. It is the gate from technology supplier to product supplier and potentially CDMO company. Global partners such as Lilly require stable supply of clinical samples and commercial products, so large-scale cGMP capacity matters.

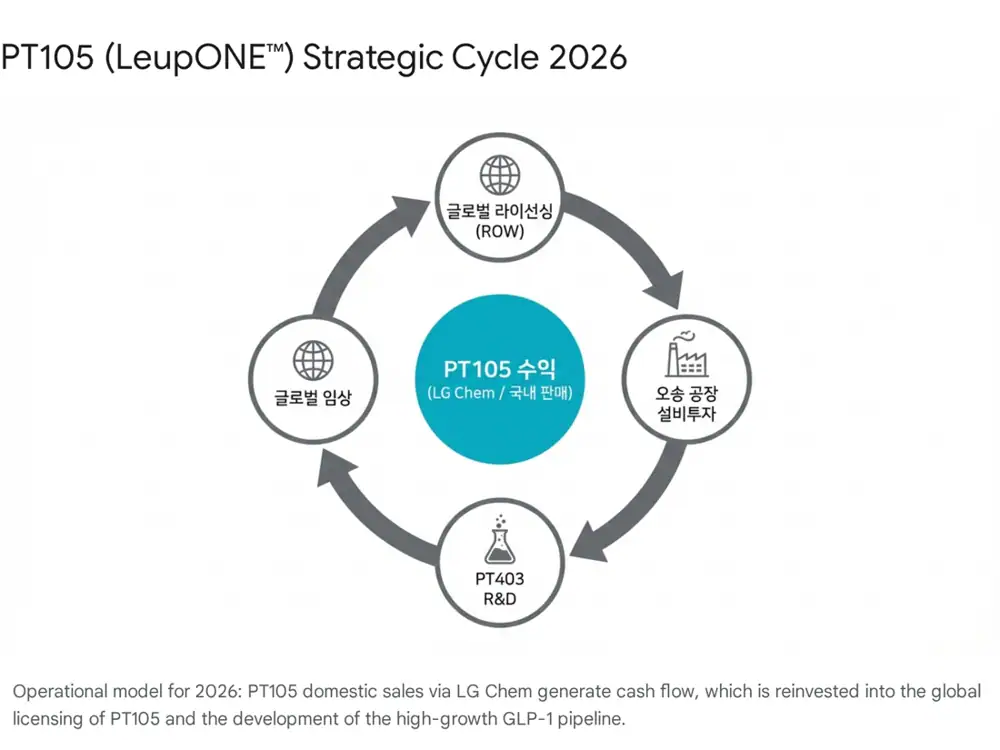

3. LeupONE: the commercial pipeline for current revenue

While future investment continues, the source identifies PT105, branded LeupONE, as the commercial pipeline responsible for near-term cash flow. It is a leuprorelin formulation for prostate cancer and precocious puberty.

Official fact: PT105 is described as a generic that established pharmacokinetic equivalence with Takeda's Leuplin. After Korean MFDS approval in July 2025, the source treats 2026 as the first year of full revenue generation. The domestic leuprorelin formulation market is estimated at more than KRW 80.0B.

- Peptron granted exclusive domestic rights to LG Chem, whose sales network is expected to support early adoption.

- SmartDepot technology is described as improving dosing convenience, including a thinner needle that reduces patient pain versus existing products.

- Overseas rights deals are planned for Europe and pharmerging markets, where the absence of an advanced-market-standard bioequivalent generic outside Japan is seen as an opportunity.

- The source says Peptron plans to accelerate candidate formulation development and preclinical work for PT105 3M, a three-month formulation, beyond the current one-month 3.75mg product.

4. R&D pipeline: GLP-1 and rare diseases

Monthly semaglutide

A monthly formulation based on semaglutide, the active ingredient of Wegovy. The source mentions a planned Korean Phase 1 IND in 2025 and Phase 1 execution in 2026.

Monthly tirzepatide

A candidate based on tirzepatide, the active ingredient of Zepbound. The source expects preclinical completion and clinical-entry preparation or possible Phase 1 work in 2026.

Rare-disease reset

After voluntarily withdrawing the Phase 1 IND for achondroplasia in 2024, Peptron plans to add preclinical data in 2026 and consider expansion to Noonan syndrome and other FGFR3-related rare diseases.

Interpretation: In the GLP-1 market, Peptron's weapon is dosing convenience. If weekly Wegovy and Zepbound can become monthly, annual injections fall from 52 to 12. But the technology-export case strengthens only if clinical data show comparable or better efficacy and safety.

5. Financial outlook and risks

Official fact: The source states that Peptron completed a roughly KRW 120.0B rights offering from late 2024 to early 2025 to fund Osong Plant 2 and clinical expenses.

| Financial variable | Source content | Investment read-through |

|---|---|---|

| CAPEX | Osong Plant 2 construction peaks in 2026 | Cash burn continues from remaining construction and equipment payments |

| Clinical cost | PT403/404 and related clinical spending | Without R&D results, cost burden remains |

| Revenue contribution | LeupONE and PeptrEX peptide-material revenue | May not be enough to offset large investment |

| Key variable | Upfront payment from a Lilly main agreement | The main financial-health fork |

Risk factors

- Construction delay: Further delay at Plant 2 could disrupt CDMO order activity and internal commercialization plans.

- Clinical data: Weak PT403/404 Phase 1 results or negative Lilly evaluation data could hit enterprise value directly.

- Cash burn: Early LeupONE revenue alone may not offset large CAPEX and clinical spending.

6. Final view

Interpretation: My conclusion is that Peptron must pass three KPIs at the same time to turn possibility into conviction in 2026: successful Lilly evaluation and a commercial license agreement in 2H 2026, steady Osong Plant 2 milestones toward 2027 completion, and LeupONE share gains plus successful PT403 clinical entry.

If these align, Peptron can connect lab-level technology to cGMP mass production and global drug markets. If the Lilly main agreement is delayed or clinical data disappoint, the large investment will show up first as financial burden.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224149341439

- CHOSUNBIZ: https://biz.chosun.com/en/en-finance/2025/11/28/OHDXJHFYTFBRZKM6VN6COQOYPU/

- CHOSUNBIZ: https://biz.chosun.com/en/en-finance/2025/12/02/B2DVV26BGBAFXFLAMQ6VECFLLI/

- MK: https://www.mk.co.kr/en/it/11335040

- University of Liverpool: https://www.liverpool.ac.uk/celt-global-health/global-news/stories/title,1485799,en.php

- Korea Biomedical Review: https://www.koreabiomed.com/news/articleView.html?idxno=29989

- CHOSUNBIZ: https://biz.chosun.com/en/en-science/2025/11/28/PABBEIAAAJFGNEWEQ2UJXBUC4Y/

- PR Newswire: https://www.prnewswire.com/news-releases/peptrons-pt105-a-sustained-release-leuprolide-established-the-bioequivalence-with-takedas-leuplin-301687409.html

- Chosunbiz: https://biz.chosun.com/science-chosun/bio/2025/07/15/6LTBXUMKURFKLABUCJBYXNJ7X4/

- Yakup: http://m.yakup.com/news/index.html?mode=view&pmode=&cat=&cat2=&nid=275758&num_start=840&csearch_word=%EC%8B%9D%EC%95%BD%EC%B2%98%20%EC%8A%B9%EC%9D%B8&csearch_type=news&cs_scope=

- BioSpace: https://www.biospace.com/peptron-s-pt105-a-sustained-release-leuprolide-established-the-bioequivalence-with-takeda-s-leuplin

- KRX KIND prospectus: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20241007000186&rcpno=20241007000053&orgid=F&tran=Y&langTpCd=0

- Mirae Asset Securities Pharma/Biotech: https://securities.miraeasset.com/bbs/download/2113897.pdf?attachmentId=2113897

- News1: https://www.news1.kr/bio/general/5760028

- Daedeok Innopolis Venture Association: https://iva.or.kr/web/bbs/info/bbsView.do?bbsId=BBS_0003&menuId=&seq=392&nowPage=1