DEEP RESEARCH · PHARMARESEARCH

PharmaResearch: Rejuran's Global Expansion and the 2026 Re-Rating Conditions

A review of Q3 seasonality, export mix shift, CVC partnership, and Europe/US milestones.

0. Bottom line first

My conclusion is that PharmaResearch's late-2025 share-price correction reflects peak-out fears and flow pressure more than a collapse in fundamentals. Q3 revenue slowed QoQ, but YoY growth, 46% OPM, 81% GPM, and rapid Americas export growth show improving quality. The 2026 re-rating depends on European Rejuran shipments, the MNRF device, US offline channels, and CVC-enabled M&A.

1. Company and moat: DOT, PN/PDRN, Rejuran

Official fact: The source says PharmaResearch was founded in March 2001, has headquarters and a GMP-certified plant in Gangneung, Gangwon-do, and owns DOT™ (DNA Optimizing Technology), which optimizes DNA fragments extracted from germ cells of returning salmon on Korea's east coast.

DOT™

PDRN/PN extraction and processing expand into Rejubinex, Rian eye drops, Rejuran, Conjuran, and Rejuran Cosmetics.

Rejuran

Presented as a premium skin-booster brand that has maintained pricing power for more than 10 years since its 2014 launch.

Drugs, devices, cosmetics

Diversified businesses create domestic cash flow that can fund global expansion.

2. Share correction: peak-out or seasonality?

The source says the share price fell more than 40% from its yearly high in the second half of 2025, reaching the mid-KRW 300,000 range. But it attributes the move to overlapping seasonality, competition fears, institutional and foreign selling, and panic selling after major support levels broke.

| Q3 2025 item | Source figure | How I read it |

|---|---|---|

| Revenue | KRW 135.4bn, QoQ -4% | Starting point of market peak-out concerns |

| Domestic medical devices | KRW 57.2bn, QoQ -6% | July-September aesthetic off-season |

| Medical-device exports | KRW 19.6bn, QoQ -19% | Partner inventory adjustment and shipment timing |

| YoY growth | Revenue +52%, operating profit +77%, net profit +99% | The source's evidence that fundamentals remain strong |

| OPM/GPM | OPM 46%, GPM 81% | Improved from OPM 39% and GPM 72% a year earlier |

Interpretation: Looking only at QoQ slowdown makes it look like peak-out. But combined with YoY growth and margin expansion, it is hard to call it structural deterioration.

3. Competition frame: complement, not pure substitute

Investor concern centers on whether PDLA/PLA skin boosters such as Juvelook will take share from Rejuran. The source views this as a natural result of the whole skin-booster market expanding. Rejuran (PN) specializes in skin regeneration and healing, while Juvelook (PDLA) specializes in volume and collagen generation, so clinics may use them as complements rather than substitutes.

The source also says Rejuran has loyal customers who accept pain and downtime for clear results and that it maintains a premium-price policy even as competing products enter price competition.

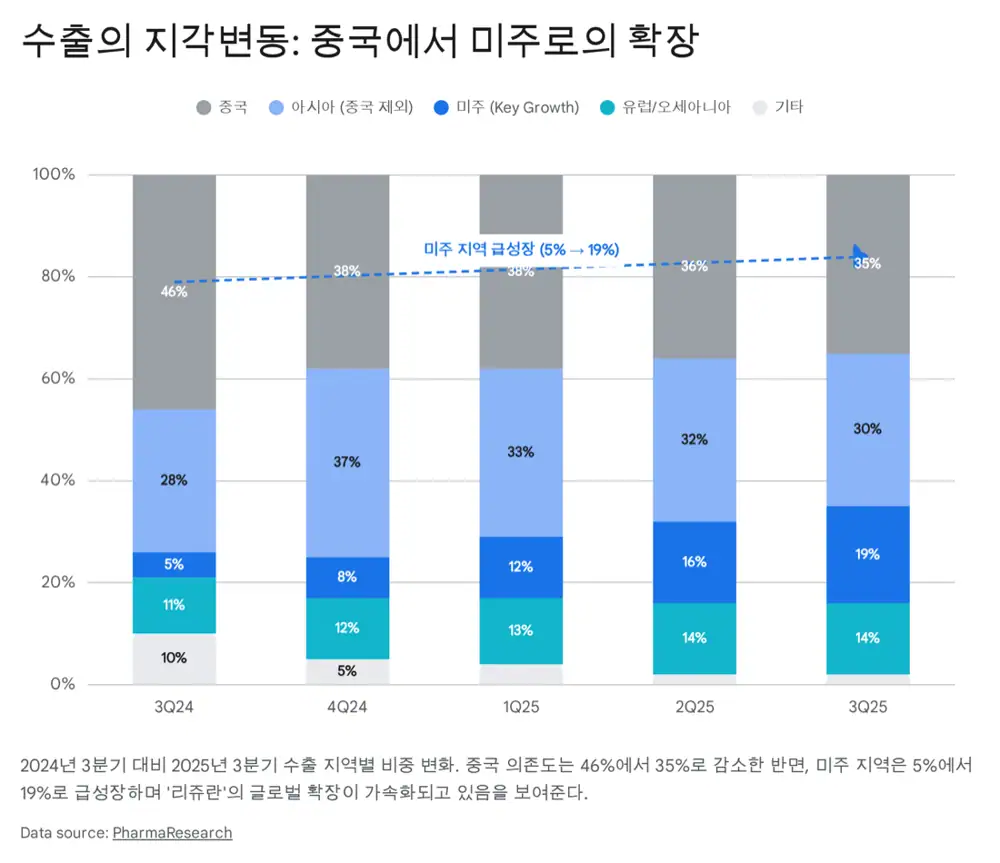

4. Export mix: lower China concentration, rapid Americas rise

Official fact: The source says China's share of total exports fell from 46% in Q3 2024 to 35% in Q3 2025, while the Americas share increased from 5% to 19%, almost quadrupling.

| Business axis | Source figure | Meaning |

|---|---|---|

| Cosmetics exports | KRW 21.9bn, QoQ +13% | Exceeded medical-device exports of KRW 19.6bn |

| US channels | Amazon and TikTok Shop momentum | Builds B2C brand awareness before medical-device approval |

| Drug exports | KRW 8.6bn, QoQ +23% | Potential stable cash cow from PDRN-based drugs |

Interpretation: The lower China share is not necessarily a collapse in China revenue. The source reads it as faster growth elsewhere, which can reduce the valuation discount tied to China risk.

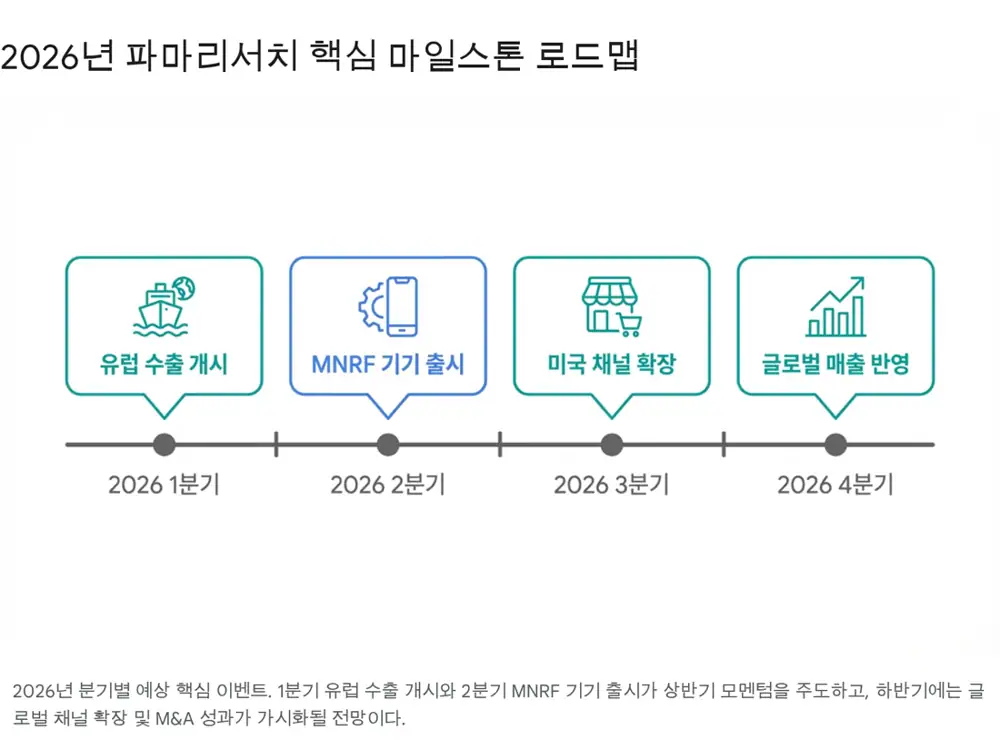

5. 2026 milestones: the order of a re-rating

- Q1: Based on CE-MDR certification received at the end of 2024, Rejuran medical-device exports are expected to begin to at least six major European countries including Germany, Italy, France, and Spain. The source expects even initial MOQ shipments could create revenue in the hundreds of billions of won.

- Q2: An MNRF, or Microneedle Radio Frequency, device with dedicated Rejuran injection functionality is expected. It can reduce pain and procedure variability while creating a device-and-consumables bundle.

- Q3: US cosmetics channels are expected to expand from Amazon-centered online sales to offline channels such as Costco and Sephora.

- Q4: CVC Capital Partners' global network could make M&A of local distributors or aesthetic companies more concrete.

6. Valuation and risks

Official fact: The source says CVC Capital Partners invested about KRW 200bn in PharmaResearch in September 2024. It also says major securities firms project 2026 revenue of about KRW 710bn and operating profit of about KRW 300bn.

| Item | Source view | Check point |

|---|---|---|

| PER | Low-10x range on 2026E EPS | Claimed undervaluation versus peers such as Hugel and Classys at 20-25x |

| Target price | Broker average KRW 640,000-820,000 | The source argues for more than 50% upside from current levels |

| First turnaround trigger | Q4 2025 earnings release expected in February 2026 | Consensus of KRW 155.9bn revenue (+51% YoY) and KRW 65bn operating profit (+93% YoY) |

| Trend reversal | Around April-May 2026 | European export data and new-device expectations need confirmation |

- Domestic competition: Juvelook, Ultracol, Volnewmer, and others can intensify marketing.

- FX volatility: as exports rise, KRW strength can pressure profitability.

- China geopolitical risk: regulatory changes or weak consumer sentiment remain risks, though US and European diversification is mitigating them.

My view is that PharmaResearch must prove global expansion with numbers in 2026. If European initial shipments, MNRF launch, US offline channels, and CVC-enabled M&A appear in sequence, the current fear zone can become the starting point for a re-rating.

Sources

- Source 1: Original Naver Blog post · https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224141423706

- Source 2: Chosunbiz: PharmaResearch stock rises on analysts outlook · https://biz.chosun.com/en/en-finance/2026/01/08/66SEMDSBBVH3FIJRI7FQAFB3WA/

- Source 3: Naver Premium Content: PharmaResearch fear-zone analysis · https://contents.premium.naver.com/a18382/prism/contents/251228095351488wf

- Source 4: Kiwoom Securities: Rejuran business analysis · https://invest.kiwoom.com/inv/37191

- Source 5: Seoul Economic Daily: next skin-booster competition · https://www.sedaily.com/NewsView/2GU0B7TOLM

- Source 6: Business Post: resilient Rejuran sales · https://www.businesspost.co.kr/BP?command=article_view&num=414561

- Source 7: Chosunbiz: Q4 earnings momentum · https://biz.chosun.com/stock/stock_general/2025/10/17/A3QA5FUGFJGXTLWZCDNDIGMMZQ/

- Source 8: PharmaResearch company PR · https://pharmaresearch.co.kr/sub/press/view.html?idx=313

- Source 9: Barchart: CVC investment in PharmaResearch · https://www.barchart.com/story/news/28530158/pharmaresearch-accelerates-global-market-expansion-with-investment-from-global-private-equity-fund-cvc

- Source 10: PRESS9: solid Q4 PharmaResearch earnings · http://www.press9.kr/news/articleView.html?idxno=70680

- Source 11: CVC: PharmaResearch global expansion investment · https://www.cvc.com/media/news/2024/2024-09-05-pharmaresearch-accelerates-global-market-expansion-with-investment-from-global-private-equity-investor-cvc/

- Source 12: Pharmnews: US revenue becoming visible · https://www.pharmnews.com/news/articleView.html?idxno=300760

- Source 13: Mirae Asset: PharmaResearch report PDF · https://securities.miraeasset.com/bbs/download/2138056.pdf?attachmentId=2138056

- Source 14: PRESS9: Samsung Securities target price maintained · http://www.press9.kr/news/articleView.html?idxno=70558