DEEP RESEARCH · AFINIT (FORMERLY BALANCE HERO)

Afinit: A Full-Stack AI Inclusive-Finance Platform for India's Next Billion

From a utility-balance app to a full-stack AI lending platform — proprietary alternative credit scoring and a Korea-India arbitrage structure

0. Bottom line first

Afinit is a full-stack AI lending platform filling India's credit gap. Three moats — a proprietary alternative-credit-scoring (ACS) engine, Korean capital backing, and an RBI-regulated NBFC license — are reinforced by a fundamentals shift: a turn to profit plus 70% revenue growth. A first-half 2026 Korea listing would offer global investors a scarce "India growth proxy."

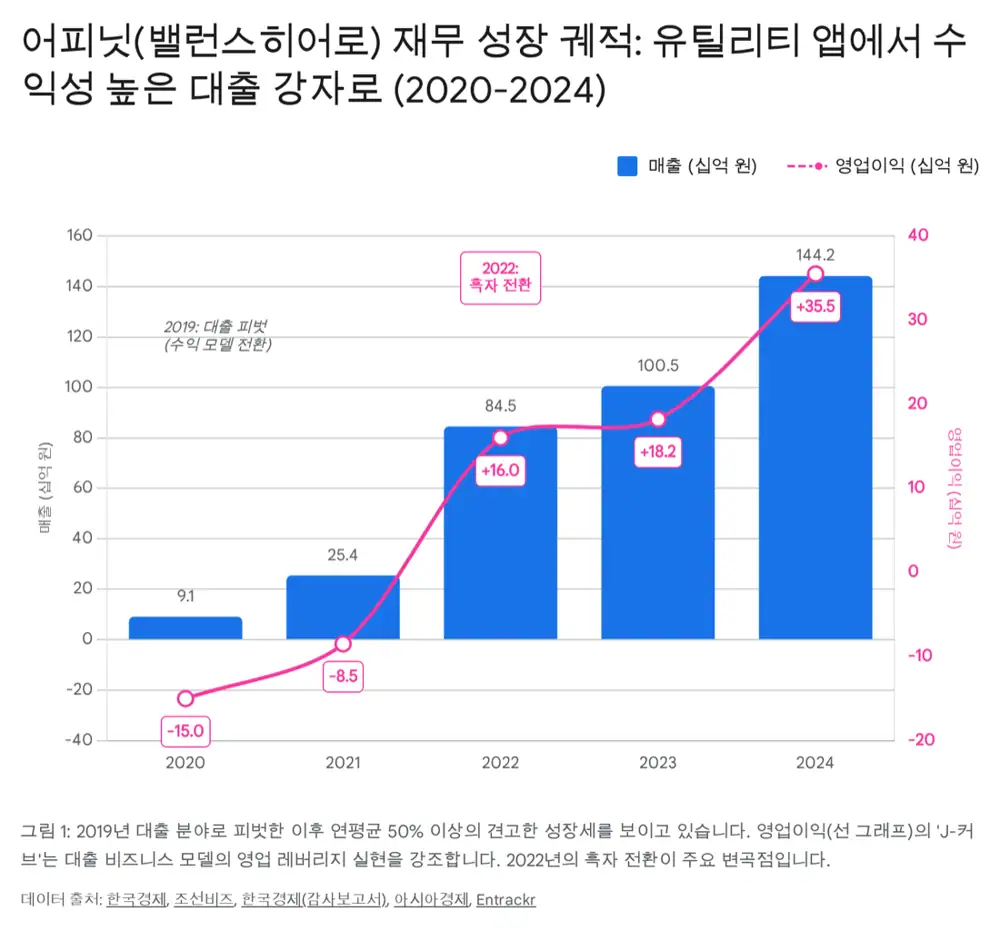

Official fact: 2024 revenue was about KRW 144.2 billion (+70% YoY) and operating profit was about KRW 35.5 billion (+121%). The Series D raised USD 28 million (about KRW 30 billion), and a recent press valuation came in around KRW 370 billion.

Interpretation: Top-line growth and operating leverage are arriving together. The high-yield structure of India's unsecured micro-lending market, combined with risk management through Afinit's own NBFC, drives a different trajectory from the "loss-funded growth" fintech pattern.

1. Identity and mission

Afinit is the rebrand of Balance Hero, a fintech operating the True Balance app in India. The new name encodes AI + Finance + IT — an intent to leap from a consumer app to an AI-centric financial platform. The headquarters is in Seoul while core operations sit in Gurugram, India — a classic cross-border setup.

The mission is "Finance for All." The target is India's Next Billion Users (NBU) — about one billion people who own smartphones and have bank accounts (thanks to Jan Dhan Yojana) but lack the credit history needed to borrow from incumbent banks like HDFC or SBI.

2. Business-model evolution in three stages

Official fact: The Stage 1 USSD-based balance-check app worked without an internet connection, hit 10 million downloads in 19 months, and built a data moat that grew to 85 million cumulative downloads.

Official fact: After moving into Stage 2, lending was executed directly via the True Credits Private Limited subsidiary to earn net interest margin, and the first annual operating profit was achieved in 2022.

Official fact: Today the platform-revenue share is about 32% as the Loan Service Provider (LSP) role expands.

3. Three economic moats

A. ACS engine (alternative credit scoring)

Scores users who are invisible to CIBIL. With user consent, the engine analyzes thousands of non-financial signals — recharge regularity, installed apps, social graph quality, activity timing — to estimate probability of default. It learns from more than KRW 2 trillion of cumulative loan disbursements.

B. Korea–India bridge

Access to Korean capital (SoftBank Ventures Asia, Naver, Shinhan Capital) translates into survival power through funding winters and acts as an underwriting signal for global follow-on rounds and the IPO.

C. License & compliance

Holds an RBI-licensed NBFC (True Credits) and a PPI (prepaid payment instrument) license. As the RBI tightens its 2025 Digital Lending Guidelines and non-compliant players exit, Afinit gains share by being on the right side of the rules.

4. What three years of cash flows mean

Afinit's cash flows follow the typical "growth-stage financial company" pattern.

- Operating cash flow (CFO): Loan disbursements are cash outflows, collections are inflows, so headline CFO can be negative or volatile. Disbursements in 2024 were roughly 13× the 2020 level, making accounting CFO largely a working-capital investment. On a pre-provision operating profit (PPOP) basis the cash generation is strongly positive, evidenced by sustained profitability since 2022.

- Investing cash flow (CFI): Persistently negative — driven by intangible R&D (ACS upgrades, LLM development) and data infrastructure/server costs. Over the last eight quarters AI/ML investment has scaled fast, supporting a "tech company" rather than a pure-lender valuation.

- Financing cash flow (CFF): Persistently positive. Equity funding (Series D, etc.) combines with True Credits' local borrowings and NCD issuance. Recent gearing of roughly 1.4–1.8× shows the leverage-driven asset growth strategy is working.

5. Who the customer is — the Next Billion User (NBU)

Young earners on USD ~200–600/month

INR 15,000–40,000 monthly income, ages 20–35. Self-employed, gig workers and early-career employees in Tier-2 and Tier-3 cities.

Bank account, no credit card

They previously relied on friends or informal money-lenders for short-term cash. Afinit gives them their first formal loan and builds their credit history.

Level-Up loans

Small-ticket loans whose limit grows as repayment history builds. Repeat-use rate exceeds 70%, offsetting high acquisition cost.

6. Corporate history

- 2014: Founder & CEO Cheolwon Lee establishes Balance Hero with an initial vision of "mobile cost optimization."

- 2016: True Balance app launches and reaches 10 million downloads in 19 months.

- 2017–2018: Payments expansion (mobile top-up, bill payments) and RBI PPI license.

- 2019: The Great Pivot from payments to lending; NBFC license obtained.

- 2020–2021: Series D (USD 28 million) closed amid COVID-19. Crisis-period repayment data sharpens the ACS model.

- 2022: First annual operating profit (BEP).

- 2023–2024: Rebrand to "Afinit" and AI-finance platform pivot; Mirae Asset and Hana Securities appointed IPO underwriters.

Key people: CEO Cheolwon Lee previously led RealNetworks Asia-Pacific and has worked the Indian telecom market (color ring services) since the early 2000s. Souparno Bagchi and others handle localization and regulation.

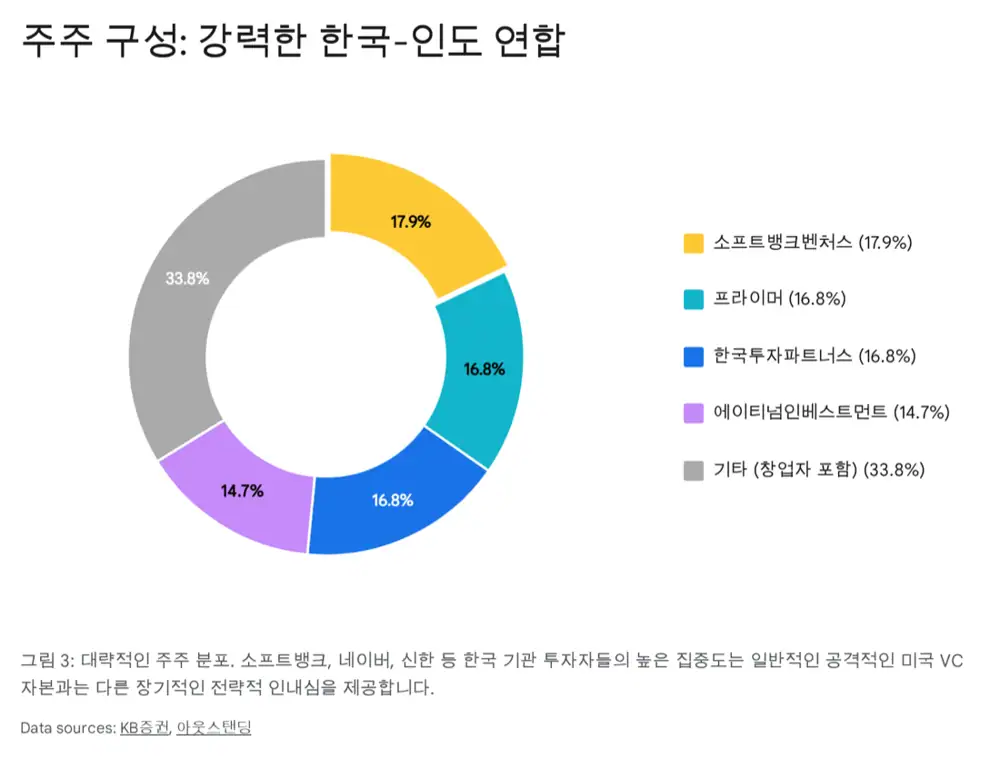

7. Funding history and shareholders

Series C in 2019 (~KRW 26 billion) seeded the lending business, followed by Series D in late 2020 raising about KRW 30 billion (USD 28 million).

| Shareholder | Stake / nature | Strategic value |

|---|---|---|

| SoftBank Ventures Asia | ~17.9% | Synergy with India fintech/e-commerce portfolio (Paytm, Flipkart, Meesho); a signal for follow-on rounds |

| Naver | Strategic investor | Potential to combine HyperCLOVA-class LLM tech with ACS |

| National Pension Service (NPS) | Indirect via VC LP | Sovereign-grade credibility |

| KDB, Shinhan Capital, Primer, Korea Investment Partners | Top-tier Korean VCs | Friendly book for a Korean listing |

8. Competitive landscape

India's digital lending market is both a red ocean and highly segmented.

- Tier 1 (prime customers): HDFC Bank, ICICI Bank, Cred, Navi — CIBIL 750+, bank-grade APR 10–15%; not direct Afinit competitors.

- Tier 2 (NTC / near-prime — Afinit's battleground): KreditBee (the strongest peer, backed by Premji Invest), Kissht (specialized in checkout finance for appliances), mPokket (students and first-jobbers, smaller ticket), CASHe.

| Dimension | Afinit (True Balance) | KreditBee | Traditional NBFC |

|---|---|---|---|

| Data source | ACS (telecom/device/behavior data) | CIBIL + bank statements | CIBIL-dependent |

| Core target | Prepaid-phone users (Tier 2/3) | Urban employees (Tier 1/2) | Prime customers |

| Average ticket | Micro (₹1k–₹50k) | Mid (₹10k–₹300k) | Large (>₹100k) |

| Risk model | High Tech (AI) / High Touch | Digital only | Manual / Hybrid |

| Regulatory status | Own NBFC (True Credits) | Co-lending biased | Own balance sheet |

Interpretation: Afinit's decisive edge is "upstream data." KreditBee customers already have some bank-transaction footprint; Afinit captures users from their first digital transaction (a mobile top-up), pre-empting them and producing a lock-in effect.

9. Growth strategy and risks

Strategy — platformization and AI scale-up

- LLM development: Voice-based finance support in Hindi, Tamil, Bengali and other Indian languages — aimed at lowering mis-selling risk and improving collections.

- LSP system: An open API allowing other financial institutions to underwrite via Afinit's ACS.

- Expected impact: Higher platform-revenue mix → improved margins and balance-sheet risk dispersion.

Risks — Bull/Base/Bear

- Bull: IPO success + rising platform-revenue mix + share absorption from RBI tightening.

- Base: Profitability sustained, stable asset growth at 1.4–1.8× gearing.

- Bear: Higher RBI risk weights on unsecured personal loans curb capacity; if listing is delayed or pricing disappoints, RCPS holders could press redemption rights.

10. Why Afinit — the macro tide

If India's last decade (2014–2024) was the "Access" era (account opening, UPI), the next decade (2025–2035) is the "Asset" era. The government's Account Aggregator framework and the whitelisting of compliant fintechs (alongside the purge of illegal apps) systematically favor licensed players. Afinit's market is the "Data Rich, Credit Poor" generation.

- Real AI utilization: One of the few firms applying AI to the core financial task of underwriting, not just chatbots.

- Proven profitability: Demonstrating profit at the Bottom of the Pyramid, unlike most loss-funded fintechs.

- Clear exit: A first-half 2026 Korea IPO gives a concrete liquidity event.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224140872241

- THE VC — Afinit (True Balance) company profile: https://thevc.kr/afinit

- CARE Ratings — True Credits Private Limited: https://www.careratings.com/upload/CompanyFiles/PR/202508120816_True_Credits_Private_Limited.pdf

- CRISIL — True Credits Rating Rationale: https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/TrueCreditsPrivateLimited_May%2008_%202025_RR_366492.html

- Seoul Economic Daily Signal — Balance Hero plans Korean listing: https://signalm.sedaily.com/NewsView/2DCY88TFLP/GX11

- Korea Economic Daily — Balance Hero KRW 144.2bn revenue: https://www.hankyung.com/article/202503319012i

- Maeil Business — Balance Hero rebrand to "Afinit": https://www.mk.co.kr/news/business/11448964

- WOWTALE — BalanceHero Doubles Revenue and Loans in H1 2024: https://en.wowtale.net/2024/08/01/226178/

- Economic Times — True Balance raises USD 28 million: https://m.economictimes.com/tech/funding/true-balance-raises-28-mn-from-softbank-ventures-asia-bonangels-others/articleshow/79282994.cms

- KB Securities report: https://rdata.kbsec.com/pdf_data/20220304071752703K.pdf

- KPMG Pulse of Fintech H1'23: https://assets.kpmg.com/content/dam/kpmg/cn/pdf/en/2023/09/pulse-of-fintech-h1-2023.pdf

- ChosunBiz — Afinit valued at KRW 370bn in latest round: https://biz.chosun.com/stock/market_trend/2026/01/04/6SQ633EJRNBXXJ7HOGPATX4TMA/