DEEP RESEARCH · ZARAM TECHNOLOGY/XGSPON

Zaram Technology: Architect of the Hyperconnected Era and the Start of a Structural Turnaround

A system-semiconductor report linking low-power XGSPON SoCs, RISC-V, European ASIC orders, automotive, and edge AI

0. Bottom line first

The source argues that Zaram Technology is moving past the 2025 earnings trough and can turn around in 2026 as telecom semiconductor production revenue begins. The key points are the ZX300 ultra-low-power XGSPON chipset at about 0.9W versus competitors above 2.0W, the December 2025 KRW 23.05B European ASIC contract, and RISC-V low-power design capability that can expand into automotive and edge AI.

Official fact: The source cites Q3 2025 cumulative revenue of KRW 7.89B, operating loss of KRW 4.89B, R&D at 92.68% of revenue, a December 9, 2025 KRW 23.05B XGSPON ASIC contract, KRW 33B of convertible bonds, and KRW 2.3B of exchangeable bonds.

Interpretation: The 2025 loss reflects demand delays and upfront R&D. The 2026 question is how quickly backlog converts into production revenue and operating leverage.

1. Company overview and business model

Zaram Technology is a fabless system-semiconductor company founded in January 2000. It is headquartered in Bundang, Seongnam, and listed on KOSDAQ in March 2023 under the technology-growth special listing track. The management team led by CEO Baek Jun-hyun is described as composed of veteran engineers from Hyundai Electronics, now SK Hynix, and Samsung Electronics System LSI.

The business model has two axes: own-brand product sales and custom ASIC development and supply for global customers through ODM. Manufacturing is outsourced to global foundries and OSATs, while the company focuses resources on R&D and customer-specific chip design. About 70% of employees are R&D personnel; the company was named an Excellent Technology Research Center in 2017 and selected as a Materials/Parts/Equipment Strong Small Giant in 2021.

2. Technology moat: XGSPON, RISC-V, distributed processing

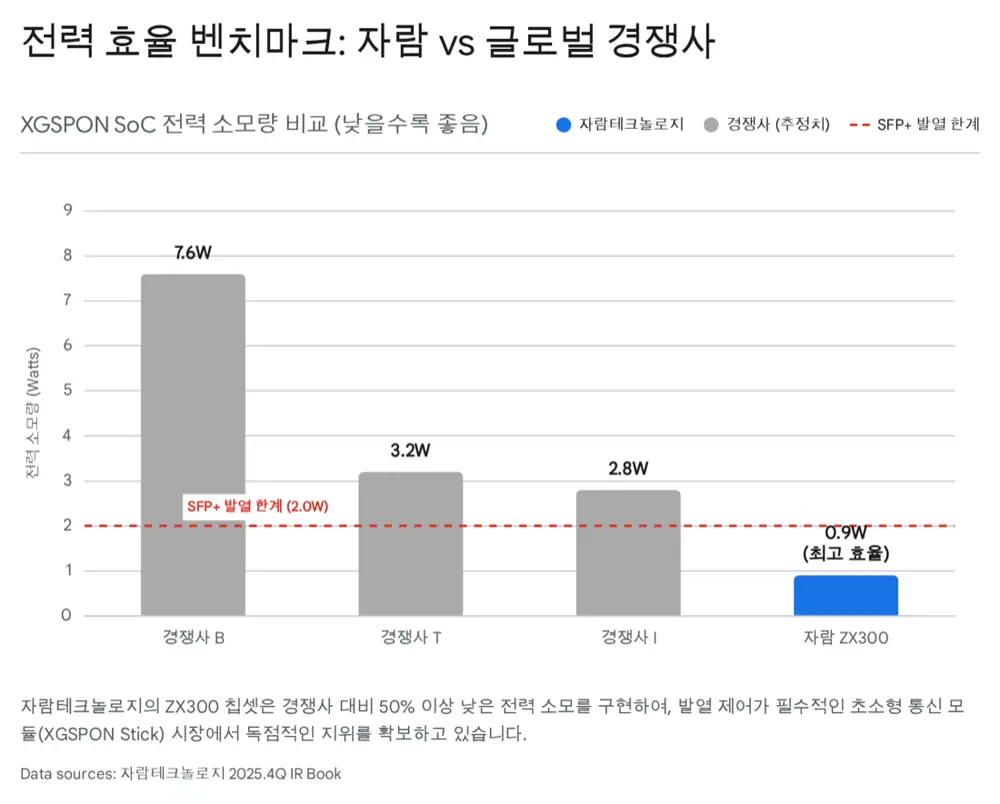

XGS-PON is a core access-network technology for 10Gbps internet, and Zaram’s XGSPON SoC is differentiated by power efficiency. Competing chipsets are typically above 2.0W, while the main ZX300 product is described at about 0.9W. That matters in SFP+ stick modules where heat dissipation space is narrow.

| Technology | Source detail | Investment meaning |

|---|---|---|

| Ultra-low power | ZX300 at 0.9W versus competitors above 2.0W | OPEX reduction and lower heat/lifetime risk |

| SFP+ form factor | Can be mounted without a separate heat sink, per source | 10G internet by plugging modules into existing equipment |

| RISC-V | Communication-optimized instruction design without ARM royalties | Price competitiveness and gross-margin defense |

| RTOS | 75% less memory use than Linux and boot time below 10 seconds | Lower BOM and maintenance cost |

| Distributed processing | 10Gbps traffic handling with zero-latency framing | Meets 5G ultra-low-latency requirements |

The source sees the combination of ultra-low-power design, RISC-V optimization, and distributed processing as the reason Zaram can stand out among global competitors such as Broadcom, Intel, and MediaTek.

3. End-market outlook: 10G internet and 5G small cells

The global telecom market is moving from 1G GPON to 10G XGS-PON. 4K/8K streaming, cloud gaming, metaverse services, and AI traffic all require higher-bandwidth and lower-latency access networks.

USD 1.82B to USD 7.11B

The source cites global XGS-PON market growth from USD 1.82B in 2024 to USD 7.11B in 2033, a 16.7% CAGR.

USD 42.5B

The U.S. broadband program can align with Non-China equipment preference.

39.2% CAGR

The 5G small-cell market is expected in the source to grow at 39.2% CAGR from 2026 to 2033.

25G/50G

Zaram is a member of the 25GS-PON MSA with Nokia and others, with a 25G PON sample chip planned for late 2025.

5G mmWave requires dense small-cell deployment. Carriers want to use existing PON networks for mobile backhaul instead of installing dedicated lines, and Zaram’s XGSPON Stick is framed as a plug-and-play way to reduce CAPEX. Gigawire also serves a niche cash-cow role in Europe’s older buildings, hotels, resorts, and apartments where fiber installation is hard.

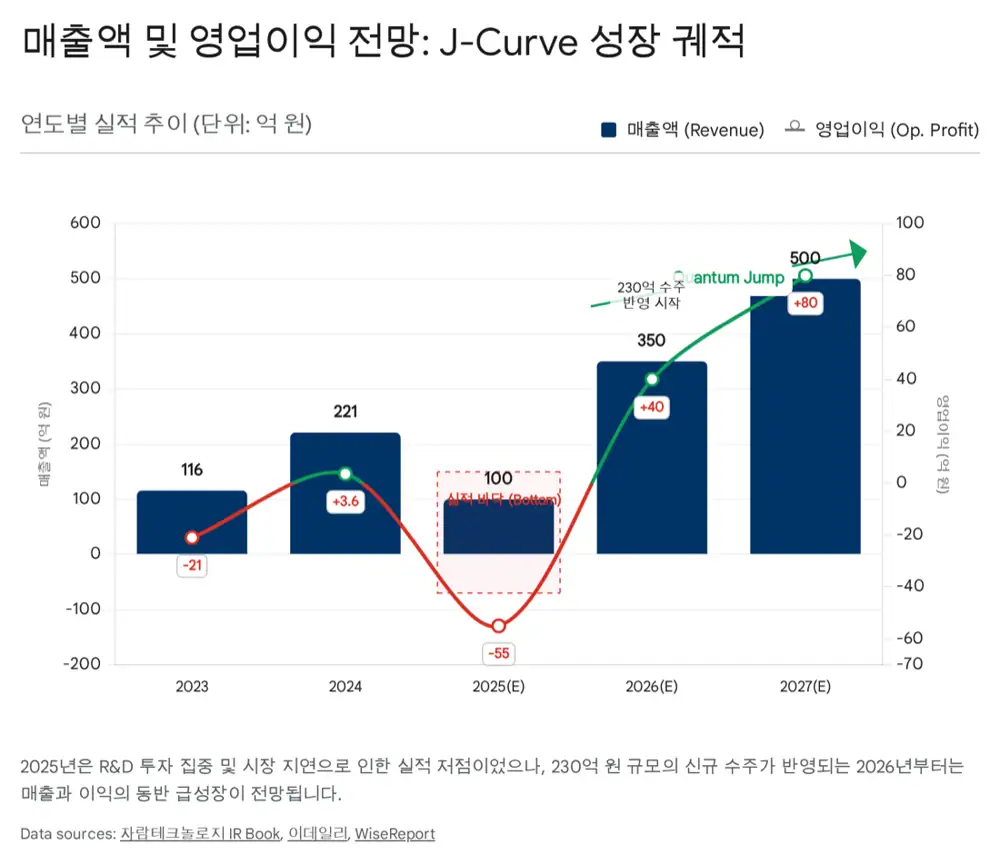

4. Earnings trough and backlog

Q3 2025 cumulative results were weak, with revenue of KRW 7.89B and operating loss of KRW 4.89B. The source attributes this to high rates, delayed carrier investment, telecom-equipment inventory correction, R&D spending for 25G PON and automotive chips, derivative valuation losses, and CB-related finance costs.

| Contract/financial item | Source figure | Meaning |

|---|---|---|

| December 2025 contract | KRW 23.05B XGSPON ASIC design and supply | Revenue recognition from Dec. 8, 2025 to Jan. 7, 2028 |

| 2023 first contract | KRW 16.5B | Same customer, estimated in the market to be Nokia |

| 2024 annual revenue | KRW 22.1B | The single KRW 23.05B contract exceeds annual revenue |

| Production from first contract | More than 10 years of KRW 50B annual revenue expected | Shift from NRE to production sales |

| IBK outlook | Potential for more than KRW 100B annual revenue over 10+ years | Long-term visibility from backlog |

| Financing | KRW 33B CB and KRW 2.3B EB | Liquidity for R&D and operations |

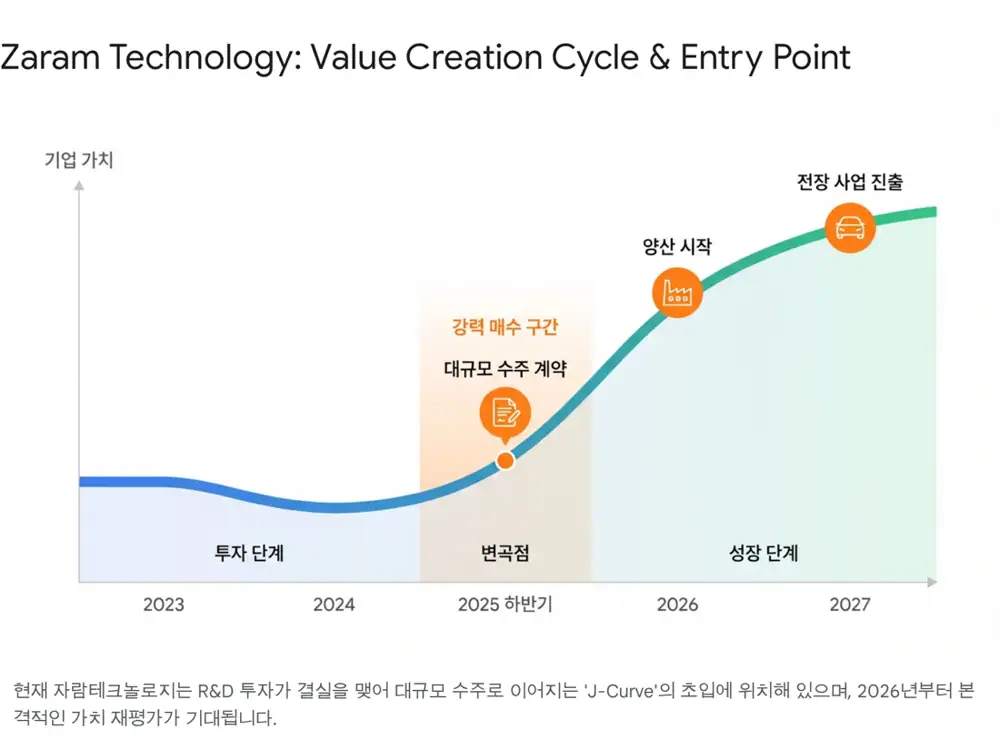

As a fabless company, Zaram can see rapid profit improvement when revenue exceeds breakeven because fixed-cost leverage is high. The source frames 2026 as the year to verify profitability from existing-product recovery plus new contract revenue.

5. Growth roadmap: SDV and edge AI

In June 2025, Zaram was selected as lead institution for a government project to develop in-vehicle high-speed communication semiconductors for SDV architectures. As vehicles become software-defined, internal data-transfer requirements rise and demand grows for high-speed Ethernet semiconductors. The source cites a 2026 prototype and 2028 commercialization target.

In edge AI, the company is developing AI communication semiconductors with low-power NPUs for on-device inference. Target applications include CCTV, smart appliances, and robots. A 2026 AI semiconductor sample-chip release is the stated goal.

6. Risks and scenarios

Overhang must be tracked. The KRW 33B CB and KRW 2.3B EB issued in July 2024 can be converted from July 31, 2025. The post-refixing conversion price is around KRW 37,322. A 0% coupon can signal that holders expect capital gains, but if the share price rises above the conversion price, profit-taking supply may emerge.

- Customer concentration: A significant share of revenue is concentrated in a few global telecom-equipment customers.

- Valuation: Because 2025 losses are expected, traditional PER metrics can make the stock look expensive.

- Execution risk: The 2026 turnaround is backlog-based, but weak global conditions could delay production schedules.

Bull Case

If European production revenue is recognized early and automotive semiconductor development accelerates, the source sees a possible break above the prior high of KRW 54,000.

Base Case

Stable backlog-based growth and confirmed 2026 profitability could support gradual upside and valuation re-rating.

Bear Case

If carrier investment weakens again or overhang supply hits at once, the stock could correct near the KRW 22,000-24,000 support zone described in the source.

7. Final view

The source sees the current market cap of about KRW 250B as attractive given the technology moat, possible 2026 revenue scale, and operating leverage. The final rating is BUY, with a target price range of KRW 55,000-65,000 based on 2026E EPS and a 25x target P/E.

My checklist is quarterly revenue recognition from the KRW 23.05B contract, the actual start of production revenue from the first contract, 25G PON sample-chip and SDV prototype timing, CB/EB conversion supply, and customer diversification.

Sources

- Naver Blog source: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224142614842

- 자람테크놀로지 기업현황 - 기업모니터: https://comp.wisereport.co.kr/company/c1010001.aspx?cmp_cd=389020

- XGS-PON Market Research Report 2033 - Dataintelo: https://dataintelo.com/report/xgs-pon-market

- Global Telecom Capex to Normalize, Not Disappear - Dell’Oro Group: https://www.delloro.com/news/global-telecom-capex-to-normalize-not-disappear/

- Small Cell 5G Network Market Size - Grand View Research: https://www.grandviewresearch.com/industry-analysis/small-cell-5g-network-market

- 자람테크놀로지 유럽 230억 추가 수주 - Daum: https://v.daum.net/v/HlsBkGSrmT?f=p

- 자람테크놀로지 230억원 공급계약 - K trendy News: http://www.k-trendynews.com/news/articleView.html?idxno=195949

- 자람테크놀로지 RISC-V 엣지 AI 반도체 - 이투데이: https://www.etoday.co.kr/news/view/2535533

- 자람테크놀로지 자산 90% 자금 수혈 - 뉴스토마토: https://www.newstomato.com/ReadNews.aspx?no=1236723

- IBK증권 노키아 추가 수주 분석 - Daum: https://v.daum.net/v/FSR76CwaZi

- 자람테크놀로지 SDV 차량용 반도체 국책과제 - DigitalToday: https://www.digitaltoday.co.kr/news/articleView.html?idxno=571795

- 자람테크놀로지 330억 전환사채 발행 - 마켓인: https://marketin.edaily.co.kr/News/ReadE?newsId=03263606638959440

- 자람테크놀로지 주가 정보 - 알파스퀘어: https://alphasquare.co.kr/home/stock-summary?code=389020

- 자람테크놀로지 투자분석 - 주달: https://www.judal.co.kr/?view=stockAI&shareToken=C1141bhim3r8eCHx