DEEP RESEARCH · CAMECO

Cameco (CCJ): Nuclear Security Premium and the Westinghouse Option

A unified investment frame for AI power demand, U.S. energy-dominance policy, uranium scarcity, and the Westinghouse AP1000 pipeline

0. Bottom Line First

My core view on Cameco is that it is no longer just a uranium miner; it is a strategic asset exposed to the Western nuclear supply chain and AI power infrastructure at the same time. The source presents a January 2026 “Strong Buy” view and a 12-month target above $125, but the actual investment judgment needs uranium prices, Westinghouse project wins, and mining operating risk analyzed together.

- Cameco owns ultra-high-grade uranium mines such as McArthur River and Cigar Lake, and with Brookfield owns Westinghouse, creating an integrated nuclear value-chain profile.

- The late-2025 $80 billion strategic partnership among the U.S. government, Brookfield, Cameco, and Westinghouse is presented as the key catalyst for AP1000/AP300 deployment.

- The source says Meta is pursuing up to 6.6GW of nuclear power by 2035, Amazon has a 1.9GW PPA with Talen Energy, and Microsoft has a 20-year PPA with Constellation.

- Kazatomprom's 10% production-guidance cut for 2026, declining secondary supply, and reduced reliance on Russian enrichment strengthen a supplier-driven uranium market.

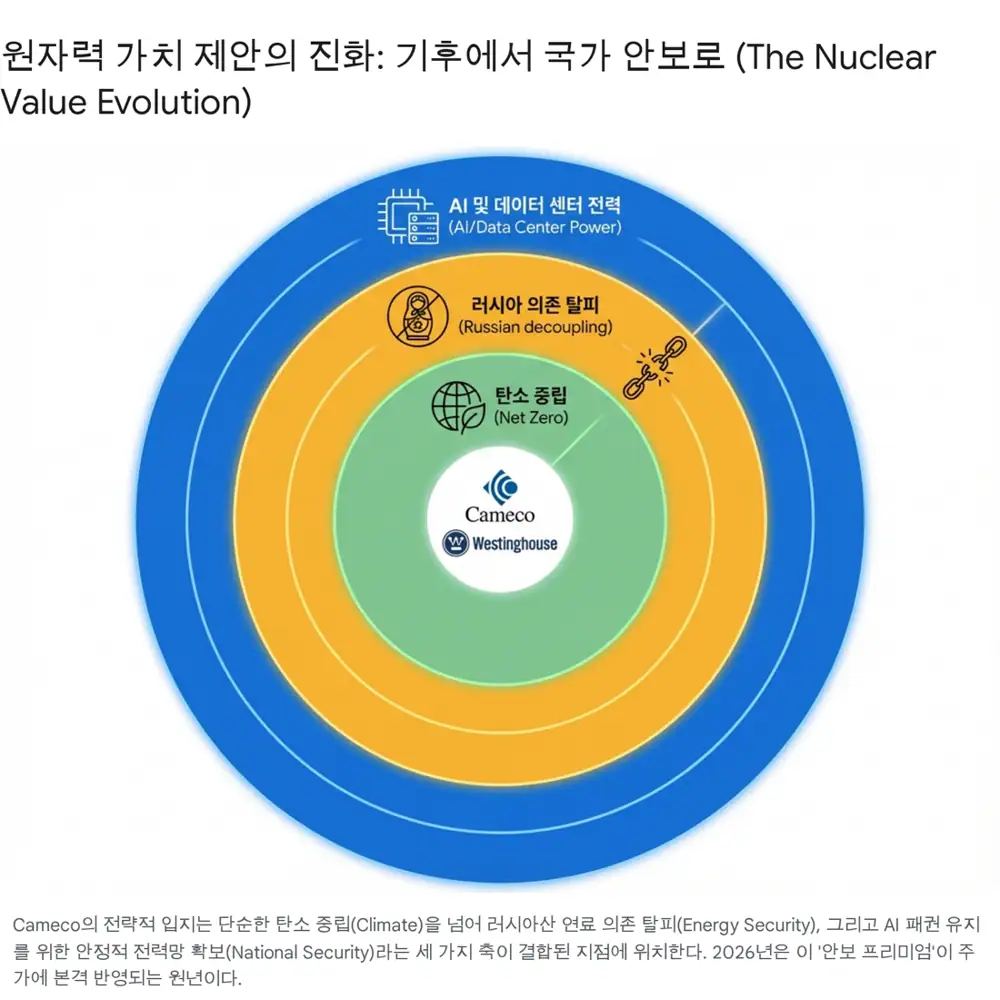

1. Paradigm Shift: Nuclear Moves From Climate Theme to Security Infrastructure

Official fact: The source says Cameco COO Grant Isaac defined nuclear power as a “fully emerged national security solution” at the Goldman Sachs Energy, CleanTech & Utilities Conference in January 2026.

In the past, the nuclear investment case was mostly about decarbonization and climate policy. The source argues that after the Russia-Ukraine war, energy security, and then AI data-center power demand, lifted nuclear power into the realm of national technology competitiveness and security. That shift supports valuing Cameco less like a traditional mining company on P/NAV and more like a strategic infrastructure and technology company on EBITDA multiples.

Interpretation: Grant Isaac's “3S strategy” of Standardize, Sequence, and Simplify is an execution model for avoiding the construction delays and budget overruns that hurt previous nuclear projects. The source reads it as support for Westinghouse AP1000's modular-construction advantage.

2. Macro: Energy Dominance and AI Data Centers

EDFO and $250B Limit

The source says DOE's LPO has been reshaped into the Energy Dominance Financing Office, with a loan ceiling expanded to $250 billion.

100GW in 2026-2030

Roughly 100GW of new global data-center capacity is expected, about twice current capacity according to the source.

De-Russianizing Nuclear Fuel

Because Russia has held about 40% of global enrichment services, bans and replacement sourcing can lift Western nuclear-fuel pricing.

| Company | Partner | Nuclear power detail in source |

|---|---|---|

| Meta | Vistra, TerraPower, Oklo | Up to 6.6GW of nuclear power by 2035, including SMR and large reactors |

| Amazon (AWS) | Talen Energy | Data center adjacent to the Susquehanna nuclear plant and a 1.9GW PPA |

| Microsoft | Constellation Energy | 20-year PPA tied to restarting the Crane Clean Energy Center, formerly TMI-1 |

| Multiple SMR developers and utilities | The source describes discussions with a possible official announcement approaching |

AI data centers require uninterrupted power 24 hours a day, 365 days a year. The source argues that once ESS costs are included, nuclear power emerges as the most economic and reliable option. That demand supports life extensions for existing plants, new large nuclear builds, and SMR development at the same time.

3. Uranium Balance: Numbers Behind the Structural Deficit

Official fact: Kazatomprom lowered its 2026 production plan by 10% versus the original target, which the source interprets as more than 3,000 tons of uranium disappearing from the market.

The supply issues include sulfuric-acid shortages, delays in materials and equipment for new deposits, and shortages of skilled labor. NexGen Energy's Rook I had completed federal environmental-assessment technical review by early 2026 but still required final permits and construction decisions, while Paladin Energy's Langer Heinrich ramp-up is not enough to fill the market gap, according to the source.

| Category | 2024E | 2026E | 2028E | 2030E | Note |

|---|---|---|---|---|---|

| Total demand | 195 Mlbs | 205 Mlbs | 220 Mlbs | 240 Mlbs | Could be revised up with AI power demand |

| Primary supply | 155 Mlbs | 165 Mlbs | 175 Mlbs | 185 Mlbs | Reflects Kazatomprom cuts and new-project delays |

| Secondary supply | 25 Mlbs | 20 Mlbs | 15 Mlbs | 10 Mlbs | Declines as inventories are depleted |

| Balance | -15 Mlbs | -20 Mlbs | -30 Mlbs | -45 Mlbs | Deepening structural deficit |

Interpretation: The important point is the source's claim that utilities are no longer buying only for consumption, but are competing to build security stock. That kind of demand is less price-elastic and can pull long-term contract prices upward.

4. Cameco's Moat: Ore Grade and Contract Structure

| Asset or strategy | Source figure | Investment meaning |

|---|---|---|

| McArthur River | Average grade about 16% U3O8 | Massively higher than ordinary mines at 0.1-1.0% |

| Cigar Lake | Average grade about 15% U3O8 | Basis for low cost and high margins |

| Production cost | Estimated $20-$30/lb | Margin cushion versus spot prices above $80 |

| Supply discipline | About 30% of capacity idle | Strategic reserve and price-support tool |

| Long-term contracts | Floor in the mid-$70s, ceiling up to $150 | Protects downside while keeping upside to uranium price strength |

The source describes Cameco's marketing strategy as “value over volume.” Grant Isaac's comment that the midpoint of these contracts already points to triple digits, meaning $100 or more, signals supplier bargaining power in long-term pricing.

Fuel services are another hidden cash generator. Port Hope is one of the few commercial conversion facilities in the Western world, and the source argues its strategic value rises as Russian enriched uranium is banned and conversion bottlenecks deepen.

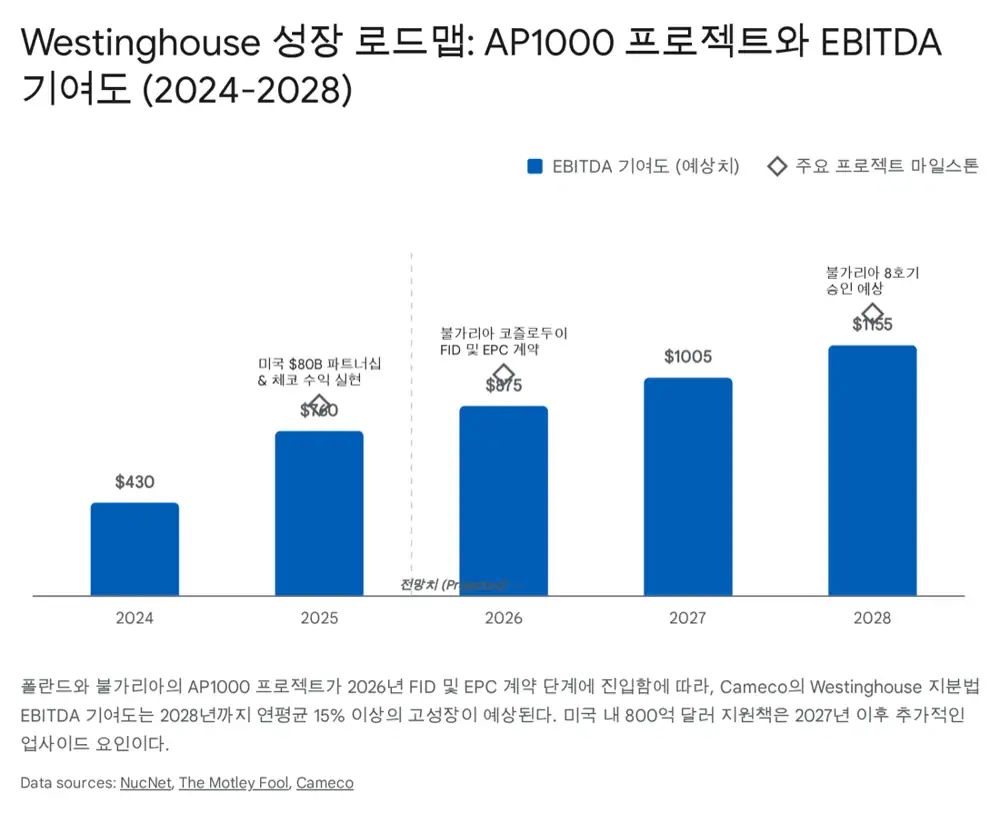

5. Westinghouse: The $80 Billion Momentum

Official fact: The source says Cameco and Brookfield Renewable Partners jointly acquired Westinghouse Electric Company in 2023, with Brookfield holding 51% and Cameco 49%.

Westinghouse changes Cameco from a uranium supplier into an integrated nuclear-solutions company spanning reactor technology, fuel fabrication, and maintenance. The late-2025 strategic partnership among the U.S. government, Brookfield, Cameco, and Westinghouse targets at least $80 billion of new reactor construction, with AP1000 and AP300 as the central technologies.

Financial Support

EDFO low-rate loan guarantees, ITC/PTC tax credits, and direct grants are meant to reduce upfront construction cost.

Standardization and Permits

Standardized design approval is intended to shorten permitting and construction timelines, reinforcing the 3S strategy.

Eastern Europe Projects

Poland's three AP1000 units, Bulgaria's Kozloduy 7 and 8, and Ukraine's nine AP1000 plan form a long-term pipeline.

AP1000 is a Generation III+ reactor with passive safety systems, meaning the source says it can cool using natural forces such as gravity and convection without external power or operator intervention. Commercial operation at Vogtle, Sanmen, and Haiyang is presented as a competitive advantage among Western Generation III+ designs. eVinci, a container-sized microreactor, is framed as a future option for remote mines, military bases, and islands.

6. Financials, Valuation, and Risks

| Item | Source detail | Meaning |

|---|---|---|

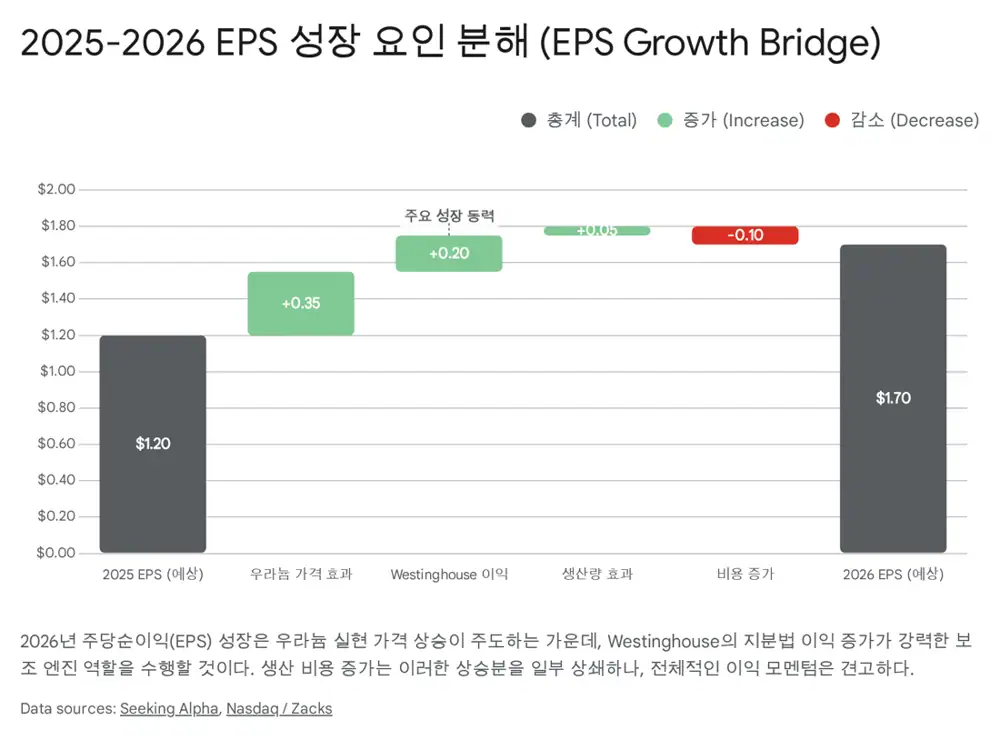

| Westinghouse adjusted EBITDA contribution in 3Q 2025 | $124M | Equity-method contribution becoming visible |

| Czech nuclear project cash inflow | $171.5M | Item supporting financial stability |

| 2026 revenue outlook | Above about CAD 3B | Repricing of legacy long-term contracts plus high-priced new contracts |

| 2026 adjusted EBITDA | Expected to grow more than 20% versus 2025 | Higher uranium margins plus growth in Westinghouse service revenue |

| Dividend | Raised 50% in 2025 | The source sees room for stronger shareholder returns in 2026 |

The valuation is expensive. The source says Cameco traded in January 2026 at about 69x 2026E P/E and about 98x versus 2025 earnings. That looks demanding on a miner-only basis, but the source argues SOTP is more appropriate because of Westinghouse technology and service value, Western energy-security premium, and AI data-center power demand.

The target-price frame is a 12-month consensus of $121.68 among major banks, with a bull-case possibility above $150. Risks include operating issues at Cigar Lake and McArthur River, partial loss of the security premium if Russia-Ukraine tensions ease, and nuclear-accident or regulatory risk. The key monitoring points are Westinghouse contract progress in Poland and Bulgaria, Kazatomprom's production recovery pace, and Cameco's mining ramp-up stability.

7. Final Read

Interpretation: Cameco sits where energy security, AI infrastructure, and supply-chain reshoring meet. But rather than treating the source's “must-own asset” conclusion as a direct buy signal, I would require long-term uranium pricing and Westinghouse wins to translate into actual numbers before fully justifying the high multiple.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224142791940

- Cameco Conference: COO Says Nuclear “Fully Emerged” as Security Play, $80B AP1000 Push in U.S. - MarketBeat: https://www.marketbeat.com/instant-alerts/cameco-conference-coo-says-nuclear-fully-emerged-as-security-play-80b-ap1000-push-in-us-2026-01-07/

- Goldman Sachs Energy Conference 2026: Nuclear Renaissance, AI Power Demand, and the New Energy Playbook | Fintool News: https://fintool.com/news/goldman-sachs-energy-conference-2026

- Strategic Partnership | Westinghouse Nuclear: https://westinghousenuclear.com/strategic-partnership/

- U.S., Westinghouse Ink $80 Billion Nuclear Deal - NAM: https://nam.org/u-s-westinghouse-ink-80-billion-nuclear-deal-35084/

- Meta goes all-in on nuclear power with 6.6 GW plans: https://www.fierce-network.com/cloud/meta-goes-all-nuclear-power-66-gw-plans

- Amazon, Talen Energy ink nuclear PPA to power data centers with carbon-free energy: https://www.esgdive.com/news/amazon-talen-energy-ink-nuclear-ppa-to-power-data-centers-pennsylvania/750950/

- Kazatomprom Eyes Fuel Cycle Expansion Beyond Mining Under 2034 Strategy, Says Expert: https://www.nucnet.org/news/kazatomprom-eyes-wider-expansion-beyond-mining-under-2034-strategy-says-expert-10-5-2025

- Kazatomprom to lower uranium production in 2026 - World Nuclear News: https://www.world-nuclear-news.org/articles/kazatomprom-to-lower-uranium-production-in-2026

- Cameco Corporation (CCO:CA) Presents at Goldman Sachs Energy, CleanTech & Utilities Conference Transcript | Seeking Alpha: https://seekingalpha.com/article/4857801-cameco-corporation-cco-ca-presents-at-goldman-sachs-energy-cleantech-and-utilities-conference

- Energy Infrastructure Reinvestment Financing: https://www.energy.gov/edf/energy-infrastructure-reinvestment-financing

- How the Loan Programs Office Became the Energy Dominance Financing Office: https://heatmap.news/energy/energy-dominance-financing-office

- Clean Energy Brief 11.21.25 - BGR Group: https://bgrdc.com/wp-content/uploads/2025/11/Clean-Energy-Brief-11.21.25.pdf

- DOE Rebrands Energy Infrastructure Reinvestment Program as Energy Dominance Financing Program | Norton Rose Fulbright: https://www.projectfinance.law/blog/2025/november/doe-rebrands-energy-infrastructure-reinvestment-program-as-energy-dominance-financing-program/

- Department of Energy Loan Guarantee Program Update: New Energy Dominance Financing Mechanism - Hunton Andrews Kurth LLP: https://www.hunton.com/insights/legal/department-of-energy-loan-guarantee-program-update-new-energy-dominance-financing-mechanism

- Interim Final Rule Announced: Changes from Energy Dominance Financing Provisions to Impact the Loan Programs Office - McAllister & Quinn: https://jm-aq.com/interim-final-rule-announced-changes-from-energy-dominance-financing-provisions-to-impact-the-loan-programs-office/

- 2026 Global Data Center Outlook - JLL: https://www.jll.com/en-us/insights/market-outlook/data-center-outlook

- Energy Department awards $2.7B for domestic uranium enrichment - POLITICO Pro: https://subscriber.politicopro.com/article/2026/01/energy-department-awards-2-7b-for-domestic-uranium-enrichment-00711201

- The Trump administration is moving towards nuclear autarky – Q1 2026 inflection point through Section 232 review : r/UraniumSqueeze - Reddit: https://www.reddit.com/r/UraniumSqueeze/comments/1q53gfr/the_trump_administration_is_moving_towards/

- Cameco, Kazatomprom Production Cuts Stoke Uranium Market Tightness | INN: https://investingnews.com/cameco-kazatomprom-uranium-production-cuts/

- Rook I Project - NexGen Energy Ltd.: https://www.nexgenenergy.ca/rook-1-project/

- Update on the Rook I Project - Canadian Nuclear Safety Commission: https://www.cnsc-ccsn.gc.ca/eng/about-us/media-centre/feature-articles/update-on-the-rook-i-project/

- Paladin raises equity to back Langer Heinrich 2026 ramp-up - The Extractor Magazine: https://theextractormagazine.com/2025/09/16/paladin-raises-equity-to-back-langer-heinrichs-2026-ramp-up/

- Paladin sets uranium production guidance for Namibia mine - Mining Weekly: https://www.miningweekly.com/article/paladin-sets-uranium-production-guidance-for-namibia-mine-2025-07-23

- AI boom set to turbocharge uranium demand in 2026: https://www.canadianminingjournal.com/news/ai-boom-set-to-turbocharge-uranium-demand-in-2026/

- Cameco and Brookfield establish transformational partnership with United States Government - Westinghouse Nuclear: https://westinghousenuclear.com/strategic-partnership/press-releases/cameco/

- Agreement extension enables continued development of Polish plant - World Nuclear News: https://www.world-nuclear-news.org/articles/agreement-extension-enables-continued-development-of-polish-plant

- Poland First Nuclear Plant Moves Forward with Westinghouse-Bechtel, PEJ Agreement: https://info.westinghousenuclear.com/news/polands-first-nuclear-plant-moves-forward-with-westinghouse-bechtel-pej-agreement

- Bulgaria Plans 2026 Final Investment Decision For Two New Kozloduy Units, Says Official: https://www.nucnet.org/news/bulgaria-plans-2026-final-investment-decision-for-two-new-kozloduy-units-10-5-2025

- Bulgaria Expects Final Investment Decision On Kozloduy In Second Half Of 2026 - NucNet: https://www.nucnet.org/news/bulgaria-expects-final-investment-decision-on-kozloduy-in-second-half-of-2026-12-2-2025

- Cameco Surges 99% in a Year: How to Play the Stock in 2026? | Nasdaq: https://www.nasdaq.com/articles/cameco-surges-99-year-how-play-stock-2026

- Research Update: Cameco Corp. Upgraded To BBB O | S&P Global Ratings: https://www.spglobal.com/ratings/en/regulatory/article/-/view/type/HTML/id/3449461

- Cameco stock maintains Buy rating at BofA amid dividend hike - Investing.com: https://www.investing.com/news/analyst-ratings/cameco-stock-maintains-buy-rating-at-bofa-amid-dividend-hike-93CH-4334217

- Cameco Corporation (CCJ) Stock Valuation Grade & Metrics - Seeking Alpha: https://seekingalpha.com/symbol/CCJ/valuation/metrics

- Cameco (CCJ) Stock Forecast and Price Target 2026 - MarketBeat: https://www.marketbeat.com/stocks/NYSE/CCJ/forecast/