DEEP RESEARCH · NEOTIS

Neotis Structural Re-Rating Research Report

A compact manufacturer analyzed through micro bits, automotive shafts, and electronics controllers

0. Bottom line first

Neotis appears to be moving from a traditional manufacturer into a precision-processing and automotive-electronics solutions company, with lens-polishing equipment and controller revenue added to its micro-bit and motor-shaft base.

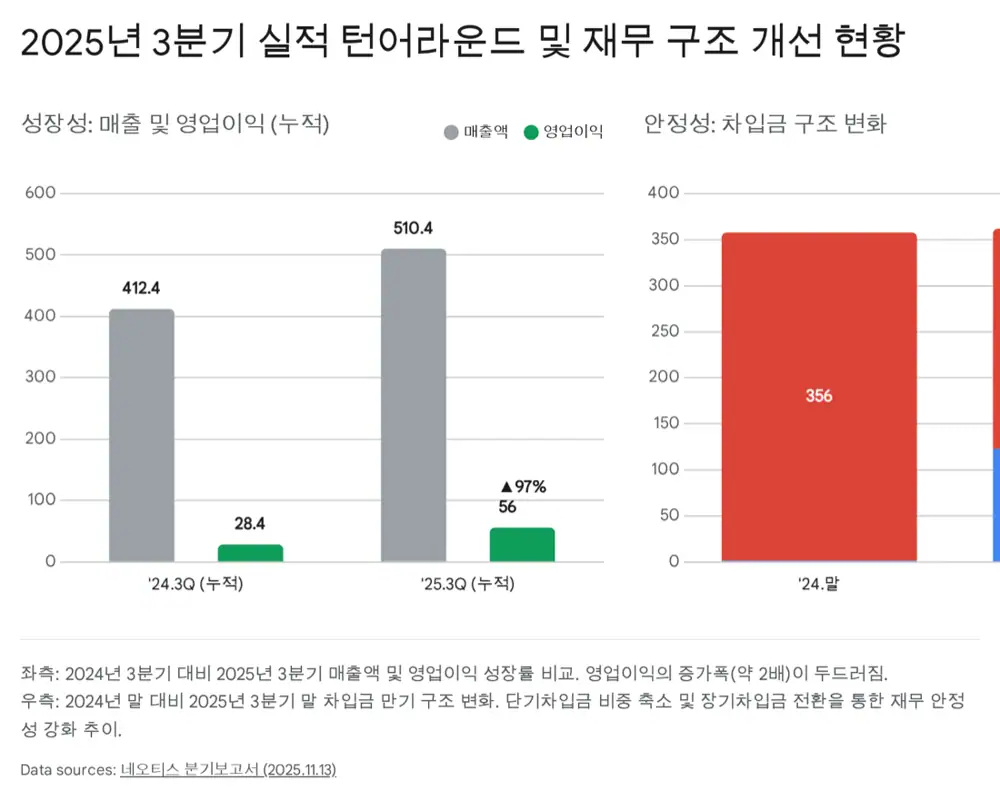

Official fact: The source gives 2025 third-quarter cumulative revenue of KRW 51.03727 billion, operating profit of KRW 5.60223 billion, operating profit growth of 97.32% year over year, cash and cash equivalents of KRW 23.3 billion, and a debt ratio of about 65.3%.

Interpretation: The key is not just revenue growth but improvement in earnings quality, driven by higher-margin mix and automation.

1. Governance and business base

Neotis was founded in 2000 and grew around PCB micro bits and automotive motor shafts. As of the third quarter of 2025, chair Kwon Eun-young held 17.9%, or 2,495,958 shares; including CEO Kwon Sang-hoon at 12.6% and Kim Hyun-mi at 5.7%, friendly ownership is presented at about 43.8%.

Subsidiary Neodis, 53.57% owned, specializes in automotive motor shafts and is also led by CEO Kwon Sang-hoon, linking shaft operations with group manufacturing strategy.

2. 2025 third-quarter financial turnaround

| Item | 2025 Q3 cumulative | Meaning |

|---|---|---|

| Revenue | KRW 51.03727 billion | Up 23.76% from KRW 41.24035 billion a year earlier |

| Operating profit | KRW 5.60223 billion | Up 97.32% from KRW 2.83917 billion |

| Net profit | KRW 3.86747 billion | Slightly down year over year but still profitable |

| Debt ratio | About 65.3% | Viewed as healthy for a manufacturer |

Short-term borrowings fell from KRW 35.6 billion at year-end 2024 to KRW 23.8 billion at 2025 Q3, down about KRW 11.8 billion or 33%. Long-term borrowings rose from about KRW 0.14 billion to KRW 12.3 billion, which the source interprets as maturity extension and strategic financial management.

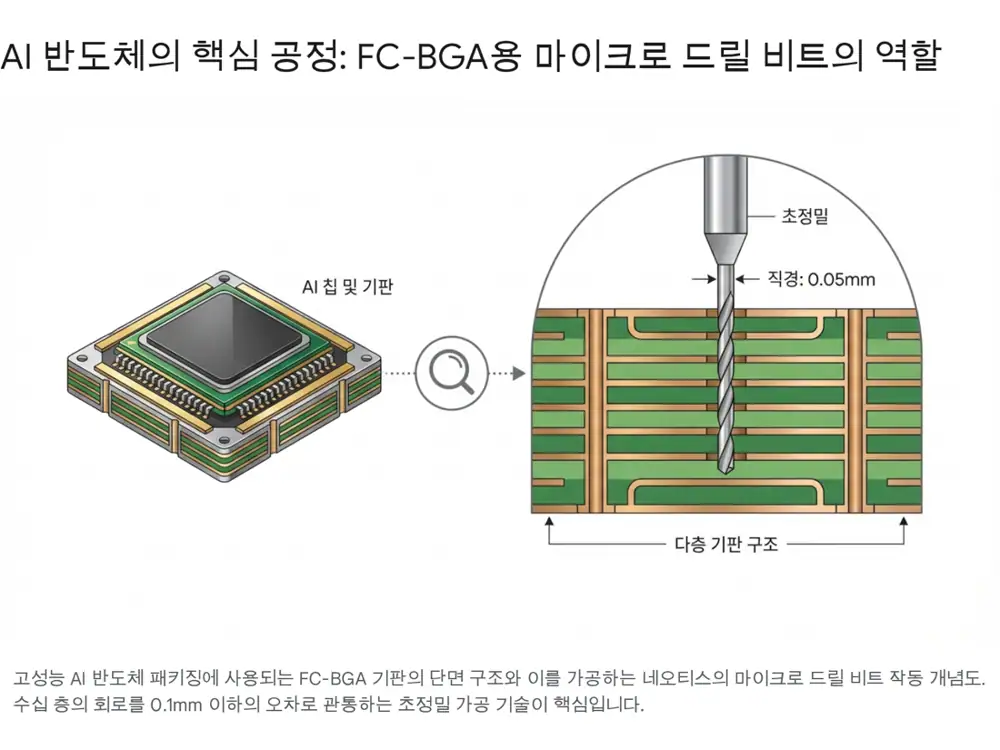

3. Micro bits: hidden beneficiary of AI substrates

The micro-bit business is tied to FC-BGA demand from AI data centers, autonomous driving, and 5G networks. Neotis mass-produces ultra-small drill bits with 0.05mm-0.35mm diameters for substrate makers including Samsung Electro-Mechanics and Daeduck Electronics.

96.95%

Micro-bit factory utilization in Q3 2025 is presented as nearly full.

Tungsten carbide

The source cites USD 81.06/kg in September 2025, up about 19.98% month over month, as a cost risk.

Pass-through power

High-end FC-BGA drill bits are hard to replace, supporting potential cost pass-through.

4. Shafts and lens polishers

The shaft business centers on whirling. Unlike rolling, which presses material into shape, whirling cuts with high precision. It costs more but reduces motor noise and vibration.

Because EVs lack engine noise, motor sound becomes more noticeable, so global electronics suppliers such as Bosch, Brose, and Nidec are described as increasing adoption of whirling shafts in premium and EV lines. Shaft utilization is about 69.77%, leaving room for more revenue without major new investment.

Gwangjin Precision, acquired in 2021, generated KRW 16.0 billion in cumulative Q3 2025 revenue, 31.3% of total sales. The source says it competes technologically with German companies and contributes to profitability with an operating margin around 20%.

5. Electronics controllers and R&D

Neotis formed its electronics business unit in May 2022 and began supplying all panorama sunroof controllers for KG Mobility's Actyon and related models in the second half of 2025. The controller includes safety functions such as anti-pinch, not just open-close control.

For R&D, Neotis operates a corporate research institute founded in 2006 with teams for cutting tools, motor shafts, and electronics components. Q3 2025 R&D expense was about KRW 1.81016 billion, or 3.55% of revenue. The source also lists a 2013 Presidential Award and IR52 Jang Young-sil Awards in 2018 and 2021.

6. Risks and stock checkpoints

- Raw-material inflation such as tungsten and whether prices can be passed through

- FX volatility because exports account for 58.3%

- Possible profit-taking after a late-2025 rally and 52-week high

- As of January 2026, trading around KRW 9,400, after a December 2025 high of KRW 9,880 and more than triple the three-year low of KRW 2,760

- Expected 2026 PER below 10x and whether KRW 8,000 acts as support

7. Conclusion

The key triggers are FC-BGA growth, additional electronics orders, shaft mix improvement, and sustained profitability at Gwangjin Precision. Short-term overheating matters, but the business mix supports a possible re-rating from traditional manufacturer to AI-substrate, EV, and automotive-electronics component supplier.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224146766457

- Source 2: http://www.neotis.co.kr/sub/news/neo/view.html?noticeSeq=10

- Source 3: https://www.wowtv.co.kr/TotalSearch/Mariner/Index?searchTerm=%EC%87%BC%ED%8B%B0%EC%A7%80

- Source 4: https://cm.asiae.co.kr/article/2024091308040973616

- Source 5: https://www.bloter.net/news/articleView.html?idxno=627430

- Source 6: https://www.judal.co.kr/?view=stockAI&shareToken=WnMr65c97mf88ZxS

- Source 7: https://www.judal.co.kr/?view=stockAI&shareToken=QQbjd21Rypc7cm4m

- Source 8: http://www.dailyinvest.kr/news/articleViewAmp.html?idxno=69814