DEEP RESEARCH · HYOSUNG HEAVY INDUSTRIES

Hyosung Heavy Industries: Power Supercycle and Construction Risk Cleanup

A review of AI data centers, North American grid renewal, Memphis and Changwon expansions, and pure heavy-industry re-rating after the PF big bath.

0. Bottom line first

The Hyosung thesis is less about the power-equipment boom alone and more about a 2026 re-rating after construction risk is cleared through a Q4 2025 big bath, revealing the full earnings power of heavy industry. Memphis transformers, Changwon high-voltage breakers, and HVDC are the three core axes.

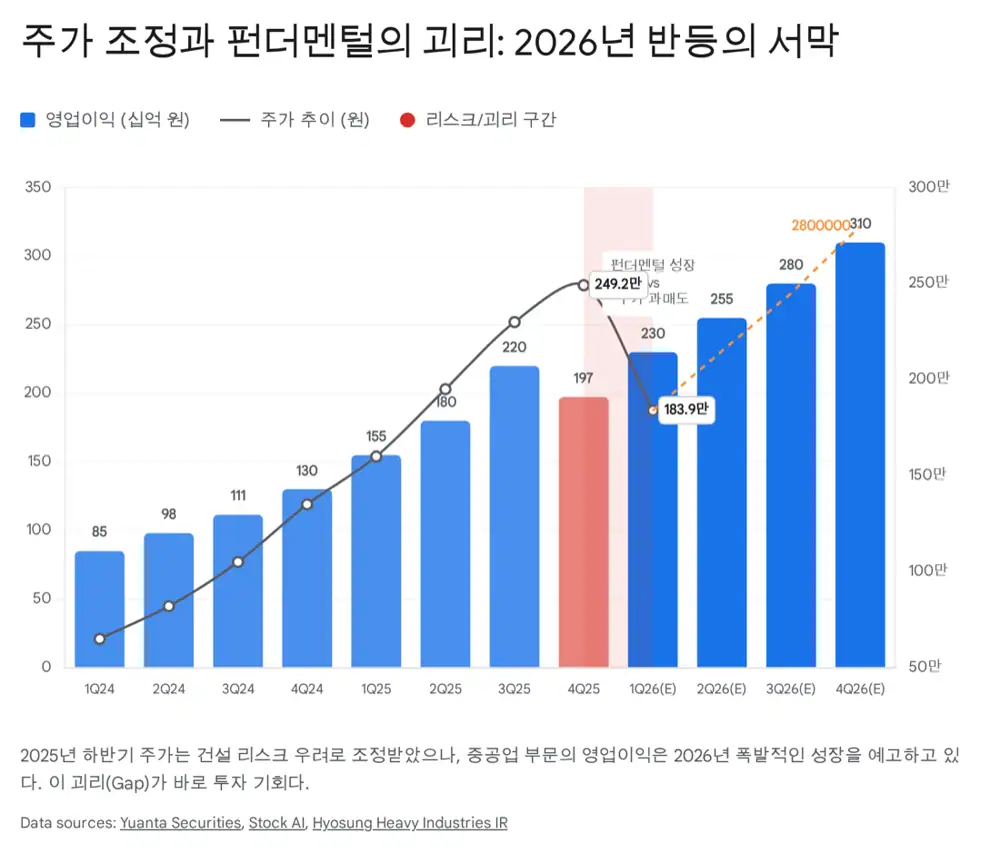

1. Nature of the correction: construction risk and Q4 costs

The source views the H2 2025 share correction as fear around construction PF contingent liabilities, unsold-unit provisions, and Q4 one-off costs rather than fundamental deterioration.

Official fact: The source estimates debt assumption under completion guarantees for local projects such as Daegu Sincheon and Busan Oncheon at around KRW 200bn, including about KRW 147.4bn from Busan Oncheon KRW 103.8bn and Daegu Sincheon KRW 43.6bn.

Interpretation: A confirmed loss is no longer uncertainty. The source treats Q4 2025 provisions as the end of the bad news and a clearing event before the company is valued more like a pure heavy-industry business in 2026.

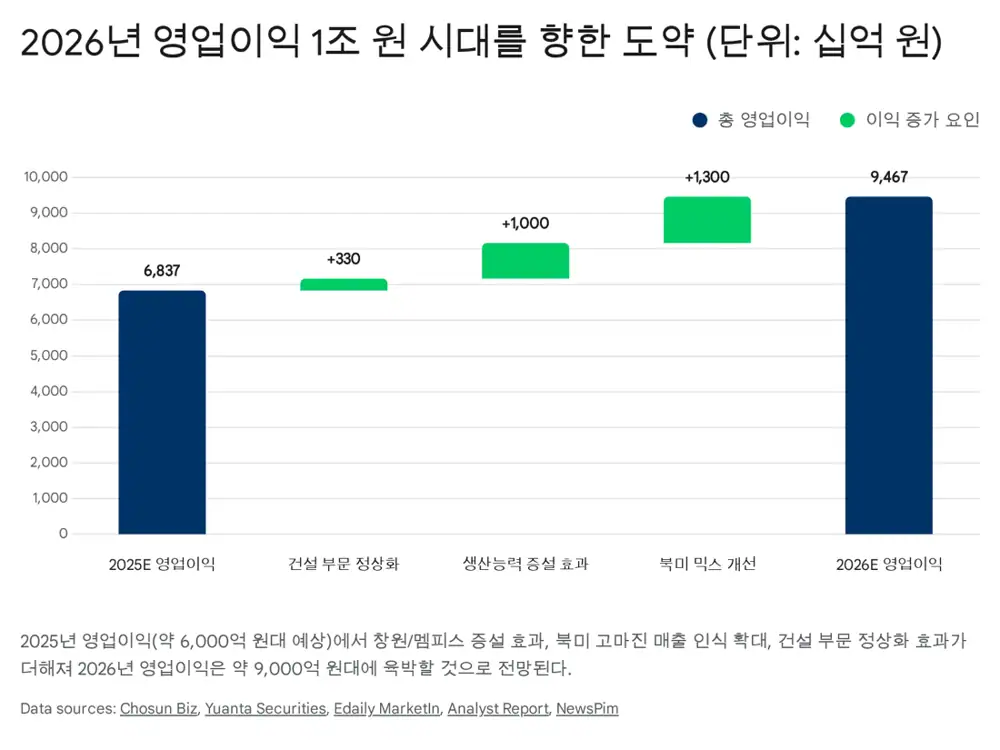

2. 2026 three-stage rocket: capacity, margin, geography

- Changwon high-voltage breaker plant: construction started in September 2025, KRW 100bn investment, completion and operation planned for H1 2026, capacity rising 1.5x.

- Memphis ultra-high-voltage transformer plant: USD 157mn, about KRW 230bn, of additional investment expands capacity by more than 50%.

- Memphis is presented as a US base capable of producing 765kV ultra-high-voltage transformers.

- In Europe, the source cites KRW 230bn of ultra-high-voltage power-equipment orders from the UK, Sweden, Spain, and others.

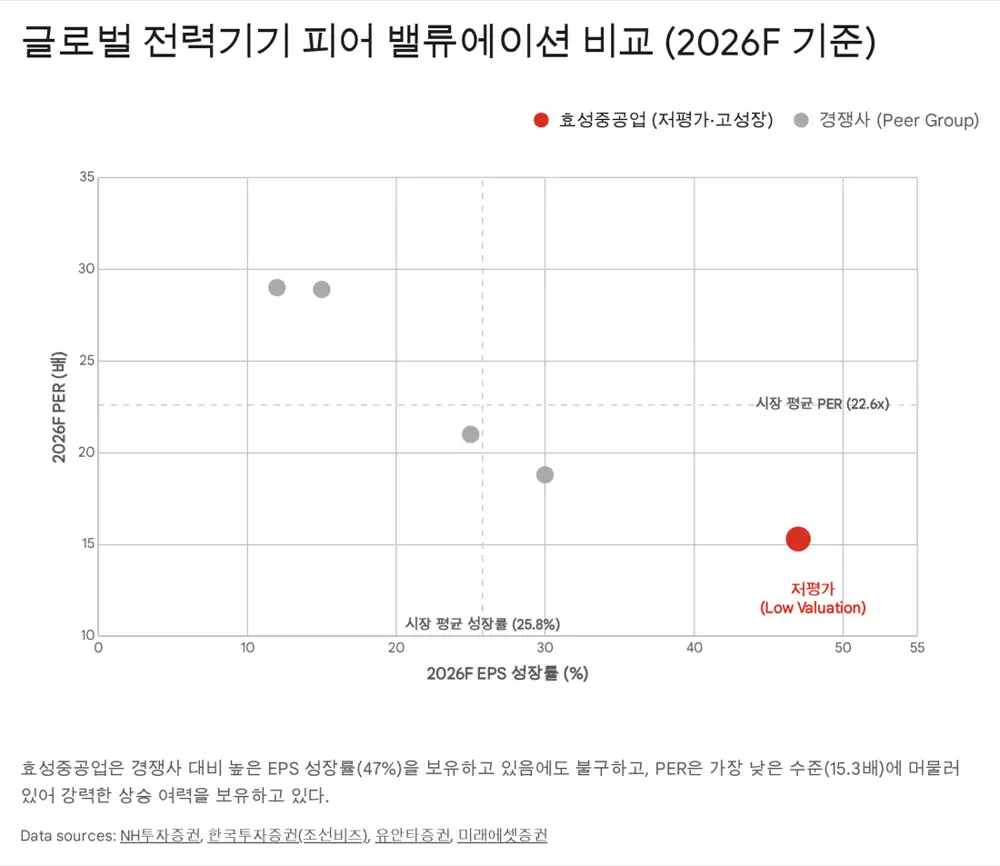

3. Margin structure: North America mix and pricing power

Official fact: The source estimates North America revenue mix at 29% in 2026 and above 35% in 2027. It presents companywide OPM rising from the mid-10% range in 2025 to 13-15% in 2026, with heavy-industry standalone OPM above 17%.

| Item | Source figure | Meaning |

|---|---|---|

| Q3 2025 operating profit | KRW 219.8bn | Record result, 13.5% OPM |

| 2026 companywide OPM | 13-15% | Recognition of high-margin orders |

| Heavy-industry OPM | Above 17% | North American UHV transformer mix |

| Anti-dumping tariff | Presented as maintained at 0% | 15-60% price-competitiveness edge versus peers |

| Target PER | 25x | Re-rating after construction discount fades |

4. Hidden value: data centers, HVDC, renewables

KRW 360bn order

AI data centers require uninterrupted power, supporting package orders involving STATCOM and ESS.

KRW 330bn investment

The company decided in Q2 2025 to build an HVDC transformer plant, with orders expected to become visible from 2026.

Grid reinforcement

Offshore wind, renewable integration, and aged-grid replacement support demand for ultra-high-voltage equipment.

5. Conclusion and risks

The source cites Yuanta Securities' KRW 2.8mn target price and more than 50% upside from the then-current share price. My checkpoints are whether Q4 2025 construction provisions truly end the issue, whether Memphis and Changwon expansion converts into revenue on schedule, and whether high-margin North America and Europe orders prove 13-15% OPM. Risks include further construction losses, raw-material or logistics bottlenecks, and a slowdown in US power-equipment investment.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224142618510

- Source 2: https://drive.google.com/open?id=16Gumv1fGSAJsAuf1X13Z7-9Vuw_K7FYWIPzpUzkduaY

- Source 3: https://www.npcelectric.com/news/transformer-market-2025-performance-and-2026-outlook.html

- Source 4: https://www.judal.co.kr/?view=stockAI&shareToken=kLDrhRgwMFciQjF5

- Source 5: https://news.stockplus.com/m?news_id=14109810

- Source 6: https://m.news.zum.com/articles/103244594/eba6aced8faced8ab8-ebb88ceba6aced9591-ed9aa8ec84b1eca491eab3b5ec9785-4q25-pre-eca491eab3b5ec9785-ec84b1ec9ea5ec84b8-eca780ec868d-vs-eab1b4ec84a4ec9d80-ec9dbced9a8cec84b1-ebb680eb8bb4-ebaaa9ed919ceab080-2-800-000ec9b90-ec9ca0ec9588ed8380eca69deab68c

- Source 7: https://www.pinpointnews.co.kr/news/articleView.html?idxno=415940

- Source 8: https://www.hellot.net/news/article.html?no=108738

- Source 9: https://www.chosun.com/economy/industry-company/2025/09/24/57DYMK3TC5FSBLJXUCH5D76ZUY/

- Source 10: https://www.ceoscoredaily.com/page/view/2025092409201560862

- Source 11: https://www.bicmagazine.com/departments/operations/hyosung-announces-major-expansion-of-memphis-power-transformer-plant/

- Source 12: https://www.hyosung.com/kr/newsroom/view/19022

- Source 13: https://biz.chosun.com/stock/stock_general/2025/11/14/VLWR736WVVFKXKBHI47FRXXO2U/

- Source 14: https://biz.chosun.com/stock/stock_general/2025/11/03/FU3AXBE76BEEVLO547TBSOUBMY/

- Source 15: https://www.etoday.co.kr/news/view/2538434

- Source 16: https://www.joongangenews.com/news/articleView.html?idxno=479804

- Source 17: https://memphischamber.com/blog/press-release/hyosung-hico-expands-u-s-manufacturing-hq/

- Source 18: https://m.megaeconomy.co.kr/news/newsview.php?ncode=1065576601494605

- Source 19: https://drive.google.com/open?id=1TQTpQjBZjH-nxJ6L-vQs-sEkyNUnU1qa

- Source 20: https://file.myasset.com/sitemanager/upload/2025/0726/160459/20250726160459887_0_ko.pdf

- Source 21: https://stock.pstatic.net/stock-research/company/18/20251014_company_899900000.pdf

- Source 22: https://securities.miraeasset.com/bbs/download/2135886.pdf?attachmentId=2135886

- Source 23: https://marketin.edaily.co.kr/News/ReadE?newsId=02666646642365720

- Source 24: https://www.chosun.com/economy/industry-company/2025/11/18/Y6LOYQLOIVHQLJOCS76HEEH5YQ/

- Source 25: http://www.whitepaper.co.kr/news/articleView.html?idxno=256534

- Source 26: https://www.woodmac.com/press-releases/power-transformers-and-distribution-transformers-will-face-supply-deficits-of-30-and-10-in-2025/

- Source 27: https://www.woodmac.com/news/opinion/transformer-troubles-manufacturing-and-policy-constraints-hit-us-transformer-supply/