DEEP RESEARCH · MEDIANA

Mediana: AI Medical Solution Transition and Valuation Re-rating

A review of the shift from PMD/AED hardware manufacturing to AI-enabled medical solutions with Selvas AI.

0. Bottom line first

My core view is that Mediana is moving from a device seller to a medical data platform by adding Selvas AI voice recognition, medical data analytics, and predictive AI models to its more than 30-year PMD and AED hardware base.

Official fact: The source presents Q3 2025 cumulative revenue of KRW 45.7bn and operating profit of KRW 4.0bn as turnaround signals. It also says Mediana has distribution in more than 80 countries, over 2,500 customers, and cumulative sales above 700,000 units.

Interpretation: The source thesis is that the current share price reflects the legacy medical-device business and net cash, while assigning almost no value to the AI-solution option. The source DCF target price is KRW 10,150, implying 25-30% upside assuming a KRW 7,700-8,000 share price.

1. Company and ownership shift

Official fact: Mediana was founded in 1995. It operates headquarters and production facilities in Wonju, a Seoul office, and Mediana USA. Its businesses include patient monitors, AED and professional defibrillators, and body-composition analyzers.

Official fact: In early 2024, Selvas AI became the largest shareholder with 31.69%, while Selvas Healthcare held 5.83%. The appointment of Selvas AI CEO Kwak Min-cheol as Mediana CEO is presented as a key turning point.

Next-generation patient monitor

The roadmap points to AI analysis of ECG waves and vital signs, strengthening early warning for arrhythmia and cardiac-arrest signals.

Intelligent CMS

The plan extends Infoware X, which connects up to 32 monitors, into a hospital-wide server platform that uses AI to analyze patient trends.

Wearable and remote care

The concept monitors discharged and chronic-disease patients at home and links the data back to hospital CMS.

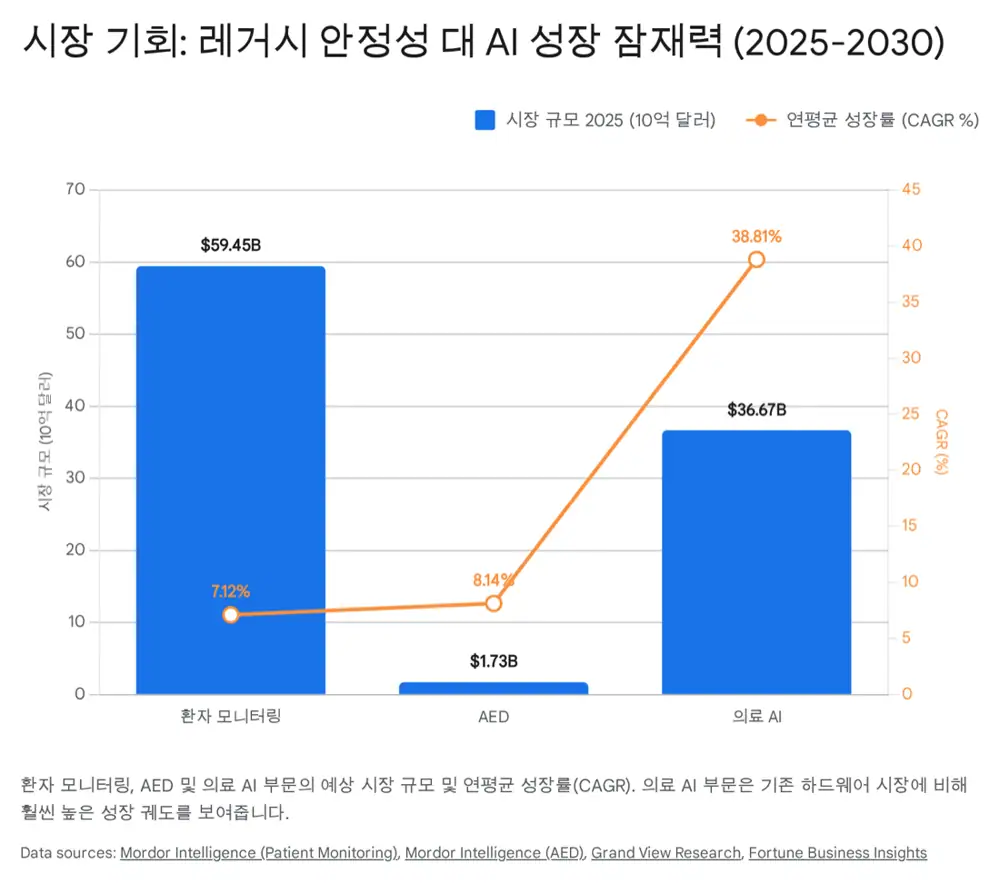

2. Markets: PMD, AED, AI healthcare

The source separates Mediana's TAM into traditional medical devices and AI healthcare. PMD and AED provide the stable base; AI healthcare provides the re-rating option.

| Market | Source figure | Core driver |

|---|---|---|

| Patient monitoring | USD 59.4bn in 2025, USD 83.8bn in 2030, 7.12% CAGR | Aging, chronic disease, hospital modernization, wireless and EMR connectivity |

| AED | USD 1.73bn in 2025, USD 2.56bn in 2030, 8.14% CAGR | Public-space installation mandates, home AED adoption, IoT maintenance |

| AI healthcare | USD 26.5bn in 2024, USD 505.5bn in 2033, 38.8% CAGR | Diagnostic algorithms, data analytics, clinician workflow tools |

| Korea AI healthcare | 50.8% CAGR forecast through 2030 | Digital-health policy and medical-data accessibility |

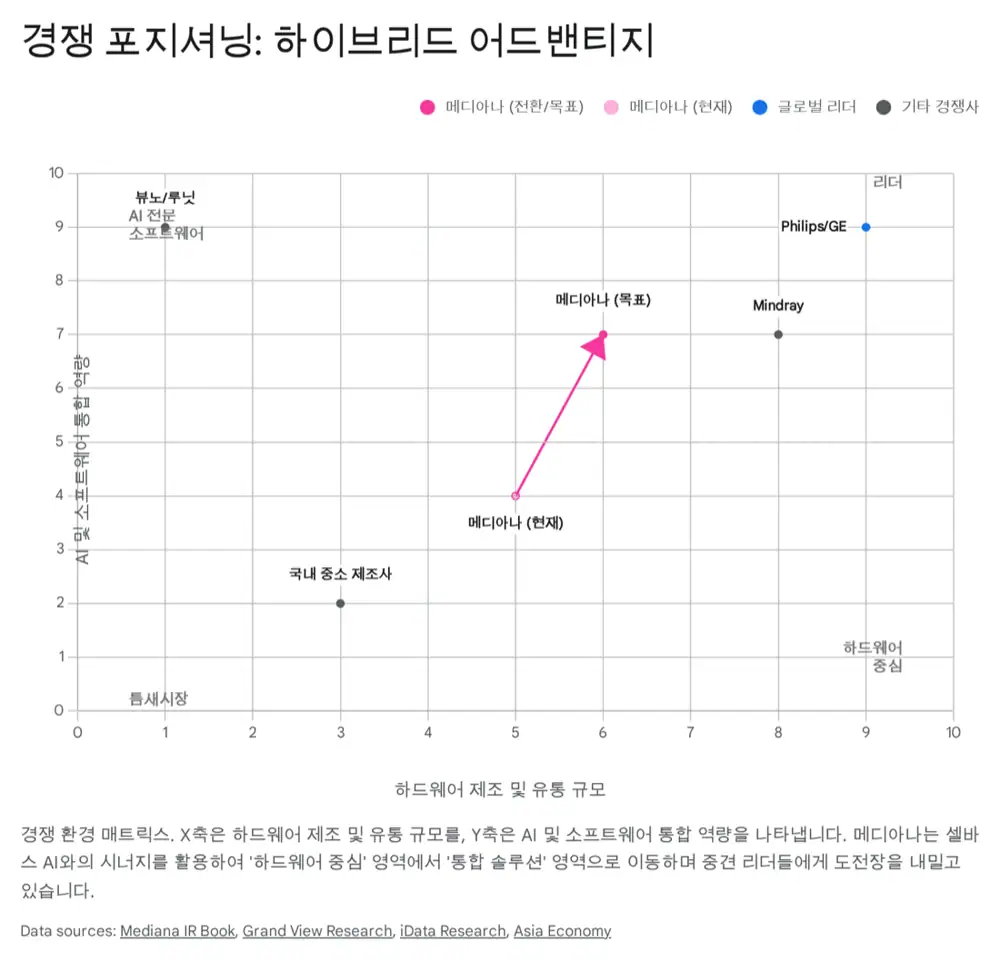

3. Competitive position and share thesis

Official fact: The source mentions Philips, GE Healthcare, Mindray, and Nihon Kohden as global Tier 1 peers, and Bionet, Mekics, Vuno, Lunit, and Seers Technology as domestic comparables.

- Hardware moat: FDA, CE, ISO approvals, 30 years of manufacturing experience, and a more than 20-year Medtronic partnership are presented as entry barriers.

- AI verticalization: Internal access to Selvas AI technology should help Mediana productize hardware+AI+voice recognition faster.

- Installed base: More than 700,000 devices in 80 countries create a base for CMS connection and software upgrades.

Interpretation: The source estimates Mediana's global patient-monitoring share at about 0.8-1.0% by revenue and its share in certain domestic segments, including AED, around 20%. Under an AI smart-hospital adoption thesis, it frames 25-30% domestic share by 2027 and 1.5-2.0% global share by 2030 as realistic targets.

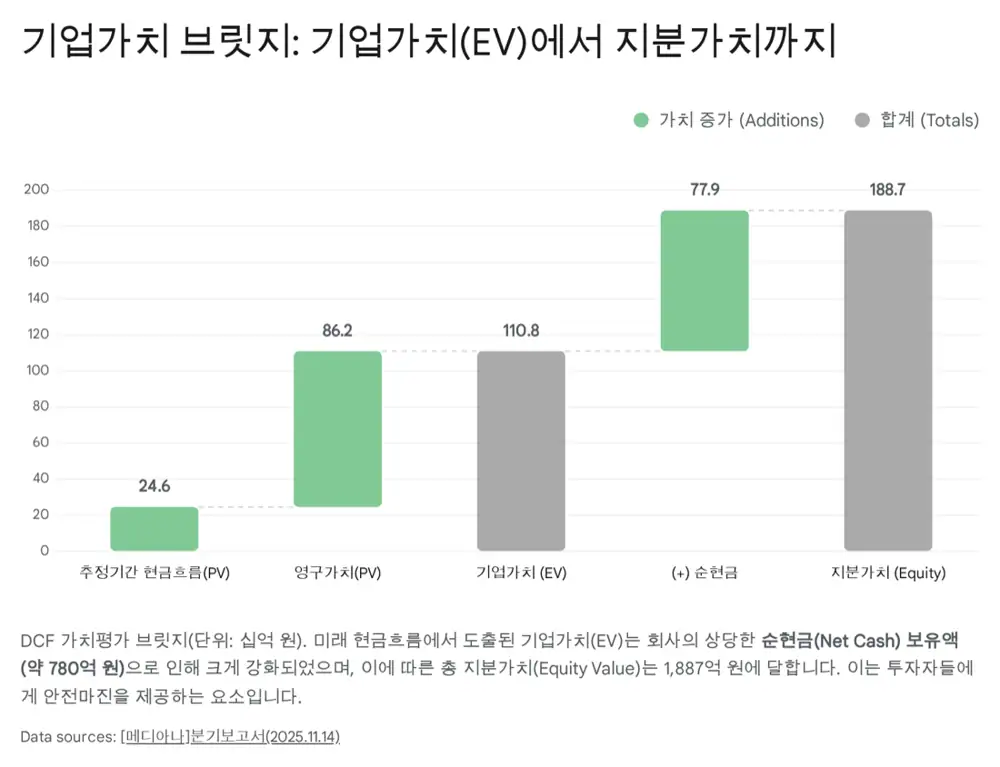

4. Earnings and DCF valuation

Official fact: Q3 2025 cumulative revenue was KRW 45.7bn, while Q3 revenue alone reached KRW 15.0bn, up 15.1% year over year. Q3 operating profit turned positive at KRW 1.58bn, cumulative operating profit was KRW 4.07bn, and OPM was about 8.9%.

Official fact: Net cash-like assets at the end of Q3 2025 are presented as about KRW 79.4bn. The source reflects KRW 79.4bn of cash-like assets, about KRW 1.5bn of interest-bearing liabilities, and KRW 77.9bn of net cash in its DCF equity value.

| Item | 2025E | 2026E | 2027E | 2028E | 2029E | 2030E |

|---|---|---|---|---|---|---|

| Revenue, KRW bn | 63.5 | 71.1 | 79.6 | 89.2 | 99.9 | 111.9 |

| Operating profit, KRW bn | 6.2 | 7.8 | 9.6 | 11.6 | 14.0 | 16.8 |

| OPM | 9.8% | 11.0% | 12.0% | 13.0% | 14.0% | 15.0% |

| FCFF, KRW bn | 3.3 | 4.1 | 5.1 | 6.3 | 7.8 | 9.7 |

| DCF assumption/result | Source figure |

|---|---|

| WACC | 9.35% |

| Risk-free rate | 3.36% |

| Beta | 0.77 |

| ERP | 5.5% |

| Cost of equity | 9.6% |

| Terminal growth | 2.0% |

| Enterprise value | KRW 110.8bn |

| Total equity value | KRW 188.7bn |

| Shares outstanding | 18,598,223 |

| Target price | KRW 10,146, rounded to KRW 10,150 |

5. Sensitivity and risks

| WACC / terminal growth | 1.5% | 2.0% Base | 2.5% |

|---|---|---|---|

| 8.85% | KRW 10,650 | KRW 11,200 | KRW 11,850 |

| 9.35% Base | KRW 9,700 | KRW 10,150 | KRW 10,700 |

| 9.85% | KRW 8,950 | KRW 9,350 | KRW 9,800 |

- PMI risk: Integration between a hardware manufacturer and a software company could delay synergy.

- Regulatory approvals: Medical devices with AI diagnostic-assist functions may face delays at MFDS, FDA, or CE MDR stages.

- FX and raw materials: More than 70% of revenue comes from exports, making FX and key parts such as semiconductor chips important variables.

6. My conclusion

I read Mediana as a Value + Growth setup: the profitable legacy medical-device business and net cash support downside, while the Selvas AI combination creates upside. The thesis still needs proof that AI-integrated products convert into revenue and approvals, and that CMS, wearables, and remote-care services become recurring revenue.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224146756407

- Source 2: https://www.mordorintelligence.com/industry-reports/global-patient-monitoring-market-industry

- Source 3: https://www.grandviewresearch.com/industry-analysis/patient-monitoring-devices-market

- Source 4: https://www.mordorintelligence.com/industry-reports/global-automated-external-defibrillator-market-industry

- Source 5: https://www.grandviewresearch.com/industry-analysis/artificial-intelligence-ai-healthcare-market

- Source 6: https://globalpricing.com/south-korea-unveils-five-year-roadmap-to-advance-ai-in-healthcare/

- Source 7: https://www.grandviewresearch.com/industry-analysis/remote-patient-monitoring-devices-market

- Source 8: https://idataresearch.com/product/patient-monitoring-market/

- Source 9: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240513000285&docno=&viewerhost=&

- Source 10: https://www.tossinvest.com/disclosure?symbol-or-stock-code=A041920&contentType=disclosure&contentParams=%7B%22id%22%3A%22DART%3AA%3A041920-20251114001473%22%2C%22companyCode%22%3A%22041920%22%2C%22reportItem%22%3A%224.2.0%22%7D

- Source 11: https://naver.me/5f5cXEUY

- Source 12: https://tradingeconomics.com/south-korea/government-bond-yield

- Source 13: https://in.investing.com/equities/mediana-co-ltd

- Source 14: https://kpmg.com/nl/en/home/topics/equity-market-risk-premium.html

- Source 15: https://www.judal.co.kr/?view=stockAI&shareToken=VGV1ZxcKorFtSytR

- Source 16: https://www.emergobyul.com/news/south-koreas-digital-medical-products-act-now-enforced