DEEP RESEARCH · CLASSYS/MEDICAL AESTHETICS

Classys: Structural Causes of the Share-Price Correction and the 2026 Global Supercycle Roadmap

Separating post-Ilooda merger cost and overhang noise from the 2026 Brazil, China, U.S., and Europe growth setup

0. Bottom line first

The source reads Classys' share-price correction from 2H25 into early 2026 not as fundamental impairment, but as transitional friction from the Ilooda merger: overhang, one-off costs, and controlling-shareholder noise. In contrast, it frames 2026 as the first year of a supercycle combining Brazil direct operation, faster equipment sales in developed markets, and China approvals.

The key question for me is whether the margin decline is structural or investment-like. 3Q25 OPM was 45.3%, down from 48.7% a year earlier and 51.6% in the prior quarter, but the source separates deferred advertising expense, merger advisory fees and severance, and PPA amortization as temporary items.

1. Three sources of share-price pressure

From late December 2025 into early January 2026, volatility was driven by a mix of supply-demand pressure, profitability concerns, and governance uncertainty rather than one isolated issue.

| Pressure | Source fact | Investment read |

|---|---|---|

| Merger overhang | The Ilooda merger closed on October 1, 2024, and about 1,506,140 new merger shares were listed. Ilooda's minority-shareholder ratio was about 57% at the end of the first quarter before the merger. | A shareholder base more likely to realize short-term gains likely increased volume and volatility around the new-share listing. |

| Merger-term noise | The scheduled purchase price was KRW 7,293, and the appraisal-right exercise limit was KRW 30 billion. | The market focused first on merger-ratio debate, new-share pricing, and possible EPS dilution. |

| Controlling-shareholder issue | Rumors circulated that Bain Capital's BCPE Centur Investment, the largest shareholder, could sell its stake. | Unclear timing, buyer, and structure chilled sentiment, while also implying that Classys is viewed as an attractive M&A asset. |

Interpretation: I read the correction as a period when the market mistook post-merger integration costs for long-term impairment. Still, overhang and controlling-shareholder-sale rumors can affect actual supply, so short-term volatility needs to be treated separately.

2. 3Q25 results: the numbers are still strong

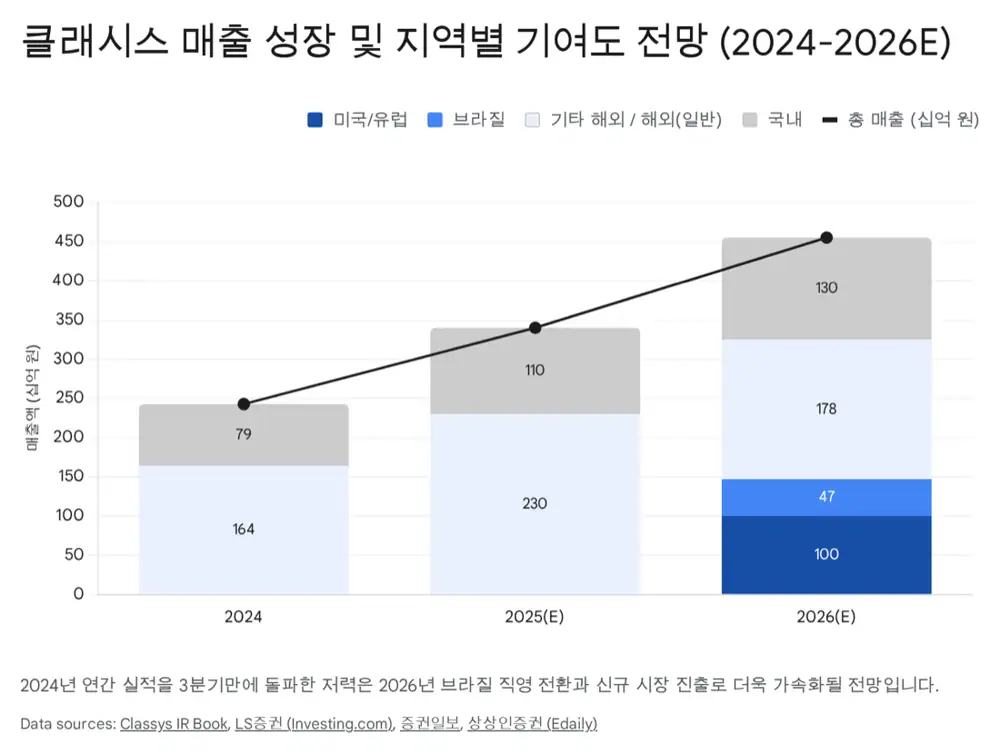

Official fact: 3Q25 consolidated revenue was KRW 83.0 billion, up 39.7% year over year and down 0.3% quarter over quarter. Cumulative revenue through 3Q25 was KRW 243.4 billion, already above full-year 2024 revenue.

| Region | Main performance/features | Note |

|---|---|---|

| Thailand | Became the top country by cumulative revenue through 3Q | K-Beauty trend spread and stronger local partnerships |

| Brazil | Revenue recovered and a direct subsidiary was established | Re-entry into a growth path after temporary stagnation |

| Americas | Sharp increase in new-device sales | Stronger position in the U.S. and Canadian markets |

| Europe | Strong growth in Spain, Turkey, and other key countries | New-market expansion starting to show |

| Korea | Up 56.4% year over year | Ilooda products and strong consumables sales |

KRW 83.0bn

3Q25 consolidated revenue, +39.7% YoY and -0.3% QoQ.

KRW 42.9bn devices

Equipment sales represented 52% of revenue. A larger installed base supports future consumables revenue.

KRW 37.3bn

Consumables were up 43.4% YoY and represented 45% of revenue.

76.8%

Gross margin stayed high despite the inclusion of legacy Ilooda items and higher device mix.

3. Temporary margin retreat and balance-sheet stability

3Q25 consolidated OPM of 45.3% remained far above the average medical-device business, but disappointment followed the decline from 48.7% a year earlier and 51.6% in the previous quarter. The source points to deferred advertising expense, merger-related one-off costs, and PPA amortization.

Official fact: At the end of 3Q25, total assets were KRW 654.4 billion, liabilities were KRW 136.0 billion, and equity was KRW 518.4 billion. Current assets were KRW 272.4 billion, cash plus short-term financial instruments were about KRW 171.6 billion, and the debt ratio was about 26%.

4. 2026 turnaround: Brazil and margin recovery

The source expects the turnaround to become visible around the 4Q25 earnings release, likely in February 2026. Consensus cited in the source expects 4Q25 OPM to rebound to about 53%, up 5 percentage points year over year and 8 percentage points quarter over quarter.

Official fact: Through Classys Brasil Ltda., established after October 2025, the Brazil business shifts from a distributor model to direct operation. Revenue recognition moves from wholesale price to retail price, meaning final hospital supply price.

- Brazil revenue is expected to reach about KRW 47.0 billion in 2026, up 64% year over year.

- Early direct operation can add personnel, rent, and marketing costs, causing a slight dip in consolidated OPM.

- The source interprets this as strategic investment in local customer data, pricing power, and marketing efficiency rather than simple cost inflation.

| 2026 outlook | Source range | Meaning |

|---|---|---|

| Revenue | KRW 455.1bn-465.8bn | +34%-36% year over year |

| Operating profit | KRW 204.9bn-243.8bn | +23.5%-44% year over year |

| Valuation | About 23x 2026E PER | The source sees undervaluation given CAGR above 30% and PEG Ratio below 1. |

5. 2026 global growth milestones

KRW 100bn market

China is framed as a strategic market that could account for about 7%, or KRW 100 billion, of Classys' 2030 revenue target of about KRW 1.4 trillion.

2H26

Volnewmer applied for China NMPA review in October 2025, with the source expecting approval and launch in 2H26.

Early 2027 target

Ultraformer MPT has completed local clinical work and is in the report-preparation stage, targeting approval in early 2027.

Developed-market device growth

U.S. Volnewmer sales in 2025 are expected to exceed the 300-unit estimate, and Europe revenue is forecast to grow 92% YoY in 2026.

In the U.S., Volnewmer expanded its sales network after its 4Q24 launch, and the source expects the growing installed base to convert into high-margin consumable tip revenue in 2026. Europe remains conservative because approvals differ by country, but Ultraformer MPT and Volnewmer sales began in 2H25 and key distributor partnerships are lowering entry barriers.

In Korea, new products such as Quad-say/Quadessy, launched in July 2024, should contribute for a full year in 2026. After the Ilooda merger, Classys' B2C marketing and brand power combine with Ilooda's U.S./Europe B2B network and microneedle RF product line, enabling combination procedure packages such as Shurink (HIFU) plus Secret RF.

6. Investment strategy: separate short-term noise from long-term expansion

The source concludes that the recent correction reflects post-large-M&A integration, temporary costs, and supply-demand noise rather than weakened core competitiveness. If the 4Q25 results confirm margin recovery, the market may increasingly view overhang and cost growth as already priced in.

- Bad-news fade: Check whether overhang and temporary costs ease around the 4Q25 earnings release.

- Structural growth: Brazil direct operation, China approvals, and U.S./Europe device expansion form the 2026 growth roadmap.

- Valuation appeal: The source sees the stock as attractive for medium- to long-term investors given 2026E revenue growth of +34% and operating-profit growth of +44%.

Interpretation: My checklist is whether 4Q25 OPM recovers to around 53%, whether Brazil direct operation raises gross revenue enough to offset added costs, and how quickly U.S. installed devices convert into consumables revenue. If those three are confirmed, the 2026 rerating thesis becomes much stronger.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224141380348

- News1 merger-share overhang article: https://www.news1.kr/finance/general-stock/5575543

- Chosun Biz Ilooda merger article: https://biz.chosun.com/stock/stock_general/2024/07/03/PCID6PERV5C73O22JRPN4SNHAM/

- ROA Classys research PDF: https://static.roa.ai/research/company/20240626_company_344147000.pdf

- Stockplus Brazil/U.S. growth article: https://news.stockplus.com/m?news_id=15195837

- Seoul Economic Daily 4Q OPM article: https://www.sedaily.com/NewsView/2K773SOLJT

- Investing.com LS Securities comment: https://kr.investing.com/news/stock-market-news/article-1773803

- Securities Daily target-price article: http://www.s-d.kr/news/articleView.html?idxno=78592

- Daum/Sangsangin growth article: https://v.daum.net/v/20251217074903752

- Classys Volnewmer China clinical/approval material: https://classys.co.kr/?kboard_content_redirect=584