DEEP RESEARCH · KUMHO PETROCHEMICAL/MDI

Kumho Petrochemical: North American LNG Supercycle and MDI Structural Turnaround

An energy-infrastructure materials thesis built on LNG insulation, MDI, and synthetic-rubber recovery amid NCC restructuring

Official fact: The source cites the Hana Securities energy/chemicals Telegram channel and report link https://bit.ly/4qjs3um.

0. Bottom line first

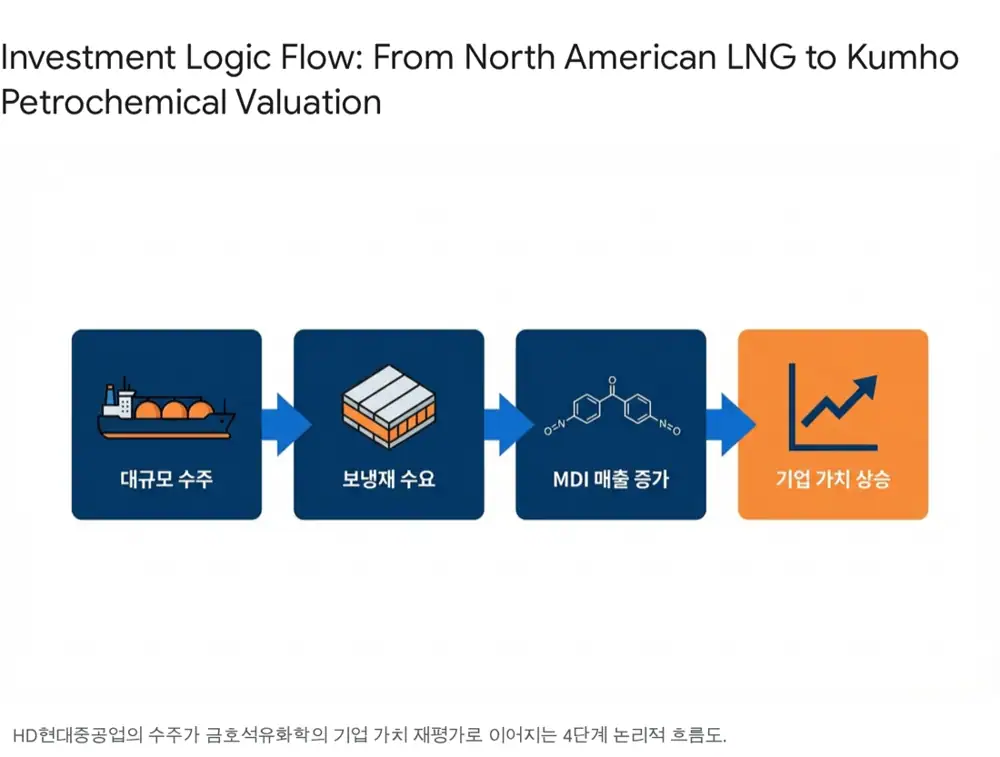

The source argues that Kumho Petrochemical should be reframed not as a commodity petrochemical stock but as a core LNG value-chain materials company. HD Hyundai Heavy Industries’ January 6, 2026 order for four LNG carriers from a North American shipowner, worth KRW 1.5T, is interpreted as a leading signal for North American LNG FIDs and future demand for MDI, the key input in cryogenic insulation.

Interpretation: The investment thesis has three pillars: the 2026 North American LNG cycle, synthetic-rubber recovery from butadiene tightness after NCC restructuring, and rising equity-method earnings from Kumho Mitsui Chemicals’ 710,000-ton MDI capacity.

1. North American LNG macro signal

Korea’s petrochemical industry is under structural pressure from rising Chinese self-sufficiency and weak global demand, forcing NCC-based companies into restructuring. The source argues that Kumho Petrochemical has differentiation through MDI and the LNG insulation value chain.

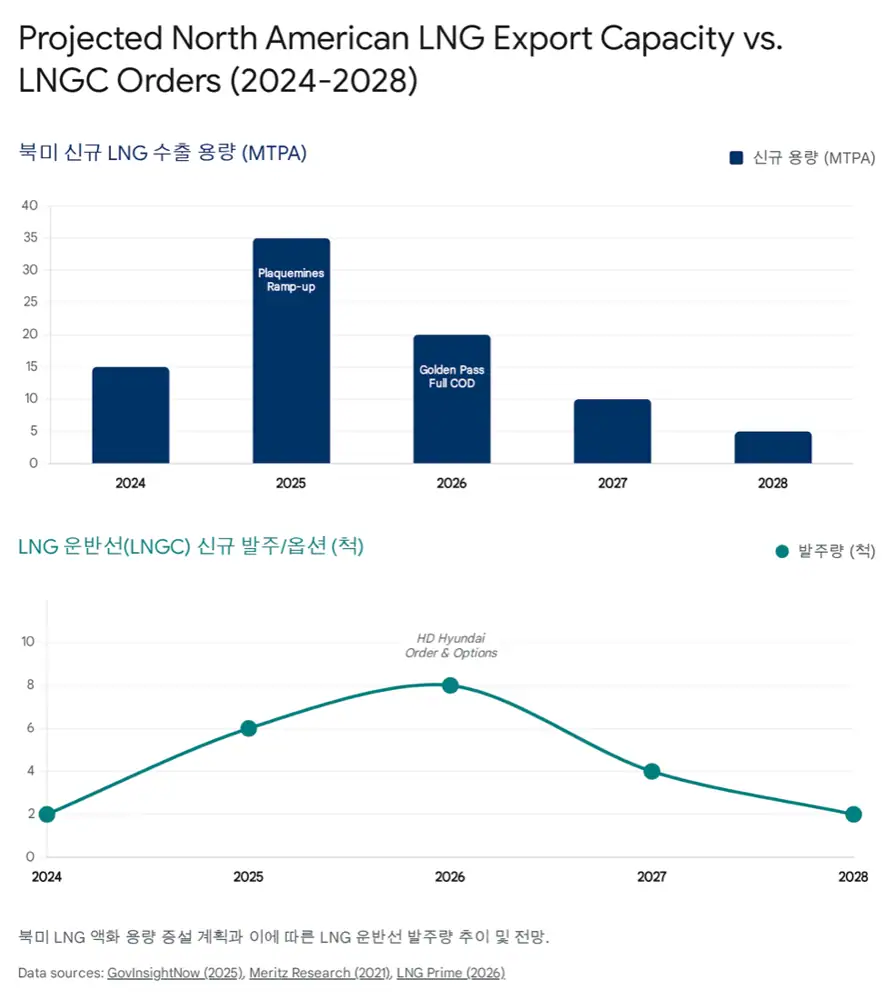

On January 6, 2026, HD Hyundai Heavy Industries under HD Korea Shipbuilding & Offshore Engineering disclosed an order for four LNG carriers from an Americas-based shipowner, worth KRW 1.5T, or about USD 1.04B. The per-ship price is about USD 260M. Because LNGC orders usually follow FID or long-term SPA visibility, the source reads the order as evidence that North American LNG projects are entering execution.

20 MTPA

First export in late 2024, commissioning through 2025, and full commercial operation in 2026-2027 are cited.

2027 target

Sempra’s Texas project is under construction after FID and targets operation around 2027.

FID complete

NextDecade’s Brownsville, Texas project has completed a large FID and entered construction.

Stage 3

Cheniere began additional production in late 2024 and is gradually expanding capacity.

After the Russia-Ukraine war, Europe reduced reliance on Russian pipeline gas and substituted LNG. The Trump administration’s 2025 “Drill, Baby, Drill” posture is presented as a policy tailwind for LNG export approvals and construction starts.

2. Cryogenic insulation and the MDI link

LNG is natural gas cooled to minus 163 degrees Celsius, reducing volume to one six-hundredth. The key is the cargo containment insulation system that blocks heat ingress and minimizes boil-off rate. If insulation fails, steel can face cryogenic brittleness, so insulation is a safety-critical component.

Among membrane cargo-containment systems used by Korean shipbuilders, GTT’s Mark III type uses reinforced polyurethane foam as its main insulation. Polyurethane foam is formed by reacting isocyanate and polyol, and MDI is the key isocyanate. LNG carriers require high-function polymeric MDI that withstands minus 163 degree contraction, sloshing impact, and flame-retardancy requirements.

The source says one 200,000 cbm class LNG carrier uses hundreds of tons of high-purity MDI. North American LNG expansion fills shipyard orderbooks, then leads with a lag to insulation orders for Korea Carbon and Dongsung Finetec, and ultimately to higher shipments and pricing for Kumho Mitsui Chemicals.

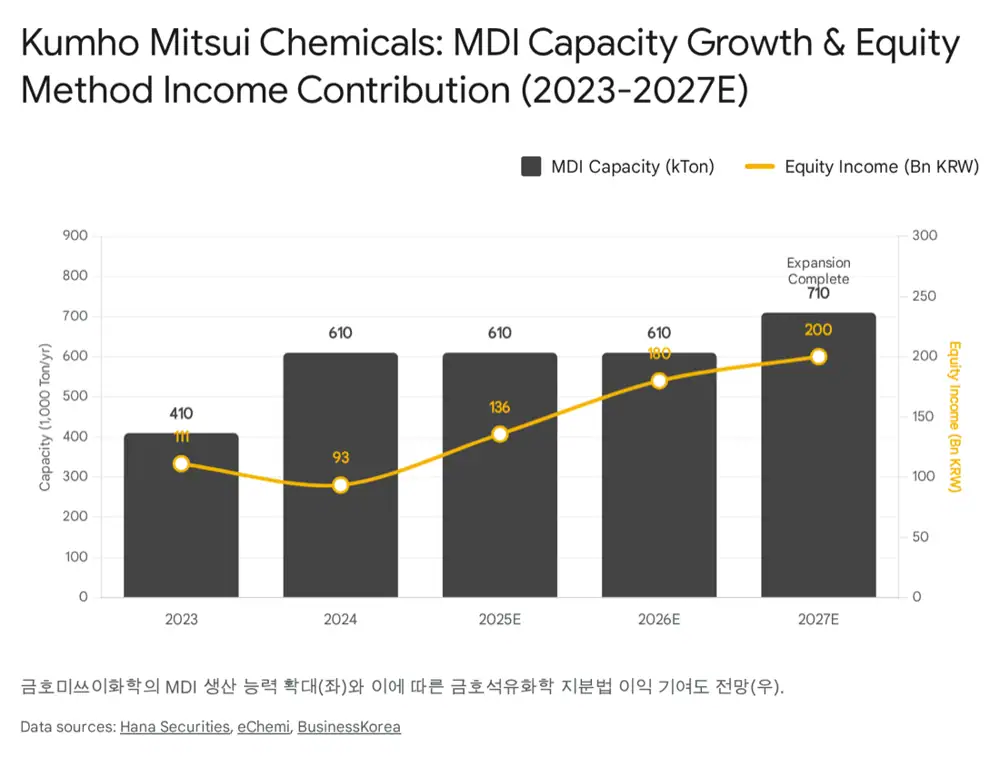

3. Kumho Mitsui Chemicals: MDI powerhouse

Kumho Mitsui Chemicals was founded in 1989 as a 50/50 joint venture between Kumho Petrochemical and Japan’s Mitsui Chemicals. It is accounted for as a joint venture, so half of its net income contributes to Kumho Petrochemical through equity-method income.

| Item | Source detail | Meaning |

|---|---|---|

| Existing capacity | 410,000 tons at end-2023 | Yeosu-centered MDI base |

| First expansion | 200,000-ton expansion completed in April 2024, total 610,000 tons | More supply for LNG and insulation demand |

| Additional expansion | KRW 140B investment approved at December 2025 EGM | Construction from February 2026, completion target May 2027 |

| Post-completion capacity | 710,000 tons | Targeting world-class single-site efficiency |

| Revenue impact | Expected annual revenue increase of about KRW 250B from the extra 100,000 tons | Capacity for 2026-2027 LNG insulation demand |

The MDI industry is described as an oligopoly where BASF, Covestro, Wanhua Chemical, Huntsman, Dow, and other majors control more than 90% of the market. Phosgene handling, technical difficulty, and upfront investment form entry barriers. MDI price hikes by major producers in Asia and Europe in November and December 2025 are read as a sign of operating leverage into 2026 demand recovery.

4. Synthetic-rubber turnaround and equity-method earnings

Kumho Petrochemical’s core SBR and BR products are tied to global tire demand. The source notes NCC restructuring in Asia and Europe due to Chinese ethylene oversupply, including discussion of up to 3.7 million tons of Korean NCC capacity reduction. Lower NCC operation and closures reduce butadiene supply, and BD is the key synthetic-rubber input.

Raw-material inflation is usually negative, but the source argues the SBR/BR market has little new capacity and solid tire-plant utilization, allowing pass-through of higher BD costs into rubber prices. EV growth also creates replacement demand for high-performance SSBR tires, and Kumho Petrochemical completed SSBR capacity expansion by end-2025.

| Equity-method income outlook | Source figure |

|---|---|

| 2024 | KRW 93.4B |

| 2025 | KRW 135.8B |

| 2026 | KRW 180B |

| 2027 | KRW 200B |

The source attributes most of this increase to Kumho Mitsui Chemicals’ MDI earnings improvement. In 2025, MDI spread recovery and utilization from the 2024 200,000-ton expansion begin to show; in 2026-2027, North American LNG insulation demand and the 710,000-ton capacity expansion add momentum.

5. Balance-sheet strength and shareholder returns

Kumho Petrochemical is described as having top-tier financial stability, with a debt ratio of only 35.2% at the end of Q3 2025. The source expects a net-cash position in 2026, supporting both MDI expansion and shareholder returns.

40% total return

The 2024-2026 policy targets a 40% total shareholder return ratio.

20%-25%

Cash dividends are planned at 20%-25% of separate net income.

10%-15%

Annual buyback and cancellation are planned at 10%-15%.

KRW 50B · 2.62M shares

The company plans to acquire KRW 50B of treasury shares and cancel them in September 2025, while also cancelling 2.62M existing treasury shares over three years.

6. Final view

The source argues that 0.5x PBR and a 40% total shareholder-return ratio give downside support. The upside comes from demand visibility, dominant domestic MDI supply, and a structural recovery in 2026-2027 earnings power from synthetic rubber and MDI.

My checklist is North American LNG FID and LNGC order continuity, the lag from insulation-maker orders to MDI shipments, completion of 710,000-ton capacity in 2027, pass-through of BD cost increases, and actual execution of shareholder returns.

Sources

- Naver Blog source: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224142783536

- 하나증권/에너지화학/윤재성 Telegram channel: https://t.me/energy_youn

- 보고서 링크: https://bit.ly/4qjs3um