DEEP RESEARCH · BOS Semiconductors

BOS Semiconductors: Targeting the Central Brain of the SDV Era

A review of chiplets, Eagle-N, the Tier-0.5 model, and the 2026-2028 growth path.

0. Bottom line first

The source thesis is that BOS Semiconductors should be read not as a simple automotive fabless startup, but as a “Tier-0.5” system semiconductor company targeting central compute and autonomous-driving AI accelerators in the SDV era.

Official fact: The source says BOS has quickly built credibility since its 2022 founding through Hyundai Motor Group investment, collaboration with Jim Keller-led Tenstorrent, and a supply contract with a leading European OEM.

Interpretation: My main checkpoints are Eagle-N customer qualification, the Eagle-A sample timeline, 2026 Series B financing, and whether the European OEM relationship moves beyond PoC into a production-development contract.

Chiplet

The strategy combines process nodes by function, such as 5nm for NPU and 12nm for I/O, to pursue both cost efficiency and scalability.

Eagle-N 250 TOPS

The source frames it as a high-performance product for Level 3+ autonomy, sensor fusion, and in-vehicle LLMs, versus competitors at 10-30 TOPS.

Tier-0.5

Rather than handing chips to Tier-1s, BOS aims to define custom chips with OEMs from the vehicle-planning stage.

1. SDV transition and BOS positioning

The auto industry is shifting from internal-combustion mechanical engineering to software-defined vehicles. Older cars used hundreds of distributed MCUs for wipers, windows, engines, and other functions; autonomy and connectivity require centralized compute that can process and judge massive data in real time.

Interpretation: This shift lowers the relative weight of low-performance MCUs and raises the value of high-performance SoCs that combine APs and NPUs. That is why the source positions BOS as a candidate for the higher-barrier, higher-value “central brain” market rather than only the IVI or edge markets where Telechips and Nextchip are stronger.

2. Company overview and partnerships

| Item | Source content | Meaning |

|---|---|---|

| Name | BOS Semiconductors, “Best Of Silicon” | Semiconductor design for mobility innovation |

| Founded | May 13, 2022 | Still a fourth-year startup |

| Locations | Pangyo HQ, large R&D center in Ho Chi Minh City, Germany branch under preparation | Combines domestic design with global customer response |

| Vision | Developing Super SoCs for mobility innovation | Expansion from Level 2+ to Level 4 and into robots, drones, and other moving machines |

| CEO | Jae-hong Park, 23 years at Samsung Electronics, former System LSI VP and foundry design-service head | Tesla FSD chip, early iPhone AP, and Audi collaboration experience serve as trust assets |

Official fact: The source says the core research staff includes veteran engineers who designed mobile APs and automotive semiconductors at Samsung Electronics, LG Electronics, and others. The early Vietnam R&D center is framed as a strategy to ease Korea’s design-talent shortage and cost burden.

3. Financing and implications

| Round | Timing | Size | Main content |

|---|---|---|---|

| Seed / Pre-A | 2022-2023 | Estimated KRW 2bn+ | Hyundai/Kia ZER01 No. 2 fund, SAFE format |

| Series A | June 2024 | About KRW 20bn | Major Korean VCs and financial institutions |

| RCPS | July 2024 | KRW 14bn | Kolon Investment, Ace Suseong New Technology Investment Association, 891,717 shares at KRW 15,700/share |

Official fact: Based on the July 2024 RCPS issue price and share count, the source estimates the post-money valuation at about KRW 140bn-150bn.

Interpretation: The funds are for sub-5nm design, MPW prototype production, and payroll. For a semiconductor startup, financing is not just a balance-sheet event; it is the central variable in crossing the pre-mass-production “valley of death.”

4. Eagle roadmap and chiplet strategy

BOS’s product family is the Eagle series. The accelerator and integrated SoC can run separately or be combined through chiplet technology for higher performance.

| Product | Source figures/timeline | Role |

|---|---|---|

| Eagle-N | 250 TOPS; evaluation sample in April 2025; production preparation in 2026 | High-performance AI accelerator for Level 3+ autonomy, sensor fusion, and in-vehicle LLMs |

| Eagle-A | 150 TOPS; sample in Q1 2027; production planned for 2028 | All-in-one ADAS SoC integrating camera, LiDAR, and radar data |

| Eagle Chiplet System | Scalable from 400 TOPS to more than 800 TOPS | Combines Eagle-N and Eagle-A in a multi-chip package to address high-end chips such as Nvidia Thor |

5. Business model: Tier-0.5 and open ecosystem

Official fact: The source says BOS does not follow a traditional fabless model of handing chips to Tier-1 suppliers. It pursues a Tier-0.5 strategy by engaging directly with OEMs from the vehicle-planning stage and defining custom chips optimized for their software architecture.

Interpretation: Unlike a closed ecosystem such as Nvidia CUDA, BOS’s Open Chiplet Atlas work with Tenstorrent may appeal to OEMs that do not want to surrender too much control of the vehicle to a semiconductor supplier. The tradeoff is that this model requires both custom development capability and long-term support capacity.

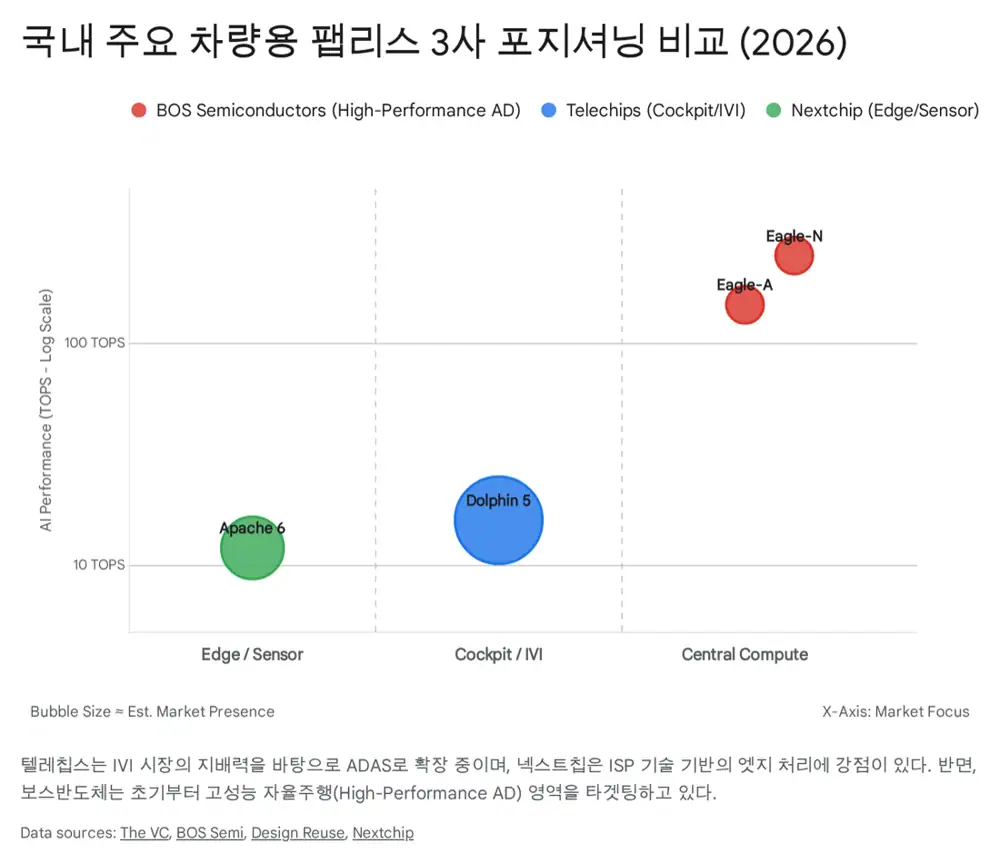

6. Competitive landscape

| Company | Source positioning | NPU/focus |

|---|---|---|

| Telechips | No. 1 Korean automotive semiconductor revenue company, strong in IVI, Dolphin 3 and Dolphin 5 | Dolphin 5 around 8 TOPS, cockpit and ADAS entry attempt |

| Nextchip | Camera-sensor strength based on ISP, Apache 6 | About 8-12 TOPS, edge object recognition |

| BOS | Targets high-performance central compute/HPC | Eagle-N 250 TOPS, autonomous-driving decision-making and LLM execution |

| Global majors | Nvidia, Qualcomm, Mobileye | Strong performance and ecosystems, but price, power, and OEM dependence are concerns |

Interpretation: The source argues that U.S.-China semiconductor conflict is making Western OEMs look for alternatives to cost-effective Chinese autonomous-driving chips such as Horizon Robotics. BOS is presented as a Korean mid-high segment candidate with lower geopolitical risk and more reasonable price/power efficiency than Nvidia.

7. 2026-2028 growth scenario

| Year | Technology | Business/financials |

|---|---|---|

| 2026 | Eagle-N customer qualification completion; start of second-generation NPU architecture | Expected production-development contract beyond European OEM PoC, CES 2026 AI Box demo, KRW 30bn-50bn Series B financing push |

| 2027 | Eagle-A sample release and customer distribution; RISC-V next-generation core review with Tenstorrent | European revenue visibility via Germany branch, defense/drone AI module revenue based on LIG Nex1 cooperation, white-label SoC talks with Tier-2 OEMs |

| 2028 | Mass-production vehicle launch using the Eagle series, SOP | Full hardware revenue, turnaround and IPO attempt, Korean fabless unicorn goal |

8. Risks

- Financial valley of death: before 2028 mass production, BOS must spend hundreds of billions of won on payroll, EDA tools, and prototype production without major revenue.

- Additional financing: despite 2024 KRW 20bn financing and KRW 14bn RCPS, one 5nm mask can cost tens of billions of won, so Series B success matters.

- Automotive certification: standards such as ISO 26262 are demanding, and a delay of six months or more for Eagle-N could affect target vehicle schedules and contracts.

- Chiplet ecosystem: UCIe is still early, so packaging yield and thermal issues can undermine mass-production cost assumptions.

- Competitive response: Nvidia’s mid-low-end lineup expansion or an early 5nm high-performance Telechips chip supported by Samsung Foundry could narrow BOS’s position.

9. My conclusion

BOS is a rare startup combination, captured in the source phrase: “Samsung Electronics design DNA, Jim Keller’s architecture vision, and Hyundai’s proof stage.” Still, it is not yet a company with mass-production revenue proven in numbers. From an investment lens, the key is not the technology narrative alone but the execution chain: Eagle-N validation, European OEM production contract, KRW 30bn-50bn Series B, and 2028 SOP.

Sources

- Source 1: Naver Blog original