DEEP RESEARCH · PABLO AIR

PABLO AIR: Swarm Intelligence and the VOLK Merger as a Defense Platform Pivot

A review of Level 4 swarm control, UrbanLinkX, in-house manufacturing through VOLK, Pre-IPO valuation, and the 2026~2028 roadmap.

0. Bottom line first

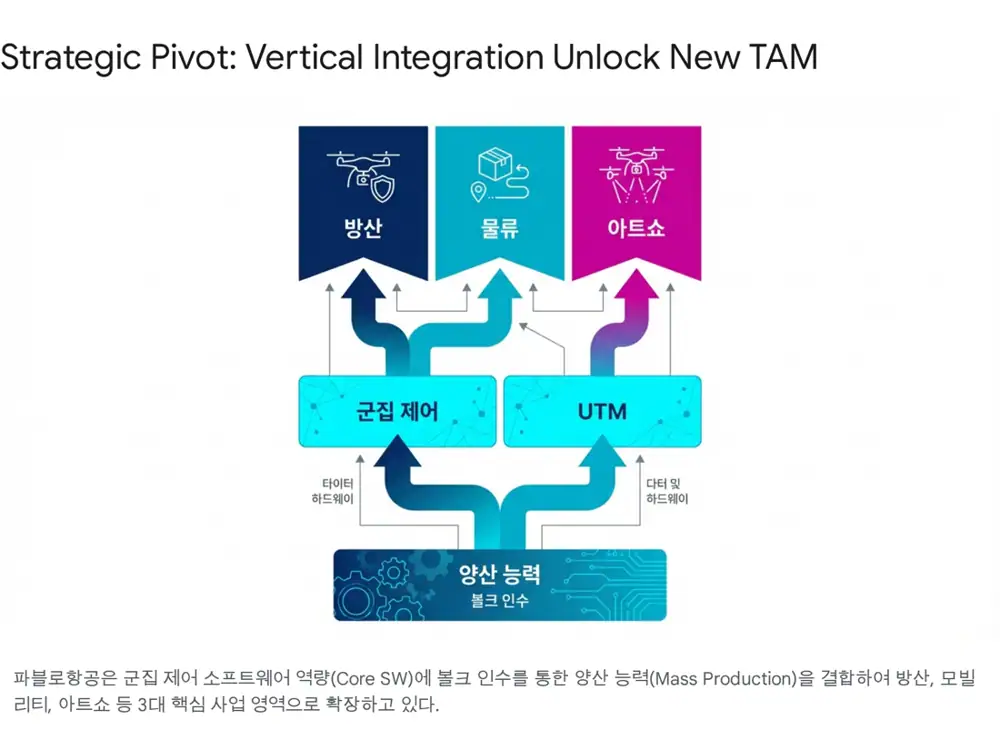

Viewing PABLO AIR only as a drone-art company misses the point. The source frames the company as being at an inflection point from software startup to defense manufacturing and platform company, combining Level 4 swarm-flight control and UTM technology developed since its 2018 founding with the 2024 merger of defense precision manufacturer VOLK.

Level 4 High Swarming

Data from operating hundreds to thousands of drones and distributed swarm control are presented as the core technical moat.

40 years of defense manufacturing

VOLK, founded in 1983, adds precision machining, procurement channels, and mass-production know-how.

2026 listing scenario

The source treats 2026 as the year of technology-special listing and defense mass production, and suggests a KRW 300~500B IPO market-cap scenario.

1. Founding story and technical heritage

Official fact: PABLO AIR was founded in August 2018 around CEO Young-joon Kim and is headquartered in Songdo, Incheon. The name PABLO was inspired by Pablo Picasso and reflects an early vision of combining technology and art. The source states that in about five years the company attracted cumulative investment of KRW 43B and reached a valuation around KRW 150B.

Public awareness began with drone art shows, but the source treats the core as swarm-flight algorithms and integrated control systems. Level 4 swarm flight includes distributed processing in which drones share position and status information and autonomously adjust routes and tasks rather than receiving every command sequentially from a central server.

2. Product portfolio: defense, performance, logistics

| Product/business | Source content | Meaning |

|---|---|---|

| PabloM | Defense and industrial lineup, including S10s swarm loitering drones and R10s wide-area reconnaissance | Main axis for defense electrification and policy tailwinds |

| PabloX | F40 firework drones and L20 LED drones | Marketing and cash-flow tool that stress-tests swarm technology |

| Logistics | Korea’s first convenience-store drone delivery center and pilots in Gapyeong | Validation of rural and island logistics potential |

| UrbanLinkX | Unified monitoring/control for drones, autonomous trucks, unmanned surface vessels, and more | K-UAM and smart-city control-platform option |

Interpretation: PABLO AIR’s strength is not one airframe. It is the ability to put multiple form factors and markets on the same control and swarm technology layer.

3. VOLK merger: from software to manufacturing-based platform

Official fact: In 2024, PABLO AIR merged with defense parts manufacturer VOLK. VOLK was founded in 1983 and has supplied cabinets, control equipment, drive equipment, and other precision-machined products for army, navy, and air-force weapons systems for more than 40 years.

Drone startups can be strong in design and prototypes but weak in uniform mass production that satisfies defense specifications. The VOLK merger is an attempt to complete an end-to-end value chain from R&D to manufacturing, operations, and MRO.

4. Financials and Pre-IPO valuation

| Item | Source figure | Interpretation |

|---|---|---|

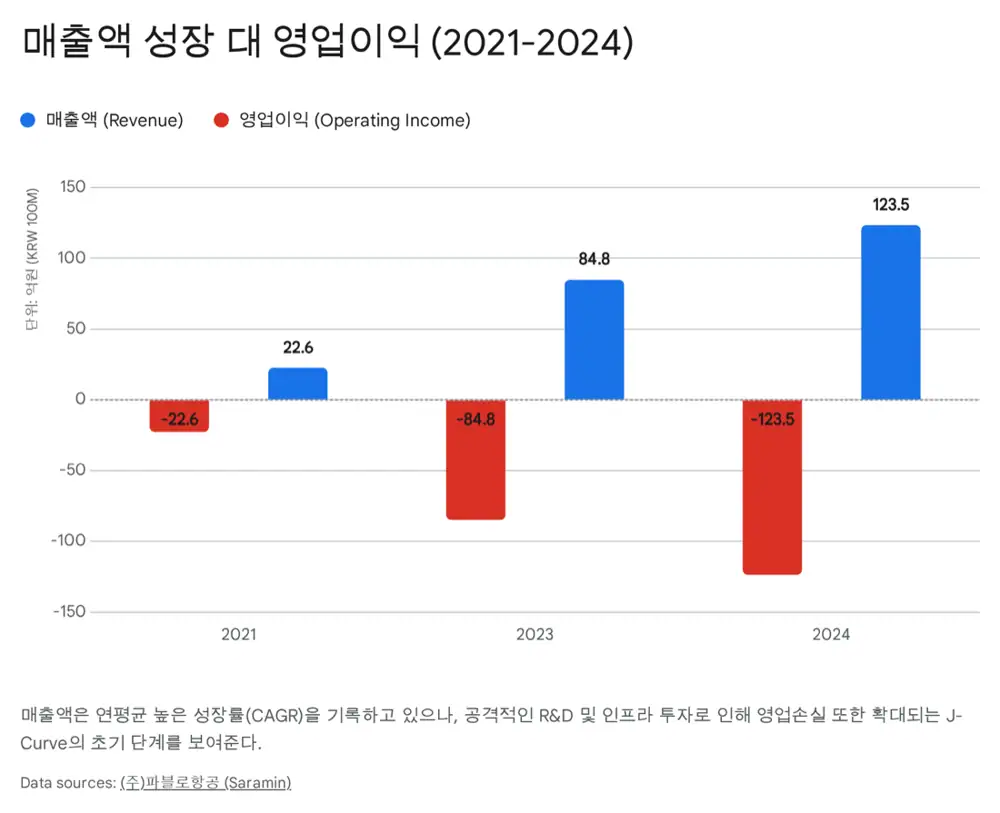

| Revenue growth | About KRW 2.2B in 2021, KRW 8.4B in 2023, KRW 12.3B in 2024 (+45%) | Growth from overseas drone-art orders, government R&D, and early defense revenue |

| VOLK contribution | VOLK revenue about KRW 32.7B in 2023 and expected KRW 40.0B in 2024 | Full consolidation in 2025 could lift revenue to KRW 50~60B |

| 2024 operating loss | About KRW 12.3B | Interpreted as growth pain from VOLK PMI, IPO staffing, R&D, and U.S./Middle East offices |

| Cumulative funding | About KRW 43B as of October 2023 | Capital-market validation of technology and expansion potential |

| Pre-IPO | KRW 21B raised in October 2023 at about KRW 150B valuation | Participation by KDB and Lee Soo-man highlights credibility and entertainment optionality |

| Listing scenario | Long-term KRW 5T vision; KRW 300~500B possible at 2026 listing per source | Technology-listing PSR, defense premium, and VOLK effect are key variables |

Interpretation: The important variables are not only the size of losses but burn rate and backlog growth. If VOLK revenue provides a financial buffer and defense mass production begins, the J-curve story becomes more credible.

5. Shareholders and competitive position

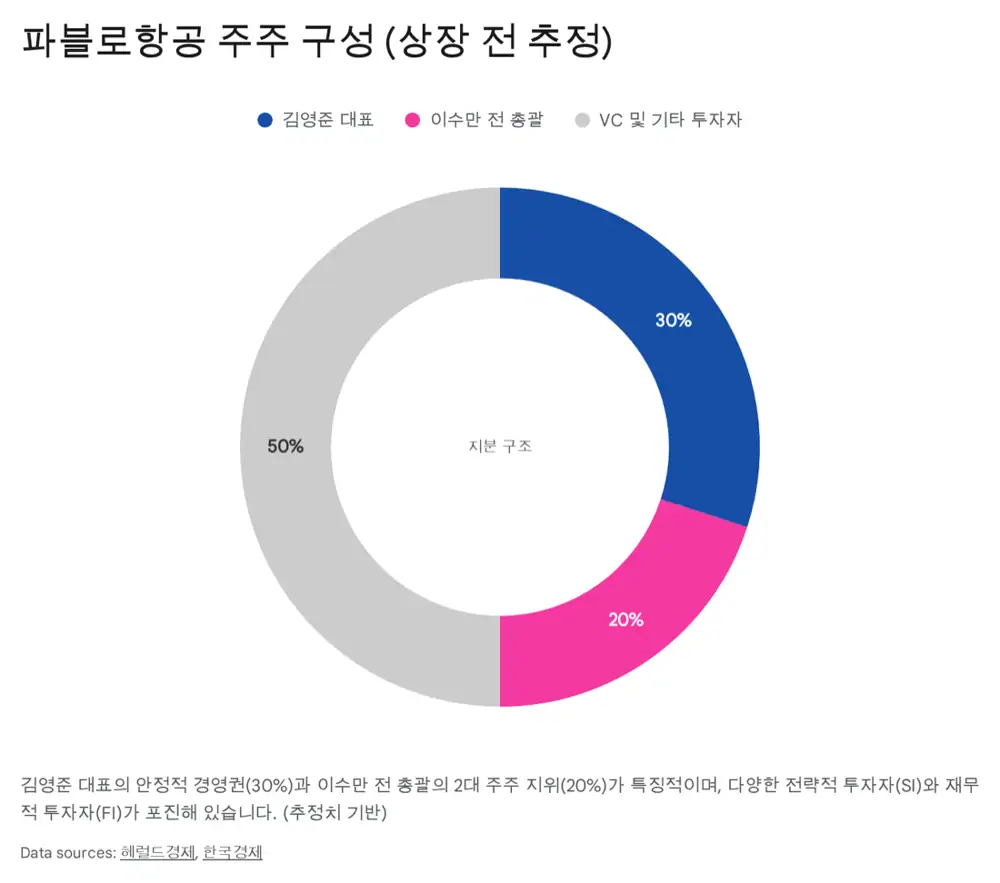

Official fact: The source presents CEO Young-joon Kim as the largest shareholder with about 30%, former SM executive producer Lee Soo-man as the second-largest shareholder with about 20%, and institutions/strategic investors at about 50%. Lee Soo-man is described as an early seed investor who invested KRW 1B in 2019.

| Category | PABLO AIR | Hancom InSpace | NeonTech |

|---|---|---|---|

| Core identity | Swarm intelligence and defense manufacturing platform | Satellite/ground-station data analytics and space | Industrial drone hardware |

| Technical strength | Level 4 Swarming, UTM, drone shows | Satellite imagery processing, AI analytics, space linkage | Airframe design, localized components |

| Major projects | ADD swarm UAVs, K-UAM GC-1 | Air Force Academy satellite development, Nuri payload | Navy target drones, reconnaissance drones, firefighting drones |

| Manufacturing | Highest after VOLK merger | Mainly software and system integration | Own production line |

| Scalability | Defense, performance, logistics | Space, defense | Defense, industry |

Interpretation: The differentiated point is turnkey capability across software and hardware. Data from operating hundreds to thousands of drones in shows, CES recognition, and Guinness records can serve as technology references for overseas buyers.

6. 2026~2028 growth roadmap

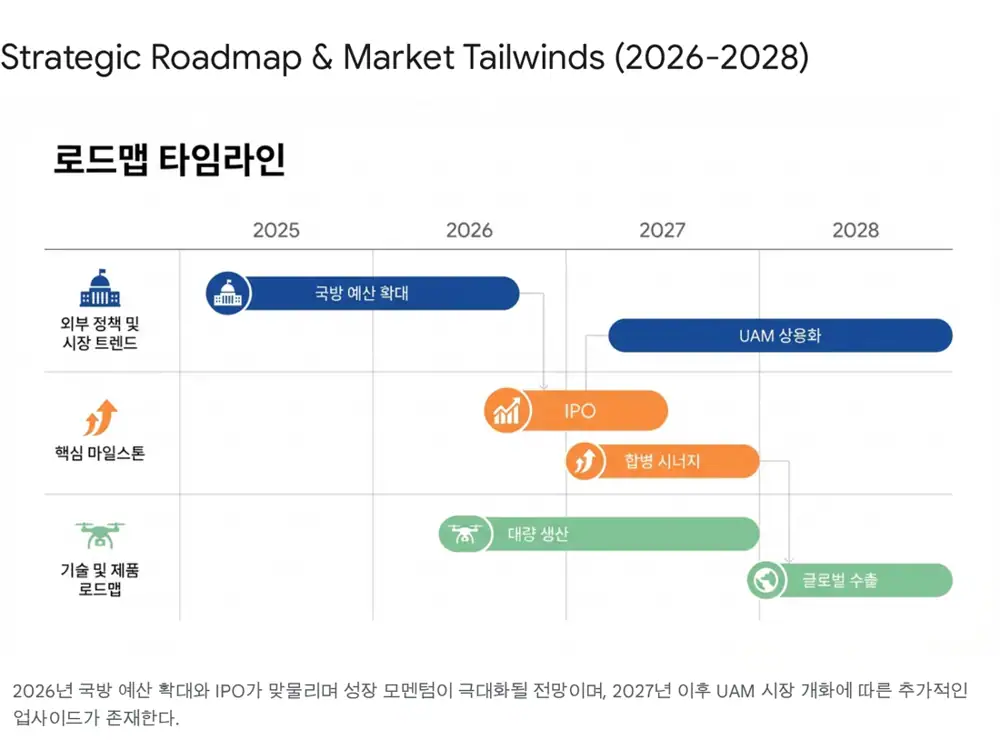

Official fact: The source expects drone deployment to reshape defense markets around 2026 and cites the Russia-Ukraine war as proof of drone value as asymmetric power. Korea’s 2026 defense budget proposal is described as emphasizing AI/drone soldiers and defense startups, with source materials mentioning KRW 65.8642T or KRW 66T.

| Phase | Goal | Source strategy |

|---|---|---|

| 2026 | IPO and first year of defense mass production | Technology-special listing, VOLK line expansion, and conversion of ADD swarm-UAV work into a mass-production model |

| 2027 | K-UAM commercialization and civilian expansion | Install UrbanLinkX, built with LG Uplus and GS E&C, at vertiports and create operating-fee revenue |

| 2028 | Global platform company | Target 50% defense export mix, export to Eastern Europe/Middle East, and make drone art a standalone cash cow |

7. Risks and final view

| Risk | Content | Mitigation logic |

|---|---|---|

| Cash burn | Aggressive expansion and IPO delay could cause dilution | Strengthen immediate-cash-flow businesses such as drone art shows |

| Regulatory delay | UAM and drone delivery depend on regulatory easing | Diversify revenue across defense, performance, and logistics |

| Overhang | FI profit-taking after listing could pressure the stock | Encourage long-term lockups from strategic investors such as Lotte and Lee Soo-man |

| Security/jamming | Electronic-warfare vulnerabilities could threaten defense orders | Security validation of swarm control and control platforms is required |

Interpretation: The investment logic is “software moat in swarm intelligence + manufacturing base from VOLK + post-2026 drone deployment.” Near-term losses can be viewed as growth cost, but without confirmed defense orders and mass-production revenue, valuation remains expectation-heavy. The source presents PABLO AIR as a top pick; this report records that as the source scenario, not as a recommendation.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224140959376

- 파블로항공 공식 사이트: https://www.pabloair.com/

- THE VC 파블로항공 기업정보: https://thevc.kr/pabloair

- Investing.com/MoneyS 볼크 합병: https://kr.investing.com/news/stock-market-news/article-1607178

- YouTube 2026 국방예산: https://www.youtube.com/shorts/3Ov5zp6lb9U

- 한국병무정책학회 국방예산: https://www.mhrd.kr/bbs/board.php?bo_table=latest_policy&wr_id=763

- 파블로항공 210억 프리 IPO: https://www.pabloair.com/kr/news/news.php?bgu=view&idx=127

- 더코리아저널 김영준 대표 인터뷰: http://thekoreajournal.com/View.aspx?No=3563940

- NEWDOT 드론 배송 아시아 랭킹: http://newdot.it/user/articleView?aaNo=709

- 모바일한경 이수만 투자: https://plus.hankyung.com/apps/newsinside.view?aid=202305221229r&category=&sns=y

- AI타임스 프리 IPO 210억: https://www.aitimes.com/news/articleView.html?idxno=154508

- 와우테일 85억원 투자유치: https://wowtale.net/2021/07/08/27848/

- 이데일리 마켓인 프리 IPO: https://marketin.edaily.co.kr/News/Read?newsId=01220166635775216

- Daum 이수만 투자 수익: https://v.daum.net/v/43xEGo6FeW

- 에너지경제신문 볼크 M&A 완료: https://m.ekn.kr/view.php?key=20250929023151804

- IT조선 2026 국방비: https://it.chosun.com/news/articleView.html?idxno=2023092152169

- 와우테일 K-UAM 그랜드챌린지: https://wowtale.net/2024/10/28/231919/

- 한국상장회사협의회 의무보호예수제도: http://www.klca.or.kr/KLCADownload/eBook/P6145.pdf?Mode=PC