DEEP RESEARCH · Woorim PTS

Woorim PTS: From Gearboxes to Defense and Robotics Powertrains

A review of the Q3 2025 qualitative turnaround, portfolio shift, and valuation rerating thesis.

0. Bottom line first

The source thesis is that Woorim PTS should be revalued not as a traditional heavy-equipment parts maker, but as a core powertrain supplier to K-defense and robotic automation, built on 50 years of gear and reducer technology.

Official fact: The source interprets the Q3 2025 cumulative result as a “qualitative turnaround”: revenue fell 26.7% year over year to KRW 41.523bn, while operating profit rose 52.3% to KRW 2.453bn.

Interpretation: My key validation points are the durability of mix improvement, defense export volume converting into parts orders, securing robot-reducer customers, and whether the reason Woorim trades at 2.68x PBR versus SPG at 7.01x PBR begins to fade.

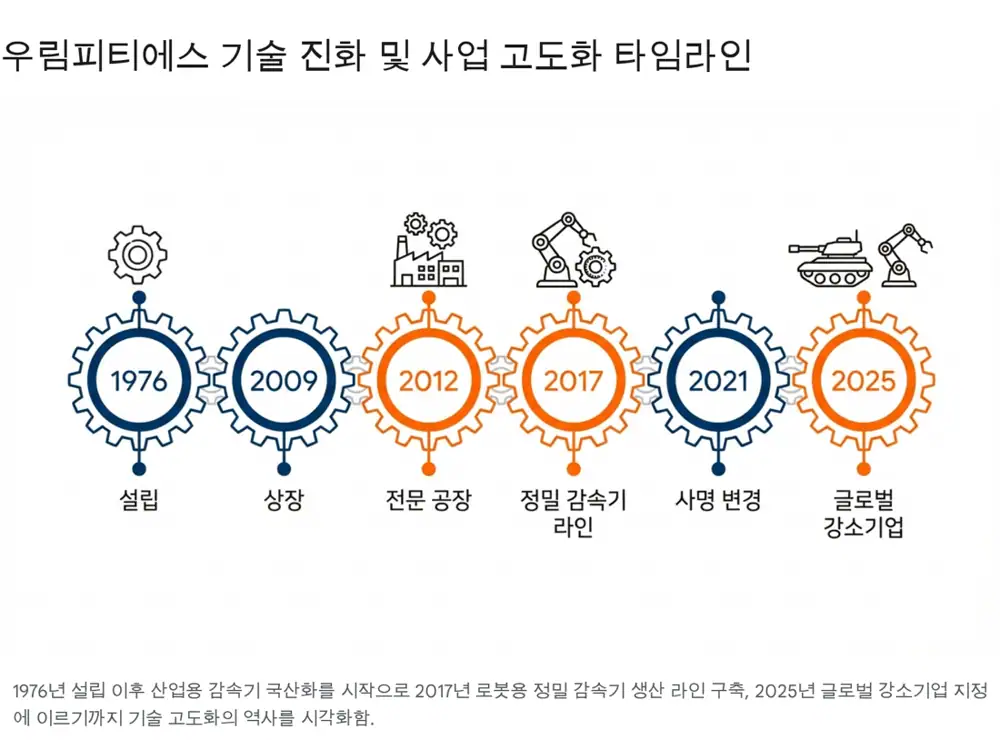

1. Origin and technology accumulation

Woorim PTS began in October 1976 as PARAMOUNT Machinery Industrial Company and has focused on reducers and transmissions. The source frames it not merely as a parts maker, but as a company that grew alongside the upgrading of Korea’s machinery industry.

| Period | Source milestone | Meaning |

|---|---|---|

| 1976-1999 | Founded in 1976; CEO Hyun-seok Han acquired the former Woorim Machinery Industrial in 1998 | Built basic gear-processing capability and a domestic industrial reducer base |

| 2000-2010 | Incorporated in 2000; research institute in 2006; KOSDAQ listing in 2009; Inno-Biz and ISO 14001 | Secured growth capital and technology/management systems |

| 2011-2020 | Completed Changwon Seongsan Plant 1 in 2012; localized converter tilting equipment in 2013; built robot/automation precision reducer line in 2017 | Moved into more difficult large-plant and ultra-precision domains |

| 2021-present | Renamed from Woorim Machinery to Woorim PTS in 2021; co-CEO Woo-jin Han system; selected as Small but Strong Materials/Parts/Equipment Company 100 in 2021 and Global Small Giant 1000+ in 2025 | Identity shift into a power-transmission solution company |

2. Business portfolio: three-way mix of stability and growth

Industrial plants

Products include rolling-mill reducers, converter tilting equipment, crane reducers, and shale-gas/oil pumping gearboxes. The source says Woorim PTS is the only Korean company able to independently design and manufacture converter tilting equipment.

Heavy equipment

The company mass-produces standardized travel and swing motor gearboxes. The source says it supplies Doosan Mottrol, HD Hyundai Construction Equipment, Volvo Group Korea, and John Deere on an OEM/ODM basis.

New businesses

K2 tanks, K9 self-propelled howitzers, armored vehicles, Surion helicopter parts, robot precision reducers, and machine-tool precision gears are presented as growth engines.

3. Economic moat: dual production and reliability

Official fact: The source says Woorim operates two specialized factories in Changwon. Plant 1 is 14,370 square meters and optimized for large gearboxes and steelmaking equipment, while Plant 2 is 10,574 square meters with temperature, humidity, and dust controls for robot reducers and aerospace/defense parts.

Interpretation: The moat is not just plant size. It is the ability to run both “small-item mass production” and “high-mix low-volume order production” inside one company. Defense parts require Mil-Spec and long-term reliability, so a 50-year track record and customer lock-in become entry barriers.

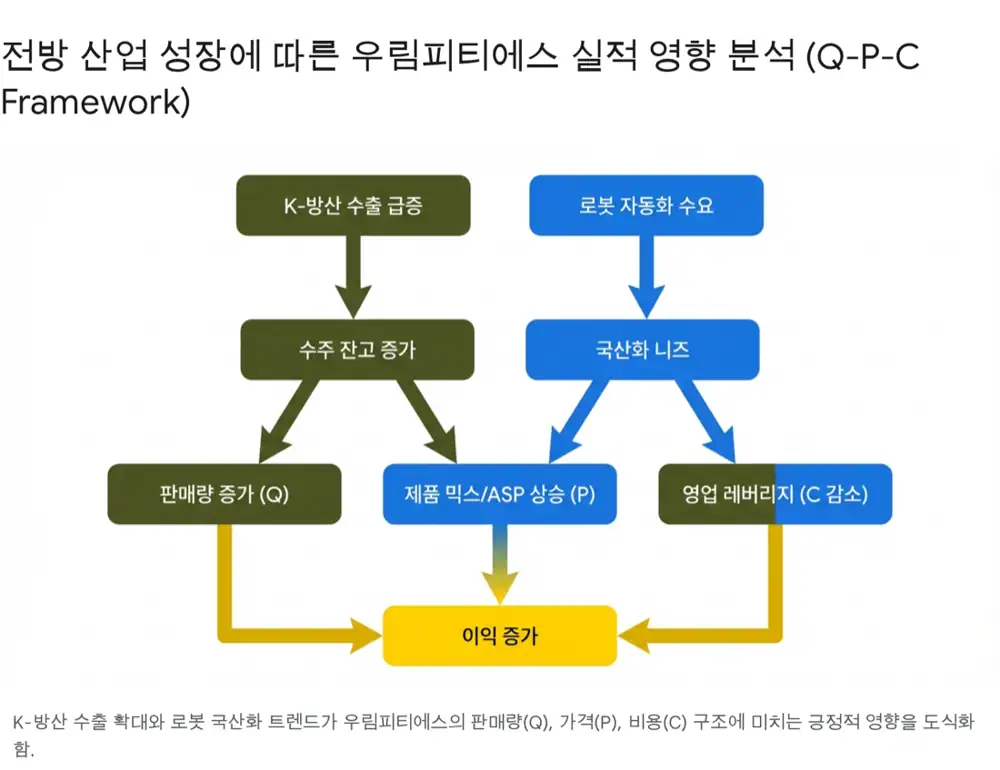

4. End-market growth: defense and robotics change Q, P, and C

| Axis | Defense | Robotics/automation |

|---|---|---|

| Q | The source cites roughly KRW 6.65tn in combined 2026 operating-profit forecasts for major Korean defense companies and more than KRW 100tn in order backlog. Poland K2/K9 exports are framed as 5-10 years of long-term volume. | Investments by Samsung Electronics, Hyundai Motor Group/Boston Dynamics, and Doosan Robotics are expected to grow demand for precision reducers. |

| P | High-reliability defense parts command higher prices than ordinary industrial parts, and localized products can gain pricing power. | The logic is higher penetration through Japan-comparable quality at competitive pricing. |

| C | Higher utilization of Plant 2 defense lines can spread fixed costs and create operating leverage. | The source highlights a robot precision reducer line with annual capacity of 20,000 sets and potential first-tier vendor status for large companies. |

The source says heavy equipment was temporarily hurt by China’s construction slowdown, but is recovering with infrastructure investment in India and North America plus mining-development demand.

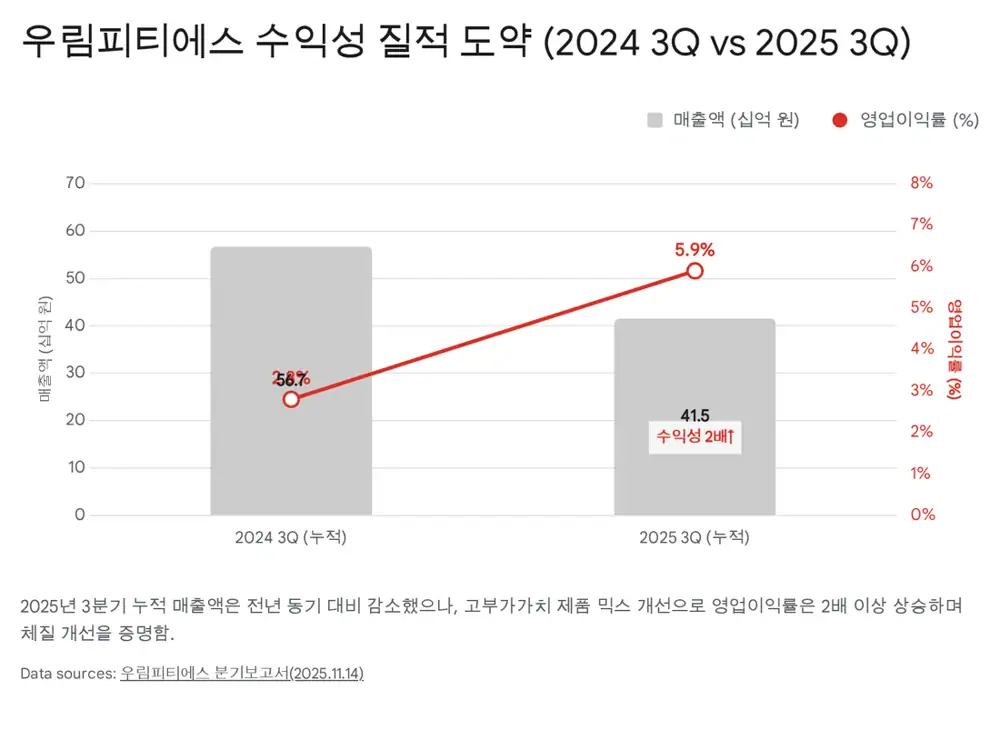

5. Q3 2025: qualitative turnaround

| Item | Q3 2025 cumulative | Prior-year period | Change |

|---|---|---|---|

| Revenue | KRW 41.523bn | KRW 56.679bn | -26.7% |

| Operating profit | KRW 2.453bn | KRW 1.610bn | +52.3% |

| Operating margin | About 5.9% | 2.8% | More than doubled |

| Net income | KRW 2.418bn | KRW 2.092bn | +15.5% |

Interpretation: The source attributes profit growth despite lower revenue to product-mix improvement. Lower-margin general industrial and heavy-equipment parts declined, while higher-margin defense parts and precision reducers increased.

6. Financial stability and valuation

20.9% debt ratio

As of the end of Q3 2025, the source presents this as very low leverage versus manufacturing peers.

About 285% current ratio

Current assets were KRW 44.5bn and current liabilities KRW 15.6bn. Cash and equivalents were about KRW 8bn.

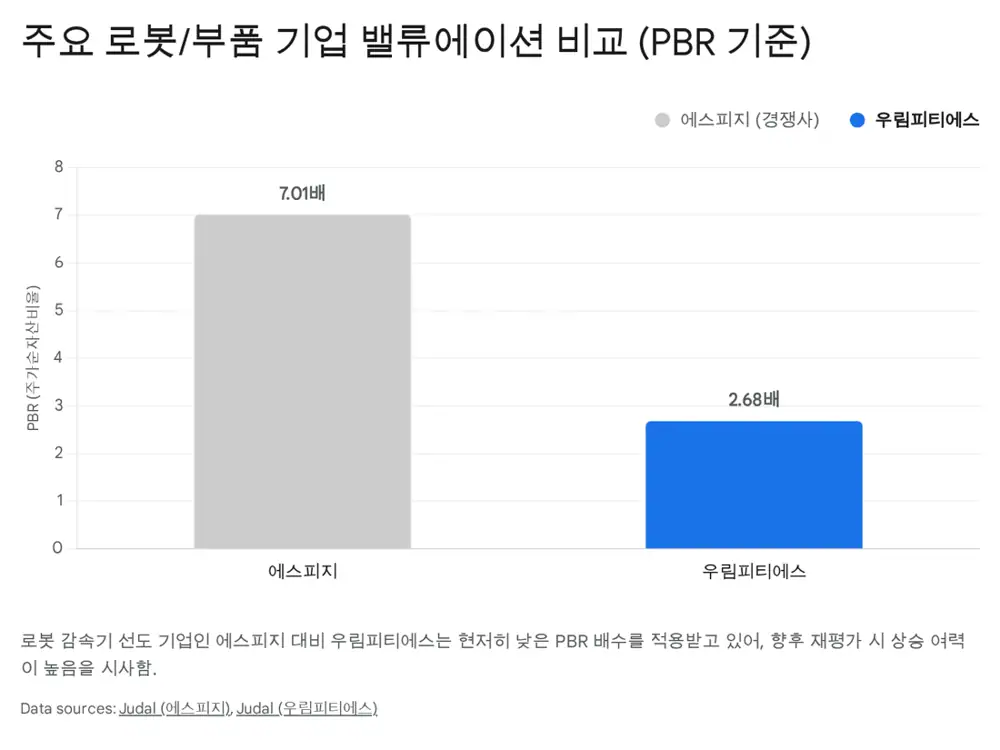

2.68x PBR

The source cites Woorim’s market cap at about KRW 300bn and frames it as more than 60% discounted versus SPG’s 7.01x PBR.

| Peer | Source figure/logic | Implication |

|---|---|---|

| SPG | PER about 135x, PBR about 7.01x | Benchmark for the robotics premium that robot-parts companies can receive |

| NBR Motion | Precision bearing and roller maker entering robot parts after IPO | Example that the market can apply favorable multiples to new robot-parts entrants |

| Woorim PTS | PBR 2.68x, market cap about KRW 300bn | Rerating potential if the frame shifts from traditional machinery to defense/robotics |

Interpretation: The source’s rerating logic is a shift from traditional machinery at around 10x PER to defense/robotics at 30-50x or more. But that thesis depends on real evidence of rising defense revenue mix and robot-reducer references.

7. Investment scenario and catalysts

Official fact: The source presents a Buy opinion for Woorim PTS. That is the source author’s opinion and is not a buy recommendation in this reformatted material.

- Short-term target: KRW 23,000, described as the prior high, first resistance level, and short-term target.

- Mid-to-long-term scenario: after 2026, if defense exports are reflected in earnings and robot-reducer revenue becomes visible, the source says a move above KRW 30,000 could be expected.

- Key catalysts: parts supply tied to Poland’s second execution contract, new overseas defense orders, robot-customer news from Samsung, Hyundai, Boston Dynamics, and defense-export financing or robot-industry policy.

- Risks: delayed construction/equipment investment, higher raw-material prices such as specialty steel, and profitability damage from a lower KRW/USD exchange rate.

8. My conclusion

Woorim PTS’s investment point is “quality of earnings” more than “revenue growth.” If the Q3 2025 pattern repeats, where margins improve despite lower revenue, the market can reclassify the company from a traditional machinery-parts maker into a defense and robotics parts company. If defense and robotics revenue contribution is delayed, the PBR discount will be harder to close.

Sources

- Source 1: Naver Blog original