DEEP RESEARCH · SAMYANG FOODS

Samyang Foods: Buldak IP and a Global Capacity Step-Up

A review of the share-price correction, tariff risk, Miryang Plant 2, the Jiaxing plant, and the 2026 KRW 3tn revenue case.

0. Bottom line first

The recent correction looks less like damage to Buldak demand and more like the overlap of valuation fatigue, tariff concerns, and temporary supply bottlenecks. The 2026 question is whether full-year Miryang Plant 2 output and preparation for local China production can support KRW 3tn-plus revenue and mid-20% OPM.

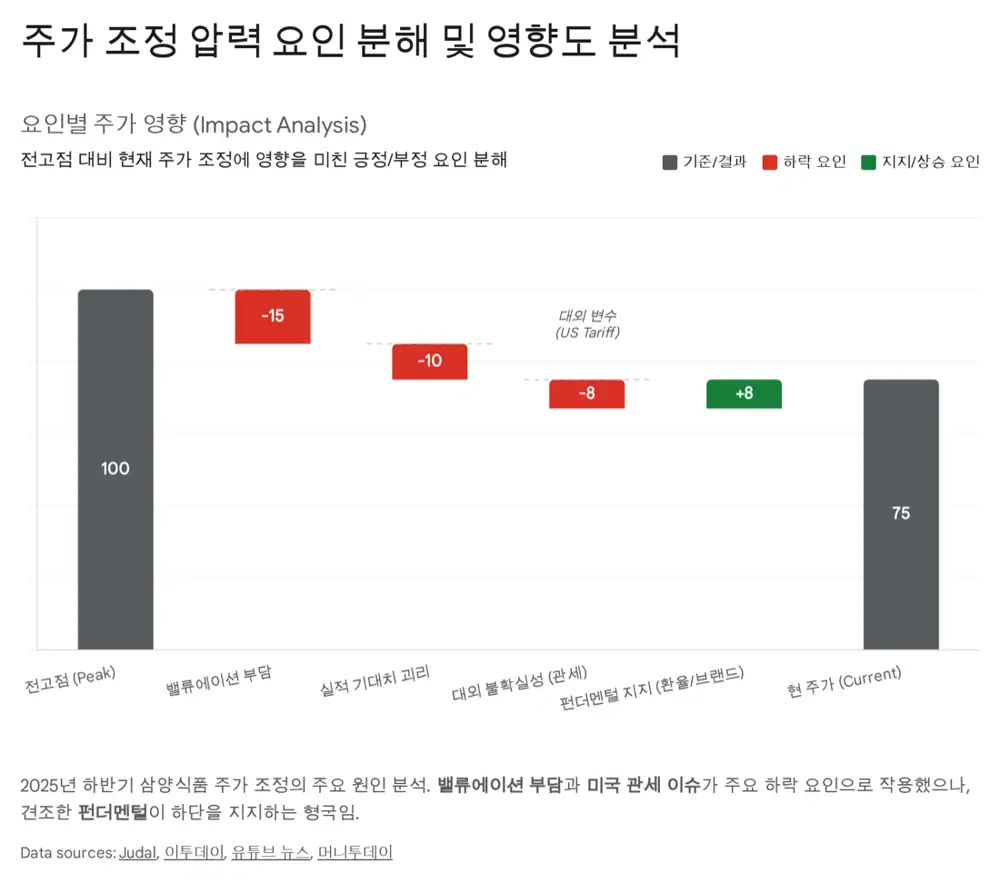

1. Why the correction happened: separating noise from signal

- Valuation fatigue: after record highs, foreign and institutional profit-taking and year-end rebalancing amplified the correction.

- Tariff risk: a Trump return and 10-20% universal-tariff scenario pressured Korea food exporters to the US.

- Q4 expectations: China inventory cleanup, marketing spending, hiring, and depreciation for Miryang Plant 2 may pressure near-term OPM.

Interpretation: The source treats Buldak's US positioning as a moat. It is seen less as cheap instant ramen and more as a trendy Asian meal, so pricing and brand loyalty can absorb part of the tariff burden.

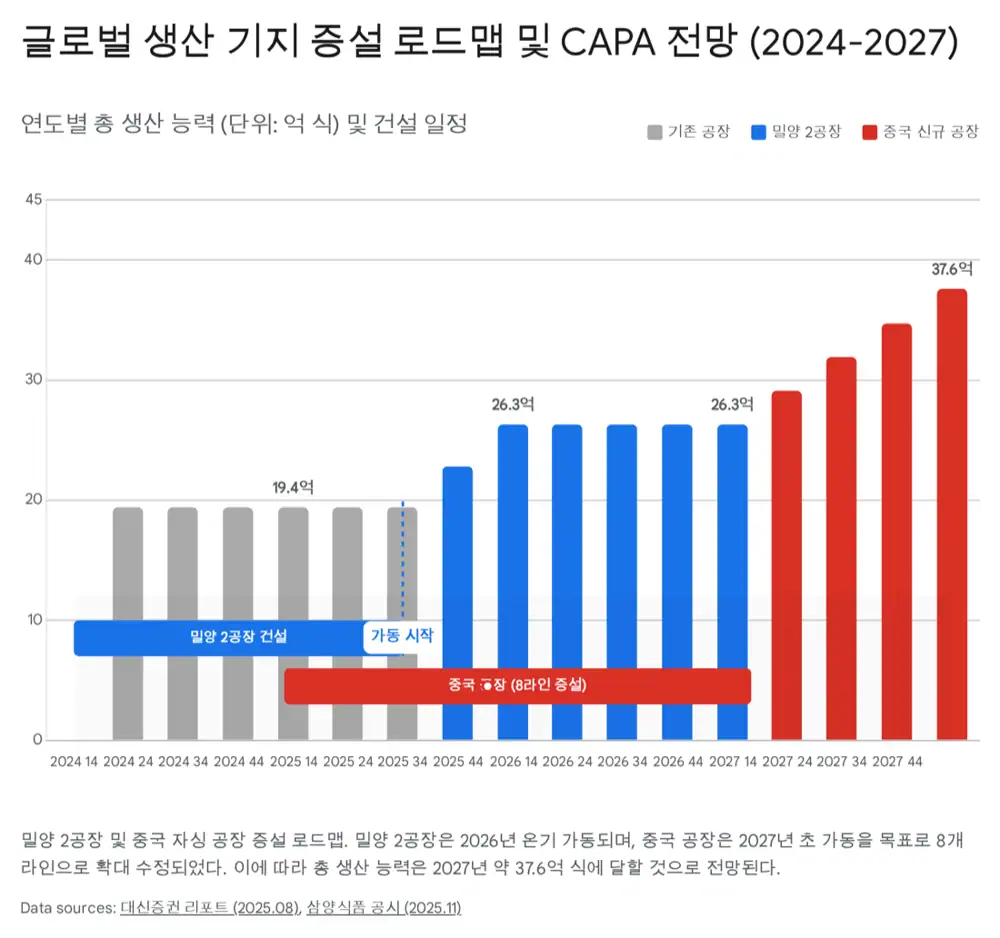

2. Capacity: Miryang Plant 2 and Jiaxing, China

Official fact: Miryang Plant 2 began partial operation around bag-noodle lines in July 2025 and targets full operation of six lines by the end of 2025. The source estimates annual capacity at about 690mn servings on a 20-hour basis and 830mn servings at 24-hour full operation.

| Base | Source figure | Strategic meaning |

|---|---|---|

| Miryang Plant 2 | 6 lines, about 690-830mn servings | Relieves US and Europe export bottlenecks |

| Jiaxing, China | Raised from 6 to 8 lines | Local production lowers tariff, logistics, and labor burden |

| China full run-rate | About 1.13bn servings/year estimated | Enables offline penetration into tier-2 and tier-3 cities |

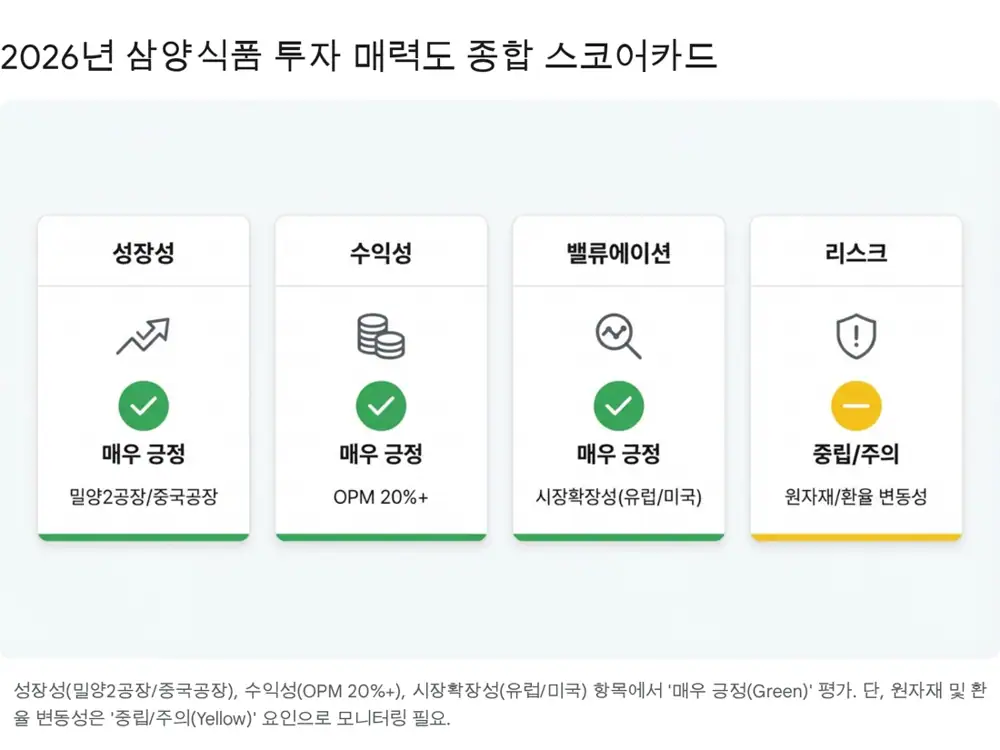

3. 2026 earnings scenario

Official fact: The source presents 2026 revenue of about KRW 3.0-3.1tn, operating profit of about KRW 693-752.2bn, and OPM of about 23-25%.

Mainstream penetration

Walmart penetration is cited around 90%, while Costco and other warehouse clubs remain around 50% with room to rise.

Next J-curve

The Netherlands entity supports expansion into channels such as Tesco, Asda, Rewe, and Albert Heijn.

Export share above 80%

High-ASP exports and fixed-cost absorption underpin the mid-20% OPM thesis.

4. Cost and policy risks

- Palm oil: Indonesia's biodiesel blend change from B40 to B50 and limited supply growth create cost pressure.

- Wheat: stable wheat prices can partly offset palm-oil pressure.

- US tariffs: protectionist risk remains, but price increases and brand loyalty may cushion the impact.

- Local China production: long-term production diversification reduces geopolitical and tariff risk.

5. Conclusion and valuation

The source compares Nissin and Toyo Suisan at 16-18x PER and argues Samyang can justify a 25-28x target PER given 20%+ CAGR and 25% OPM. My checkpoint is whether Buldak remains a one-off trend or becomes a repeatable global food-culture platform as capacity expands. The evidence should show up in Miryang Plant 2 utilization, China inventory normalization, and European revenue contribution.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224141379485

- Source 2: https://www.judal.co.kr/?view=stockAI&shareToken=PD35uNOqwY4b9hEx

- Source 3: https://www.youtube.com/watch?v=zrrV5ae1euc

- Source 4: https://www.kedglobal.com/beauty-cosmetics/newsView/ked202508120003

- Source 5: https://www.mk.co.kr/en/business/11455307

- Source 6: https://www.koreaherald.com/article/10606118

- Source 7: https://biz.chosun.com/en/en-finance/2025/12/30/RCIEQKZUTRHZLGQZOKWRBEO4RM/

- Source 8: https://koreajoongangdaily.joins.com/news/2025-11-14/business/industry/Despite-tariffs-overseas-ramyeon-sales-remain-hot-for-Samyang-and-Nongshim/2454820

- Source 9: https://www.mt.co.kr/stock/2025/11/17/2025111708371417109

- Source 10: https://www.etoday.co.kr/news/view/2543150

- Source 11: https://www.etoday.co.kr/news/view/2543001

- Source 12: https://www.youtube.com/shorts/FNoPojfXVqs

- Source 13: https://www.ksdaily.co.kr/news/articleView.html?idxno=107908

- Source 14: https://www.businesspost.co.kr/BP?command=article_view&num=409664

- Source 15: https://drive.google.com/open?id=1eRhyUlQqqzcNSdlN6MTQL1UlDO5C_Fiq

- Source 16: https://www.businesskorea.co.kr/news/articleView.html?idxno=260162

- Source 17: https://www.chosun.com/english/industry-en/2025/06/12/LDQCKULERJH75J7KEDFQ5P6AGY/

- Source 18: https://drive.google.com/open?id=19aYk4GZmaivqSCix1kFeebrppPP6R85j

- Source 19: https://www.junggi.co.kr/article/articleView.html?no=35140&cate1=9&prevPagename=mainList.html&page=

- Source 20: https://biz.chosun.com/Z4UNLGBFLRCTHCTNAI34SGLK3A

- Source 21: https://drive.google.com/open?id=1qt0g4gSeusE14rSouiVGki97M3b2x2hd

- Source 22: https://www.e-science.co.kr/news/curationView.html?idxno=113246

- Source 23: https://ai.thebk.co.kr/news/articleView.html?idxno=659

- Source 24: https://ukragroconsult.com/en/news/palm-oil-market-to-remain-tight-in-2026-despite-supply-recovery/

- Source 25: https://www.fastmarkets.com/insights/palm-oil-price-forecast-and-production-outlook-2026/

- Source 26: https://graintrade.com.ua/en/novosti/eksperti-prognozuyut-znizhennya-tcin-na-palmovu-oliyu-u-2026-rotci.html

- Source 27: https://tradingeconomics.com/commodity/wheat/news/511032

- Source 28: https://simplywall.st/stocks/us/food-beverage-tobacco/otc-nfpd.f/nissin-foods-holdingsltd/valuation

- Source 29: https://www.investing.com/equities/nissin-foods-holdings-co-ltd

- Source 30: https://simplywall.st/en/stocks/jp/food-beverage-tobacco/tse-2875/toyo-suisan-kaisha-shares/valuation

- Source 31: https://biz.chosun.com/en/en-finance/2025/09/11/BCPUVRZN4VFC5EULV6CYNACSIM/