DEEP RESEARCH · VORONOI

Voronoi: VORONOMICS and the VRN11/VRN10 Global Leap Thesis

A review of precision targeted therapy, BBB penetration, and 2026 clinical/licensing catalysts.

0. Bottom line first

The core source thesis is that Voronoi should be read not merely as a clinical-expectation biotech, but as an AI-based small-molecule kinase-inhibitor platform that improves both selectivity and blood-brain-barrier penetration.

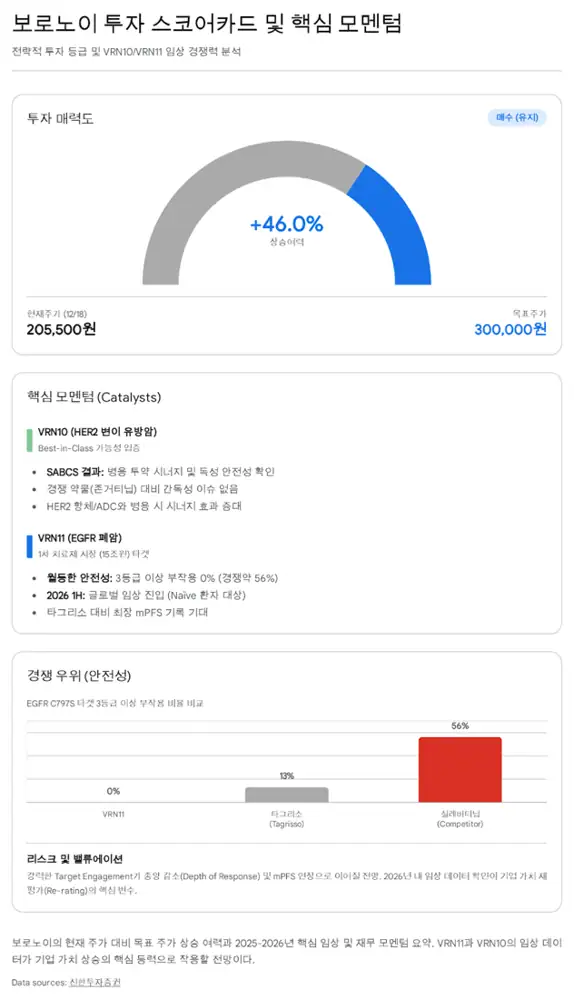

Official fact: The source presents a Buy opinion, KRW 300,000 target price, and about 46% upside. This is the source author's research opinion, not a recommendation here.

Interpretation: The main checkpoints for me are VRN11's C797S and first-line expansion, VRN10's potential as an Enhertu combination partner, and the clinical data expected through 2026.

1. Company and VORONOMICS platform

Official fact: Voronoi was founded in February 2015 and has its headquarters and key research facilities in Songdo, Incheon. It also operates VORONOI USA, INC., a 100%-owned Boston subsidiary, for global clinical and business-development work.

Official fact: As of Q3 2025, Voronoi had 149 employees. The source highlights a connected R&D infrastructure across medicinal chemistry, biology, animal testing, and AI labs, and says the company shortened candidate discovery from a typical 4.5 years to 1-1.5 years.

- Selectivity: the platform aims to reduce toxicity by targeting specific kinases among more than 500 human kinases.

- BBB penetration: from the molecular-design stage, properties favorable to brain penetration are optimized for brain-metastasis challenges in lung and breast cancer.

- Validation: VRN07/ORIC-114 was licensed to ORIC Pharmaceuticals in October 2020, and VRN06 was licensed to HK inno.N in 2021.

2. Market setup

| Market/disease | Source figure | Meaning |

|---|---|---|

| Global kinase inhibitors | USD 57.2bn in 2021, USD 95.3bn-189.2bn in 2030 | Source presents 7.3-10.5% CAGR, above overall pharma growth |

| NSCLC | About 85% of all lung cancer | Core indication for EGFR targeted therapy |

| Asian EGFR mutation-positive | About 40-50% of NSCLC patients | Basis for high EGFR drug demand in Asia |

| EGFR inhibitor market | USD 15.6bn in 2025, USD 32.8bn in 2032 | 11.2% CAGR forecast |

Interpretation: The competition in kinase inhibitors is shifting from efficacy alone to selectivity, toxicity, and BBB penetration. The source treats Tagrisso-resistant C797S and HER2 ADC combination limits as Voronoi's opportunity.

3. VRN11: fourth-generation EGFR TKI

Official fact: VRN11 is a fourth-generation TKI that selectively binds EGFR mutations including C797S. C797S is a resistance mechanism in which Cysteine 797, the covalent binding site for Tagrisso, changes to Serine and interferes with drug binding.

Kp,uu,CSF > 2.0

The source says VRN11's CSF concentration is more than two times unbound plasma concentration, over 10 times Tagrisso's roughly 0.2.

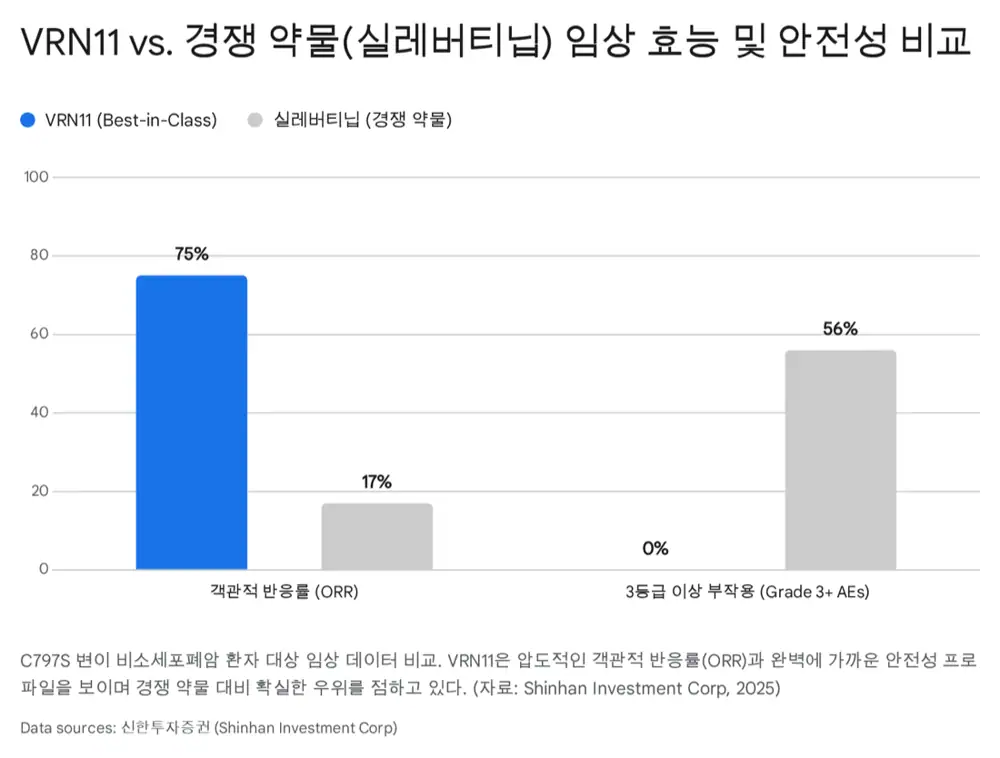

75% ORR in C797S

Based on 2025 AACR-NCI-EORTC and updated data cited in the source, ORR in C797S-positive patients is 75%, versus 17% for silevertinib.

0% Grade 3+ TRAE

The source presents 0% drug-related adverse events of Grade 3 or higher across patients, compared with 56% for silevertinib.

The source also says a complete response in brain metastasis was reported in a 160mg cohort. It frames the C797S mutation market at about KRW 1tn and the first-line market at KRW 15tn in annual revenue, arguing that the strategy extends from second-line use into first-line treatment.

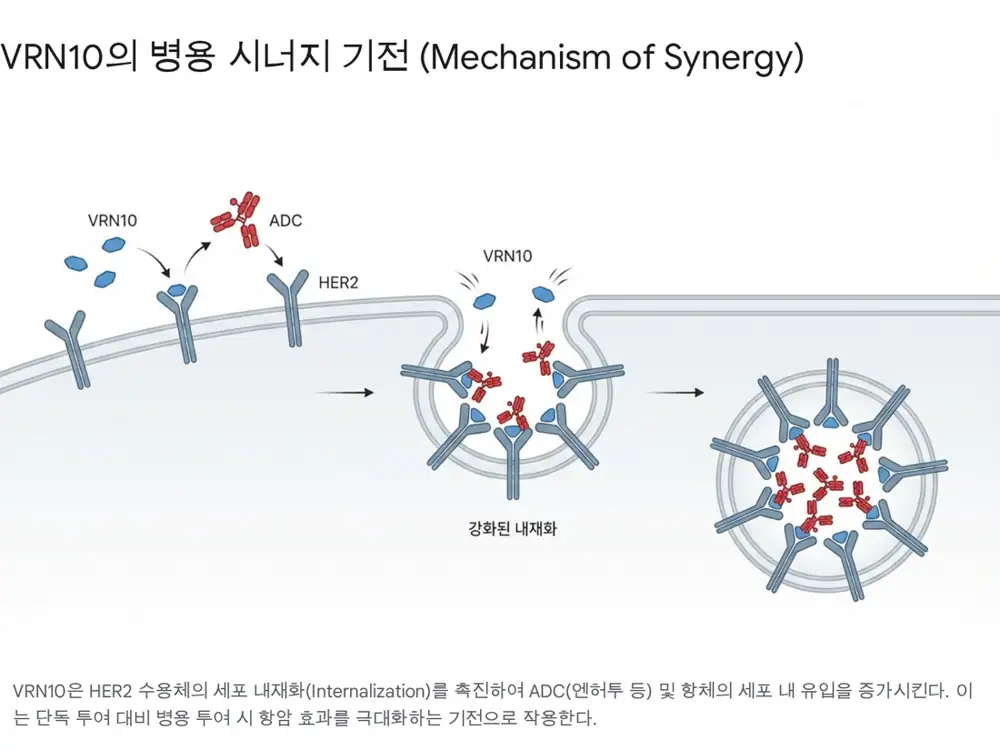

4. VRN10: Enhertu combination-partner thesis

VRN10 is presented as a small-molecule TKI candidate that could complement Enhertu's strong HER2-positive breast-cancer efficacy while addressing the combination limits created by ILD and liver-toxicity concerns.

Official fact: The source says recent phase 1a data showed tumor-size reduction with VRN10 monotherapy and no liver toxicity, which is a chronic issue for competing drugs.

Interpretation: The key is that VRN10 promotes HER2 receptor internalization. Since ADCs need to bind receptors and enter cells to release payloads, the source argues VRN10 could help Enhertu deliver more anticancer effect in combination.

5. Pipeline and financials

| Pipeline/item | Source content | What to watch |

|---|---|---|

| VRN07 / ORIC-114 | EGFR Exon 20 insertion therapy licensed to ORIC in 2020 | 2023 ESMO phase 1b data including CR in brain-metastasis patients; final phase 1b result planned for 2025 |

| VRN06 | RET fusion therapy licensed to HK inno.N | Preclinical and clinical-entry stage |

| VRN04 / VRN13 | RIPK1 inhibitor for autoimmune disease and PDGFR inhibitor for pulmonary arterial hypertension | Early pipeline breadth |

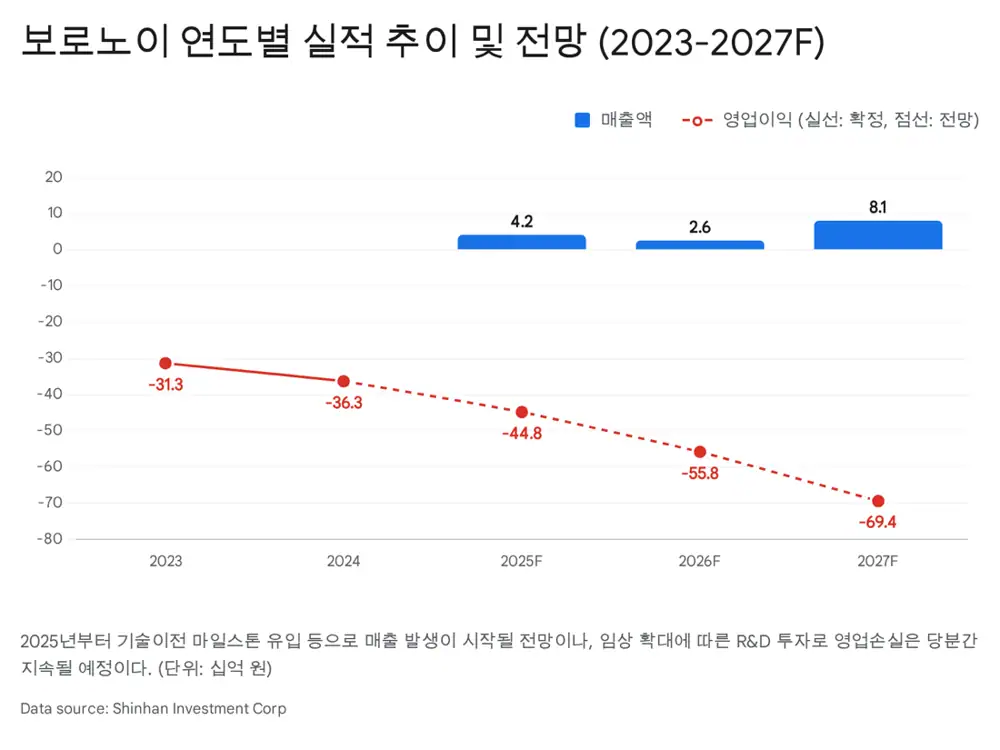

| 2024 loss | Operating loss about KRW 36.3bn and net loss KRW 32.6bn | Biotech loss structure from R&D spending |

| 2025 outlook | Operating loss about KRW 44.8bn, revenue beginning at KRW 4.2bn | Technology-transfer milestone inflow |

| 2026 possibility | Net income of KRW 49.6bn expected if a large L/O deal happens | Licensing deal such as VRN10 |

| Liquidity | Cash-like and current assets about KRW 73.8bn at Q3 2025 | Source view: enough to cover near-term clinical costs |

| Overhang | Third CB issue about KRW 50bn | Potential increase in floating shares if converted |

6. 2026 catalysts and risks

- First half 2026: VRN11 global phase 1b/2 study entry in treatment-naive patients.

- Second half 2026: VRN11 first-line efficacy data and Depth of Response versus Tagrisso.

- Ad hoc event: possible global licensing deal for VRN10.

- Risks: clinical failure, weak data quality, dilution from financing, CB/EB overhang, and delay of a large L/O deal.

7. My conclusion

For Voronoi, 2026 data may decide the direction of enterprise value. VRN11 combines a C797S opportunity with first-line expansion potential, while VRN10 has strategic positioning as an Enhertu-combination candidate. Still, all valuation logic in the source depends on clinical data and licensing execution, so data quality should come before headline numbers.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224149301551

- Source 2: https://www.sphericalinsights.com/reports/kinase-inhibitors-market

- Source 3: https://www.mordorintelligence.com/industry-reports/tyrosine-kinase-inhibitors-market

- Source 4: https://www.researchandmarkets.com/report/small-molecule-kinase-inhibitors

- Source 5: https://www.coherentmi.com/industry-reports/egfr-non-small-cell-lung-cancer-egfr-nsclc-market

- Source 6: https://www.strategicmarketresearch.com/market-report/bcr-abl-tyrosine-kinase-inhibitor-drug-market

- Source 7: https://www.biospace.com/press-releases/metastatic-her2-positive-breast-cancer-market-to-reach-usd-3-108-1-million-by-2035-impelled-by-significant-progress-in-monoclonal-antibodies-antibody-drug-conjugates-adcs-and-tyrosine-kinase-inhibitors-tkis

- Source 8: https://www.businesswire.com/news/home/20260113902192/en/CD22-Targeted-Therapies-Market-Research-Report-2025-2026-Approved-Drug-Sales-Technology-Platforms-Clinical-Trials-Insights---ResearchAndMarkets.com

- Source 9: https://www.tandfonline.com/doi/full/10.1080/14756366.2025.2481392

- Source 10: https://dealsite.co.kr/articles/147900