DEEP RESEARCH · OliX (KOSDAQ 226950)

OliX: From platform validation to clinical harvest

cp-asiRNA platform, the Eli Lilly MASH deal, and the three 2026 catalysts

0. Bottom line first

Backed by its asymmetric siRNA (asiRNA) and cell-penetrating asiRNA (cp-asiRNA) platforms, OliX shifts from “platform validation” to “commercial-value realization” in 2026, anchored by the Eli Lilly MASH/cardiometabolic deal. The three 2026 catalysts: ① OLX75016 (MASH) Phase 2 entry, ② OLX301A (AMD) global L/O or Phase 2 start, ③ OLX104C (hair loss) Phase 2a efficacy readout.

1. RNAi’s ‘third wave’ and OliX’s position

Global RNAi technology market is projected to grow from USD 2.75B in 2024 to USD 6.63B by 2033 (CAGR 10.4%). APAC is the fastest-growing region (CAGR 16.01%, 2026–2031). PR Newswire, Mordor Intelligence.

Interpretation: The two RNAi barriers are delivery and off-target effects. Alnylam solved liver delivery via GalNAc but extrahepatic delivery is still hard. OliX uses cp-asiRNA to deliver without LNPs to skin/eye/lung — a distinct niche.

2. Market: a USD 25B MASH opportunity

The global MASH (formerly NASH) market is projected to grow to ~USD 25.3B by 2026. Madrigal’s Rezdiffra is FDA-approved but oral dosing and hepatotoxicity monitoring are limitations; Lilly’s Zepbound shows strong weight loss but with muscle-loss concerns. LiverTox — Resmetirom, FDA approval analysis.

3. Platform: asiRNA → cp-asiRNA

asiRNA uses an asymmetric strand design so only the antisense strand loads into RISC — sharply lowering off-target effects vs Alnylam/Arrowhead. cp-asiRNA attaches a lipophilic group so the molecule penetrates cell membranes without LNPs. FirstWord — TIDES 2020, PharmaVoice, Therapeutic siRNA — PMC.

4. Key pipelines — 2026 momentum

4.1 OLX75016 (MASH / obesity) — Lilly partnership

- MoA: silences hepatic MARC1 to improve lipid metabolism and reduce fibrosis. GWAS links MARC1 loss-of-function to lower liver fat and cirrhosis risk.

- Status: Phase 1 started Feb-2024 in Australia, n=58 in healthy adults and early fatty-liver patients, evaluating safety/tolerability. BioSpace, Larvol Sigma.

- Preclinical: synergy with semaglutide in NHPs — better weight loss, yo-yo suppression, muscle-sparing. BioSpace, Lilly investor.

- License: Feb-2025 global license with Eli Lilly worth ~USD 630M. Korea JoongAng Daily, Pharmaceutical Technology, BioSpace press release, BioSpace MASH deal.

Competitor comparison

| Feature | OLX75016 (OliX) | Rezdiffra (Madrigal) | Zepbound (Eli Lilly) |

|---|---|---|---|

| Mechanism | MARC1 silencing (RNAi) | THR-β agonist | GLP-1 / GIP dual agonist |

| Route / frequency | SC, every 3–6 months (long-acting) | Oral, once daily | SC, once weekly |

| Key data | Preclinical: synergy with GLP-1, fatty-liver improvement | Phase 3: fibrosis improvement, MASH resolution (FDA approved) | Phase 2: MASH resolution up to 73.3%, fibrosis improvement |

| Safety | Liver-specific delivery → minimal systemic toxicity expected | Diarrhea, nausea, liver-toxicity monitoring | GI side effects, muscle-loss concerns |

| Differentiator | Convenient dosing + muscle-sparing fat loss | First oral MASH drug | Strong weight loss, ideal for obese MASH |

4.2 OLX301A (wet/dry AMD)

Silences both neovascular and inflammatory genes in the eye. Unlike Eylea/Lucentis that only target VEGF, OLX301A also controls the inflammatory pathway — a potential option for anti-VEGF refractory patients. The 2024 rights return from Théa was due to Théa’s internal strategy, not efficacy. The completed 2025 US Phase 1 showed safety and BCVA improvement potential. KBR — Phase 1 safety, FirstWord — Théa collaboration, KBR — Théa rights return, Glance by Eyes On Eyecare, FirstWord — OTS 2020.

4.3 OLX104C (androgenetic alopecia)

Silences androgen receptor (AR) only in scalp tissue; degrades quickly if it reaches blood, eliminating finasteride-style systemic side effects (sexual dysfunction, depression). Phase 1 done in Australia; first patient dosed in Phase 1b/2a in late 2025. 2026 expects Phase 2a efficacy data — potentially the first RNAi hair-loss therapeutic to show efficacy in humans. FirstWord — preclinical, KBR — World Congress for Hair Research, Biospectator — AR RNAi 1b/2a first dose, KBR — L’Oréal RNAi partnership.

5. Financials & risk

5.1 Cashflow / capital

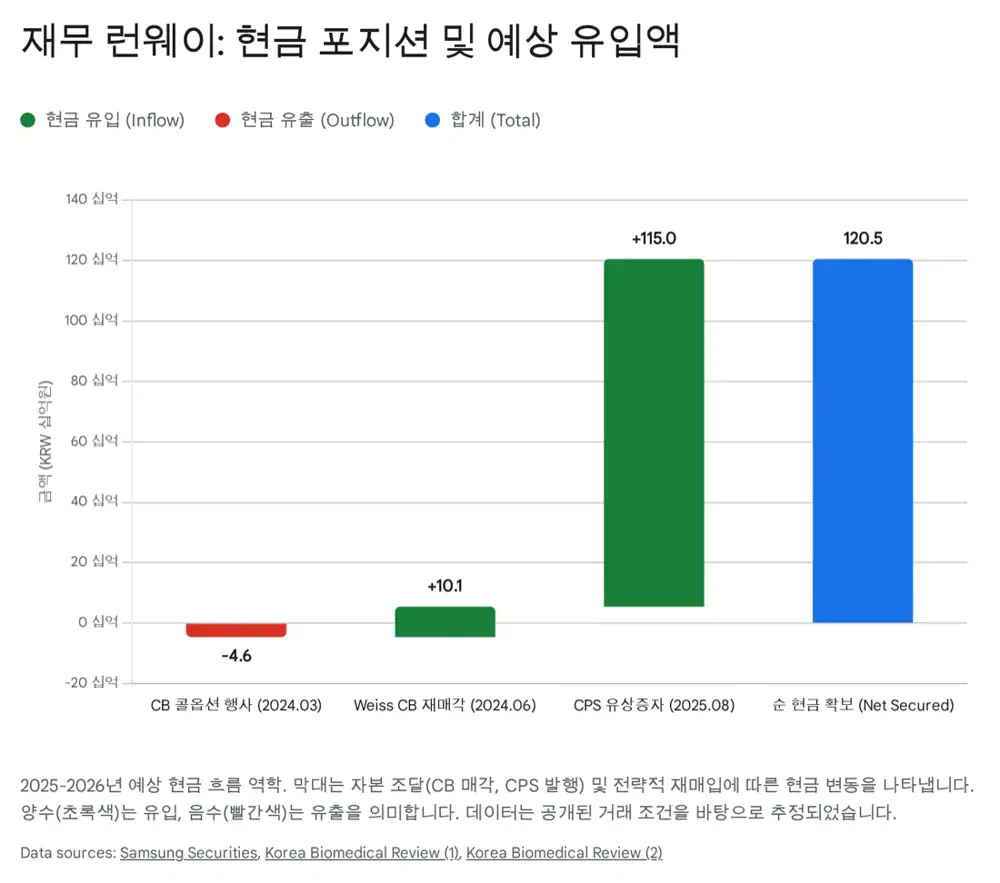

- Aug-2025 KRW 115B convertible preferred stock issuance. KBR, Webull debt analysis

- Lilly upfront + end-2025 estimated cash ~KRW 131.5B → R&D covered.

- From 2026, milestone revenues turn OliX into a revenue-generating biotech.

5.2 CB overhang resolved

Of KRW 14.7B CB, ~KRW 4.6B was called and re-sold to US hedge fund Weiss Asset Management for ~KRW 10.1B, sharply reducing near-term selling overhang. KBR, Bondweb.

5.3 Clinical risk

Interpretation: 2026 is the Phase 2 entry zone — a ‘valley of death’ window. FDA endpoints for MASH are strict; monitor Lilly’s trial design and execution closely.

6. 2026 milestones & rationale

OLX75016 Phase 2 entry

Australia Phase 1 MAD wraps H1-26 → Lilly’s competitive pressure vs Novo means immediate Phase 2 → milestone payments.

OLX301A global L/O or Phase 2

With clinical data in hand, negotiate at higher valuation. JPM 2026 catalyst accelerates the timeline.

OLX104C Phase 2a efficacy

Positive hair-count data could trigger L/O with L’Oréal or other beauty/consumer-health players.

7. Summary

- Investment thesis: The Lilly deal validates OliX globally. 2026 turns the partnership into Phase 2 progress and real cashflow.

- Risk management: Portfolio diversified across metabolic, ophthalmic and dermatologic. CB overhang preemptively addressed.

- Conclusion: 2026 is the peak of a ‘Big Cycle’ — H2-26 MASH Phase 2 entry plus hair-loss efficacy data are the key catalysts.

Appendix: competitor comparison

| Indication | OliX program | Major competitor | OliX differentiation |

|---|---|---|---|

| MASH | OLX75016 (Lilly) | Rezdiffra (Madrigal) | Long-acting injection, muscle-sparing fat loss |

| AMD | OLX301A | Eylea (Regeneron/Bayer) | Anti-VEGF refractory + dry AMD extension |

| Hair loss | OLX104C | Finasteride (Merck) | Scalp-local action, no systemic side effects |

Sources

- Naver blog source: m.blog.naver.com/.../224149302365

- EMIS — Olix profile: emis.com

- Korea JoongAng Daily — Lilly $630M: koreajoongangdaily.joins.com

- Pharmaceutical Technology — Lilly $630M: pharmaceutical-technology.com

- Glance — first AMD patient: glance.eyesoneyecare.com

- PR Newswire — RNAi market: prnewswire.com

- Mordor Intelligence — RNAi: mordorintelligence.com

- PMC — Therapeutic siRNA: pmc.ncbi.nlm.nih.gov

- PharmaVoice — Dong-ki Lee interview: pharmavoice.com

- FirstWord — TIDES 2020: firstwordpharma.com

- LiverTox — Resmetirom: ncbi.nlm.nih.gov

- PitchBook — Olix profile: pitchbook.com

- BioSpace — Lilly license press release: biospace.com

- KRX — Olix filing: kind.krx.co.kr

- FirstWord — OTS 2020: firstwordpharma.com

- BioSpace — Lilly MASH/Cancer back-to-back deals: biospace.com

- Larvol Sigma — OLX75016 trial: sigma.larvol.com

- BioSpace — OLX75016 first dose: biospace.com

- BioSpace — semaglutide combo preclinical: biospace.com

- Lilly — tirzepatide MASH: investor.lilly.com

- FirstWord — Théa collaboration: firstwordpharma.com

- KBR — Théa rights return: koreabiomed.com

- KBR — OLX301A safety: koreabiomed.com

- FirstWord — hair-loss preclinical: firstwordpharma.com

- KBR — Hair Research congress: koreabiomed.com

- Biospectator — AR RNAi 1b/2a: biospectator.com

- KBR — KRW 115B CPS: koreabiomed.com

- Webull — debt analysis: webull.com

- Bondweb research: bondweb.co.kr

- KBR — CB resale: koreabiomed.com

- Exploration Pub — Rezdiffra FDA: explorationpub.com

- KN Daily — JPM 2026: kndaily.co.kr

- KBR — L’Oréal RNAi partnership: koreabiomed.com