DEEP RESEARCH · LigaChem Biosciences

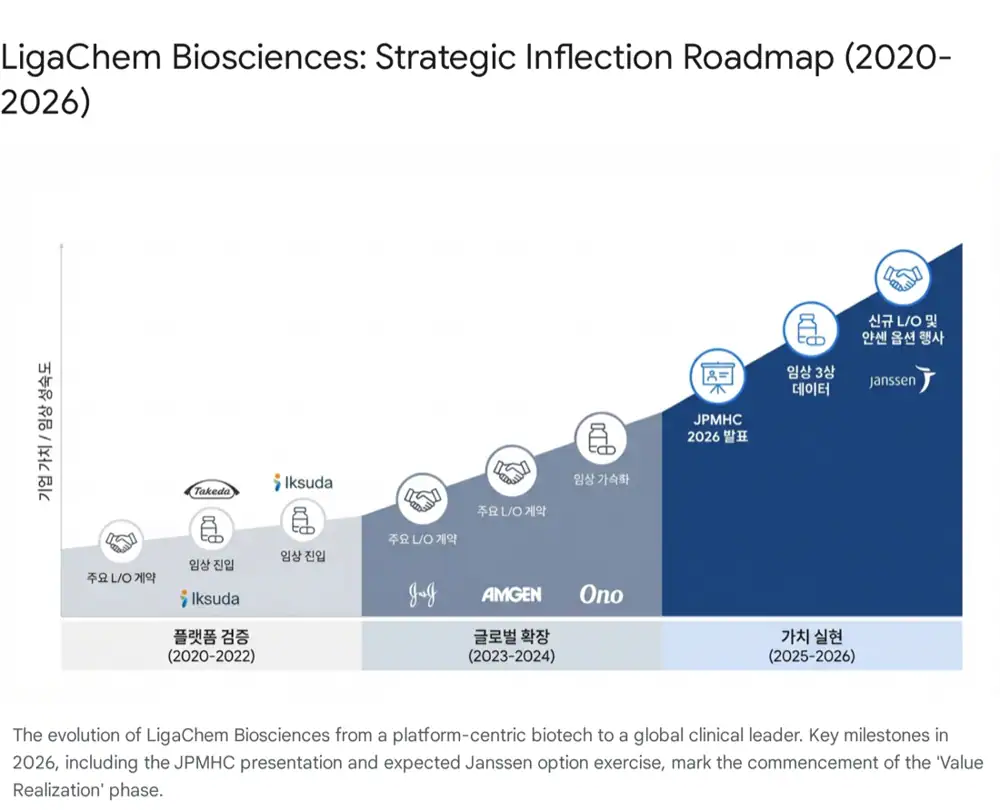

LigaChem: From Platform Provider to Global Biotech

JPMHC 2026, the ConjuALL™ platform, and the 2026 Janssen / Ono / Iksuda milestones

0. Bottom line first

Backed by its site-specific, high-stability ConjuALL™ ADC platform, LigaChem formally pivoted at JPMHC 2026 from “platform provider” to “global big biotech with its own clinical capabilities.” The three key 2026 catalysts are ① Janssen exercising the LCB84 sole-development option (~USD 200M), ② Fosun’s LCB14 China Phase 3 readout, and ③ Iksuda’s 80% clinical-benefit Phase 1 data in esophageal cancer expanding to new indications.

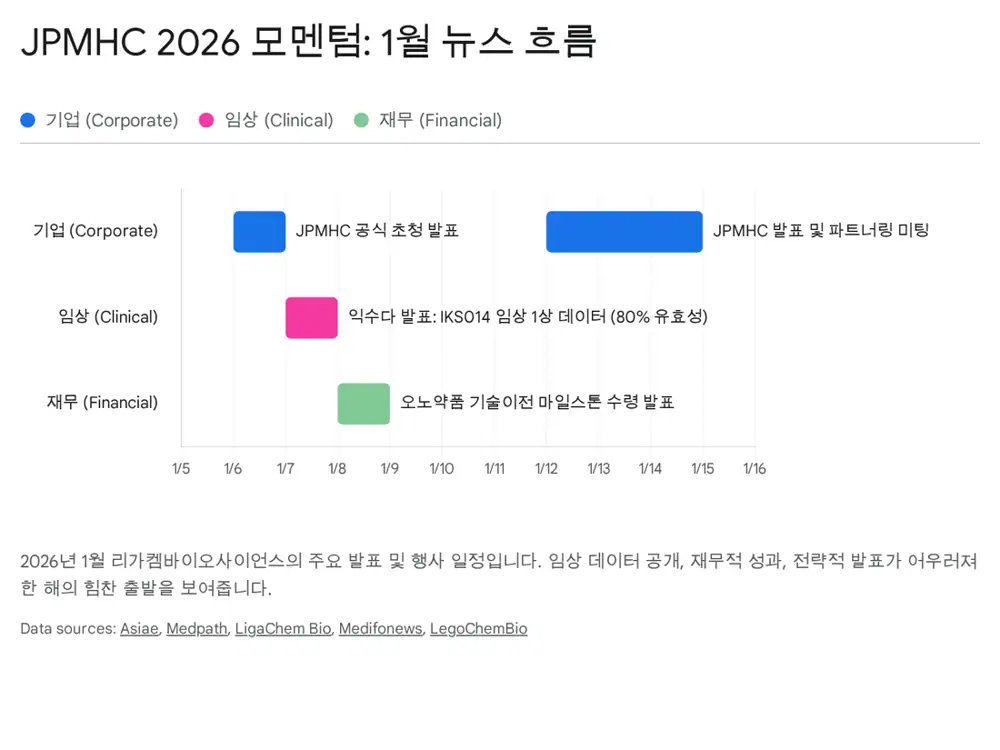

Official fact: On Jan 6, 2026, LigaChem was confirmed as an officially invited company at the 44th JPMHC. Asia Economic Daily, LigaChem press release.

Official fact: On Jan 8, 2026, the company received a development milestone from Ono Pharmaceutical — within ~3 months of the Oct-2024 deal. KBR, ChosunBiz.

1. JPMHC 2026: ‘Technology to Reality’

From Jan 12–15 2026 in San Francisco, the 44th JPMHC convened 8,000+ pharma-bio professionals. As an officially invited company, LigaChem (COO Sejin Park) presented around three axes:

Platform validated in humans

Iksuda (LCB14), Fosun (LCB14), CStone (LCB71) data prove plasma stability and safety.

Post-Enhertu payload

Disclosed a next-gen payload for DXd (Topo-I) resistant patients — strong big-pharma interest.

Multi-target L/O

L/O talks on LCB02A (Claudin 18.2), LCB39 (STING agonist), plus multi-target platform deals.

Official fact: On Jan 7, 2026, Iksuda reported ~80% clinical benefit in the global Phase 1 of IKS014 (LCB14) in esophageal cancer. Given limited options for this hard-to-treat tumor, it’s a defining data point for LCB14’s ‘Post-Enhertu’ positioning.

2. ConjuALL™ — the platform moat

2.1 Site-specific conjugation

Early ADCs (e.g., Kadcyla) used stochastic conjugation, causing DAR heterogeneity and either over-toxicity or under-efficacy. ConjuALL™ uses a CAAX motif enzymatic approach to uniformly control DAR at 2 or 4, improving PK predictability and dramatically widening the therapeutic index.

2.2 Stable linker + tumor-specific release

The beta-glucuronide linker is highly stable in plasma but cleaves only when it meets beta-glucuronidase that is overexpressed in tumor lysosomes. This is the structural reason for the strong safety profiles observed in LigaChem’s ADC clinical trials.

3. Pipelines and 2026 watch points

3.1 LCB84 (TROP2-ADC) — the Janssen big deal

- Partner: Janssen (J&J); total up to ~USD 1.7B (Dec 2023). BioSpectrum Asia

- Status: US Phase 1/2. Competitors: Gilead Trodelvy, AZ/Daiichi Dato-DXd.

- Differentiator: targets the cleaved form of TROP2 — avoids normal cells. AACR 2022 poster

- 2026 trigger: Janssen exercising the sole-development option → ~USD 200M (~KRW 260B) for LigaChem. The biggest single re-rating catalyst.

3.2 LCB14 (HER2-ADC) — Post-Enhertu leader

- Partners: Fosun Pharma (China), Iksuda (global). China Phase 3 (breast); global Phase 1b.

- Differentiator: no ILD or ocular toxicity reported (vs Enhertu).

- 2026 triggers: ① Fosun Phase 3 readout (H2 2025–early 2026); ② Iksuda esophageal cancer expansion to gastric/other tumors. LARVOL DELTA — caxmotabart entudotin (IKS014)

3.3 LCB71 (ROR1-ADC) — solid-tumor FIC ambition

- Partner: CStone. Status: global Phase 1b.

- Edge: while MSD’s zilovertamab vedotin underperformed in solid tumors, LCB71 uses a PBD prodrug payload that could become the first ROR1 ADC effective in solid tumors.

- 2026 trigger: a global partnership or pivotal-trial entry.

3.4 LCB97 (L1CAM-ADC) & new assets

- Partner: Ono Pharma; ~USD 700M deal; first milestone received in Jan 2026.

- New: LCB02A (Claudin 18.2), LCB39 (STING agonist) — clinical entry / L/O candidates in 2026.

4. Financial structure and valuation

4.1 Liquidity / Runway

- Cash + short-term financial assets >KRW 550B at end-3Q25.

- Janssen $100M upfront + Orion rights-issue proceeds.

- Annual R&D ~KRW 130B → 3–4 years of independent clinical runway without external funding → strong negotiating leverage.

4.2 Convertible bond (CB) overhang

Interpretation: Above strike, conversions dilute shares but also turn debt into equity — improving the balance sheet. With ample cash, there’s no repayment pressure, so dilution risk is contained.

4.3 Quality of earnings

- Janssen $100M upfront — recognized ratably, creating a quarterly revenue base.

- Milestone stacking across Ono/Janssen/Iksuda/Fosun reduces volatility and improves visibility.

5. Appendix — Major out-licensing deals (cumulative > $8.3B)

| Signed | Partner | Asset / Tech | Region | Notes / Status |

|---|---|---|---|---|

| 2024.10 | Ono Pharma | LCB97 + platform | Global | L1CAM target; milestone in Jan 2026 |

| 2023.12 | Janssen (J&J) | LCB84 (TROP2) | Global | Up to $1.7B; sole-development option pending |

| 2022.12 | Amgen | ADC platform | Global | Platform license, 5 targets |

| 2021.12 | Iksuda | ADC platform | Global | Long-term partnership, multiple pipelines |

| 2021.11 | Sotio | ADC platform | Global | European market foothold |

| 2020.10 | CStone | LCB71 (ROR1) | Global | Efficacy in solid/heme tumors |

| 2015.08 | Fosun Pharma | LCB14 (HER2) | China | Phase 3 advancing, commercialization imminent |

6. 2026 takeaways for investors

- Safety moat: Best-in-class safety while competitors struggle with ILD/ocular toxicity.

- Janssen option exercise: ~USD 200M cash plus a clear re-rating trigger.

- Milestone flywheel: Less single-event dependency; recurring cash from multiple partners.

2026 is plausibly the pivot from tech-out-licensing to a royalty-collecting, internally-developing global biopharma. The signal is the deal flow and clinical data — not the short-term share price.

Sources

- Naver blog source: m.blog.naver.com/.../224144164958

- JPMHC 2026 invitation: Asia Economic Daily

- JPM 2026 partnership push: ChosunBiz

- LigaChem release: ligachembio.com

- JPMHC invitation: The Bio News

- Ono milestone (KBR): koreabiomed.com

- Ono milestone (MedPath): MedPath

- Ono milestone (ChosunBiz): ChosunBiz

- ADC overview: NJ Bio

- J&J $1.7B deal: BioSpectrum Asia

- LCB84 AACR 2022 poster: PDF

- LCB84 LARVOL DELTA: delta.larvol.com

- Mirae Asset report: PDF

- IKS014/LCB14 LARVOL DELTA: delta.larvol.com

- LigaChem press list: ligachembio.com