DEEP RESEARCH · REIT/NH ALL-ONE REIT

NH All-One REIT: Strategic Alpha in the Seocho Corridor

Assessing whether the HiteJinro Seocho office acquisition and Yangjae-Seoripul development can drive NAV rerating

0. Bottom line first

The source reframes NH All-One REIT as a strategic deep-value play with a call option on the Seoripul mixed-use development, not just a dividend REIT. The argument is that the current price around KRW 3,400 and P/NAV of about 0.44x do not fully reflect the location change and long-term cash flow of the HiteJinro Seocho office acquired in May 2025.

I see two core points. First, the HiteJinro Seocho office is protected by a 100% master lease through June 2032 and 2.5% annual rent escalation. Second, if Seoripul/Yangjae development and GTX-C materialize, the cap rate for this secondary Seocho office zone could compress and NAV could rerate.

1. Seoripul-Yangjae renaissance: urban planning changes the board

Official fact: The source says Seoul's 2040 Plan points to the Seocho-Yangjae axis as a spatial outlet for a saturated Gangnam Business District. Yangjae and Seoripul are discussed as an R&D innovation district, extending GBD functions west and south.

- The Seoripul greenbelt release is described as the first large urban-core greenbelt release in Seoul in 12 years.

- Public housing supply is presented at about 20,000 units.

- FAR is being considered at 250-300%, with more than 400% possible for high-density station-area development.

- A dense 20,000-home residential district is framed as worker housing for the R&D cluster and as support for retail and office demand.

2. Anchor projects and transport infrastructure

Former intelligence-command site

Seocho-dong 1005-6 area. The source says MDM bought about 91,000 sqm for more than KRW 1 trillion and is developing an eco-friendly office complex with about 350,000 sqm of GFA.

About 1,700 pyeong per floor

Unlike high-rise Teheran-ro towers, the low-rise broad floor plates target global big-tech and biotech R&D demand.

Yangjae high-tech logistics complex

Former freight-terminal site at Yangjae-dong 225. The source describes a project approaching KRW 7 trillion in total cost, with 2025 start visibility and 2030 completion target.

Yangjae transfer axis

The practical opening target is late 2028. Yangjae Station could become an integrated transfer hub for GTX-C, Line 3, Shinbundang Line, and more than 100 bus routes.

The HiteJinro Seocho office is located at Seocho-dong 1445-14. The source places it between MDM's former intelligence-command project to the north and Harim's former Yangjae freight-terminal project to the south, at a node connecting Seochojungang-ro and Banpo-daero. It is one subway stop from Yangjae Station and within five minutes by car via Seochojungang-ro.

3. HiteJinro Seocho office: defensive quality of the acquired asset

Official fact: NH All-One REIT acquired the HiteJinro Seocho office through NH No. 9 REIT in May 2025. The address is 14 Seochojungang-ro, Seocho-gu, Seoul. The building has three basement floors and 18 above-ground floors, total floor area of about 8,295 pyeong (27,421 sqm), and was acquired for about KRW 240 billion, or roughly KRW 29 million per pyeong.

| Item | Source detail | Meaning |

|---|---|---|

| Main tenant | HiteJinro, credit rating A+ | Creditworthy single-tenant base |

| Lease structure | 100% master lease | Materially lowers vacancy risk |

| Lease term | Until June 2032 | Cash-flow visibility through the Seoripul development period |

| Rent terms | 2.5% fixed annual increase | Built-in inflation hedge |

| Ownership form | Floors 6-17 and parking share | Lower floors are owned by others, but core office floors are held |

Interpretation: The KRW 29 million-per-pyeong acquisition price is compared in the source with GBD core transactions above KRW 40 million per pyeong and landmark assets near KRW 50 million. The condition for closing that gap is not just the building itself, but a district reclassification from “old Seocho office” to “core office in a Gangnam innovation district.”

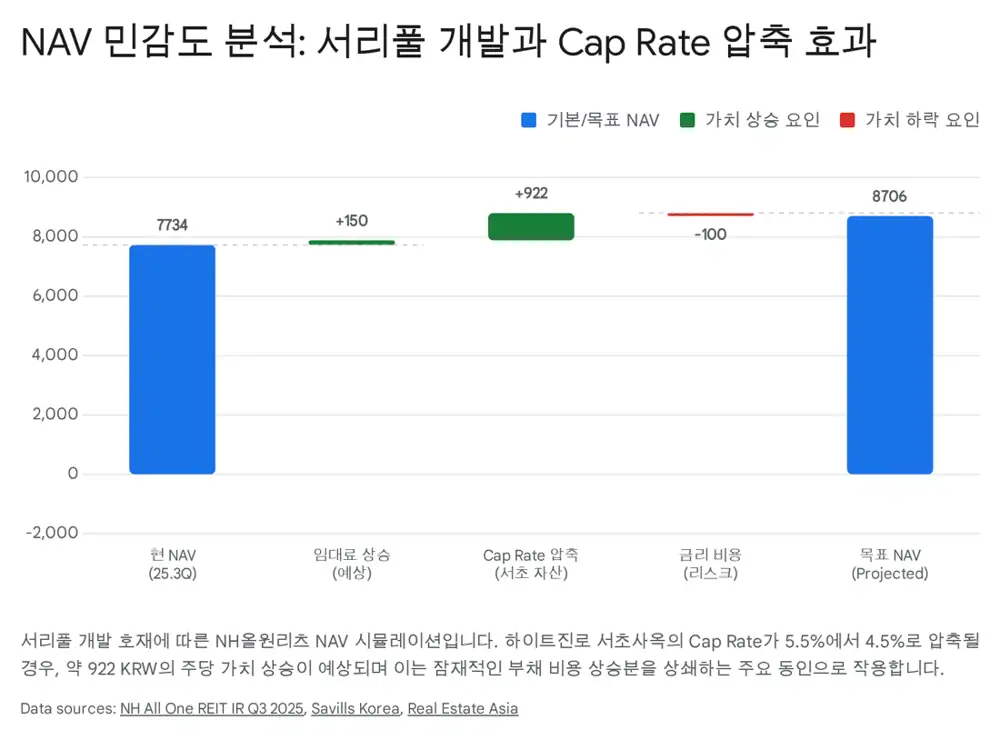

4. NAV simulation: rent and cap rate

The source simulates NAV change around 2028-2030, when Seoripul development and GTX-C are targeted to be complete. The current lease has fixed 2.5% annual increases, so market rent increases do not flow through immediately, but future reversion matters for appraisal and NAV.

- Current effective office rent near Seocho-dong and Nambu Terminal is described at about 70-80% of Teheran-ro core rent.

- Assuming conservative market-rent CAGR of 4-5%, the source sees more than 30% upside in rent by the 2032 renewal point.

- The current cap rate for Seocho and other secondary GBD zones is estimated at about 4.5-5.0%.

- If the area becomes a GBD core-expansion zone after development visibility, the appropriate cap rate for the HiteJinro Seocho office could compress below 4.0%.

- NH All-One REIT uses about 63% LTV, so a 10% increase in asset value can lift equity NAV by about 27%.

- If the cap rate falls by 0.5 percentage points, the source sees structural potential for per-share NAV to rise from the KRW 7,000 range to above KRW 9,000.

5. Risks: refinancing and oversupply

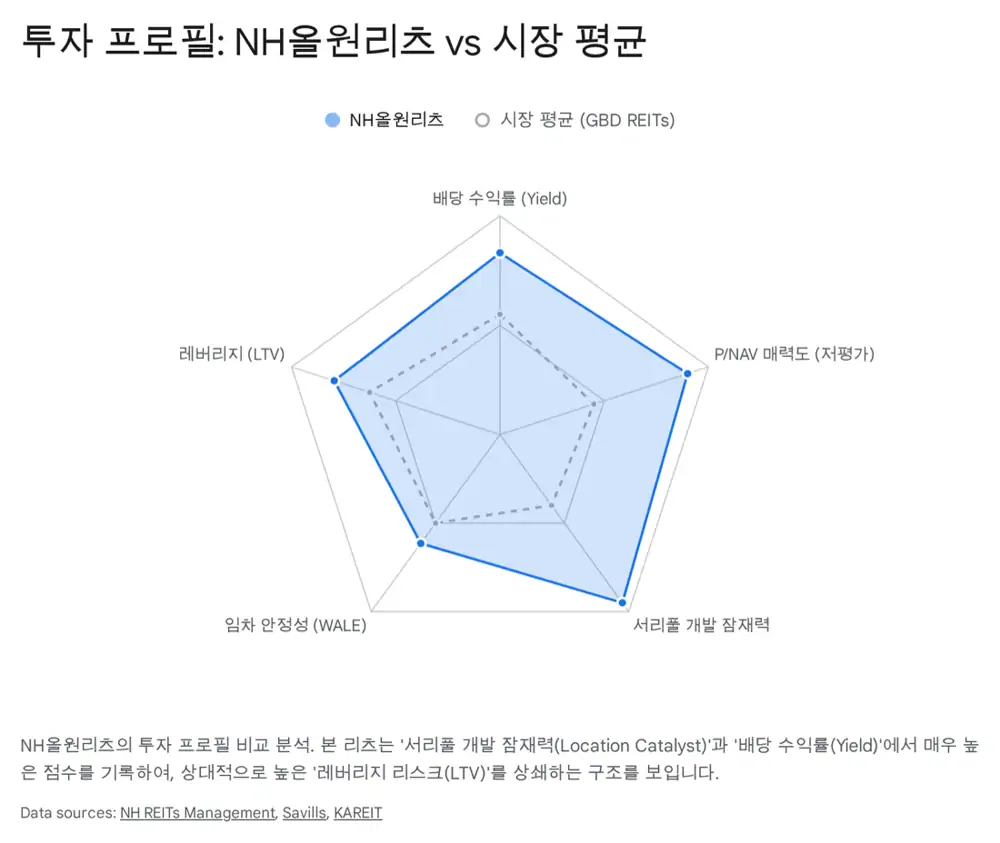

For a REIT, rates and vacancy are the key variables. The source acknowledges NH All-One REIT's 63.6% LTV as the main concern, but argues that the rate-cut cycle began at the end of 2024 and that major 2025 debt maturities were refinanced, moving risk from crisis to management mode. The current weighted-average interest rate is presented at about 4.32%.

Oversupply

When MDM and Harim projects complete around 2028-2030, major new office supply in Seocho and Yangjae could pressure rents.

Supply-induced demand

The source says current GBD vacancy is in the 1% range, implying demand is constrained by lack of space and new supply can expand the market.

Master lease to 2032

The HiteJinro office is master-leased through 2032, allowing it to maintain contracted cash flow while new buildings fill up.

6. Scenario target prices and final view

| Scenario | Macro backdrop | Seoripul development | Cap rate | Target price/NAV |

|---|---|---|---|---|

| Bear | Rates stuck above 4%, stagflation | Harim/MDM projects delayed more than three years | 5.5% | KRW 3,000. Asset value stagnates, only pure dividend appeal remains |

| Base | Rates stabilize around 3%, moderate growth | Main projects stay on schedule, 2028-2030 completion | 4.5% | KRW 4,200. Dividend appeal rises with lower rates and NAV increases moderately |

| Bull | Rates fall below 2.5%, tech-company demand surges | MDM pre-leasing completes early and GTX-C opens on schedule | 3.8% | KRW 5,500+. GBD core-zone inclusion and cap-rate compression |

Official fact: The source presents the late-October 2025 price at about KRW 3,395, P/NAV at about 0.44x, and expected dividend yield around 7-8%.

The final view is Overweight. The source emphasizes a three- to five-year horizon looking past near-term price swings toward post-2028 urban change. My checklist is actual refinancing rates, MDM and Harim project schedules, Yangjae GTX-C progress, and how much market rent catches up by the 2032 renewal.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224142965713

- Seoul Economic Daily Seoripul FAR article: https://www.sedaily.com/NewsView/2GU4U0JZQN

- Civil Engineering News Seoripul district article: http://m.cenews.co.kr/news/articleView.html?idxno=18028

- Seocho-gu district-unit planning board: https://www.seocho.go.kr/site/seocho/ex/bbs/View.do?cbIdx=272&bcIdx=340752

- Yangjae-Seoripul corporate land-ownership map: https://drive.google.com/open?id=1IDAG6cHvKi-fIh_KWtyYm1q2mkBZWNOb6mfHz5vRnWI

- Corebeat MDM office-sale article: https://www.corebeat.co.kr/article/756

- Dealsite Harim Yangjae logistics article: https://dealsite.co.kr/articles/148096

- Chosun Ilbo Harim KRW 7tn project article: https://www.chosun.com/economy/real_estate/2025/10/15/NQRQ75VPMBHSHNW7KJ4C436X7Q/

- NamuWiki GTX-C: https://namu.wiki/w/%EC%88%98%EB%8F%84%EA%B6%8C%20%EA%B4%91%EC%97%AD%EA%B8%89%ED%96%89%EC%B2%A0%EB%8F%84%20C%EC%84%A0

- Atlas News Yangjae transfer-core article: http://www.atlasnews.co.kr/news/articleView.html?idxno=10515

- NH All-One REIT notice: https://www.nhallonereit.com/ir/news.php?ptype=view&code=news&idx=407&category=

- Real Estate Asia Seoul office transaction article: https://realestateasia.com/commercial-office/news/seouls-2025-office-transaction-volume-track-surpass-2021-peak

- Gangnam/Seocho commercial-property report: http://www.wonkwangvalve.com/g5/bbs/board.php?bo_table=customer_en&wr_id=1897&sst=wr_hit&sod=desc&sop=and&page=128

- Savills 2025 Korea Office Market Outlook: https://pdf.savills.asia/asia-pacific-research/asia-pacific-research/2025-korea-office-market-outlook-en.pdf

- SPI Seoul office leasing-market article: https://seoulpi.io/article/00502765682863169536