DEEP RESEARCH · HANWHA SYSTEMS

Hanwha Systems: The Defense-Electronics Premium Built on Technology Independence

A combined view of Q3 2025 earnings, localization, Philly Shipyard, satellites/UAM, and DCF valuation.

0. Bottom line first

My core read is that Hanwha Systems' profit structure is not simple defense-platform sales. It sits in radar, combat systems, communications, and software IP. Q3 2025 consolidated profit was weighed down by Philly Shipyard costs, but the defense core still showed the power of technology independence with a 10.3% operating margin.

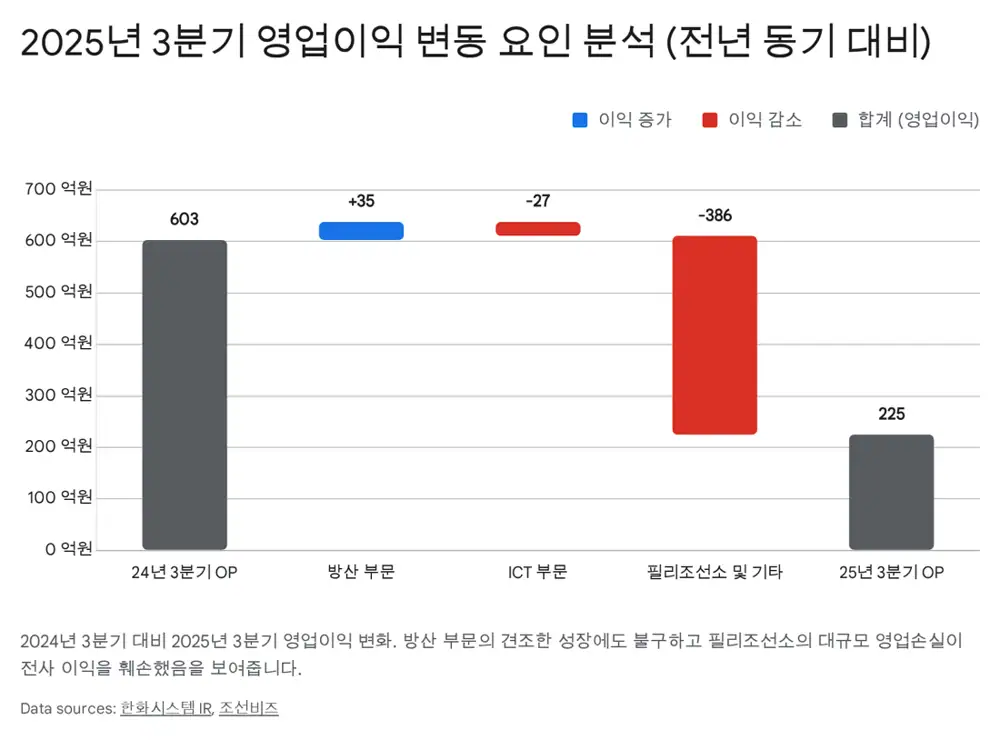

Official fact: The source cites Q3 2025 consolidated revenue of KRW 807.7B, up 26.4% YoY, and operating profit of KRW 22.5B, down 60.5% YoY. The defense segment generated KRW 481.4B in revenue, KRW 49.8B in operating profit, and 10.3% OPM. New businesses added KRW 170.6B of revenue from Philly Shipyard consolidation but recorded about KRW 39.3B of operating loss.

Interpretation: The consolidated profit decline should be read less as core-business deterioration and more as the effect of Philly Shipyard PMI and early operating losses. I treat it as the cost of entering U.S. Navy MRO and U.S. shipbuilding, while making 2026 normalization the key verification point.

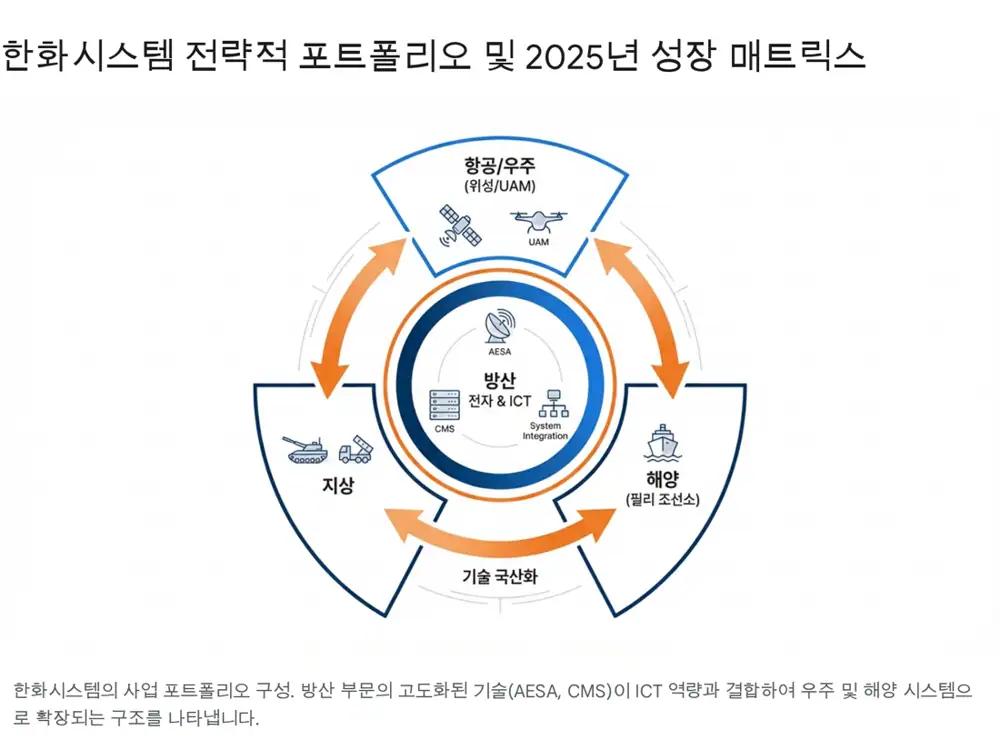

1. The defense-electronics paradigm shift

The source frames the 2025 global defense market as entering an expansion phase rarely seen since the Cold War. The prolonged Russia-Ukraine war, Israel-Hamas conflict, and tensions around the Taiwan Strait and Indo-Pacific are driving military spending, while K-defense has moved from cost-effective supplier to strategic partner with delivery discipline and technical reliability.

If first-generation K-defense exports focused on platforms such as self-propelled artillery and tanks, second-generation exports are shifting toward the electronic systems and software that determine platform performance. In network-centric warfare, the value of the brain and eyes that connect and control weapon systems rises faster than the value of hardware alone.

Combat management systems

Software-centered systems that connect vessels and platforms.

AESA radar

KF-21 and Cheongung-II MFR open mass-production and long-term MRO opportunities.

TICN communications

The fourth mass-production phase of the tactical information communication network supports stable revenue.

Interpretation: If Hanwha Aerospace and Hyundai Rotem build the body of the platform, Hanwha Systems supplies the nervous system and software that make the platform work. That position is the source of the valuation premium discussed in the post.

2. Q3 2025: growth and cost in the same quarter

| Item | Q3 2025 source figure | Read-through |

|---|---|---|

| Consolidated revenue | KRW 807.7B, +26.4% YoY | K-defense structural growth plus new-business consolidation |

| Consolidated operating profit | KRW 22.5B, -60.5% YoY | Philly Shipyard PMI and early losses |

| Defense segment | Revenue KRW 481.4B, operating profit KRW 49.8B, OPM 10.3% | Cheongung-II MFR, TICN, and KF-21 AESA mass-production transition |

| ICT segment | Revenue KRW 155.7B, operating profit KRW 12.0B | Base effect from Hanwha Aerospace ERP completion, with efforts to grow external orders |

| New business/other | Revenue KRW 170.6B, operating loss about KRW 39.3B | Philly Shipyard losses pulled consolidated OPM down to about 2.8% |

Official fact: In August 2025, the first mass-produced AESA radar unit for the KF-21 fighter was shipped. The source treats this as a transition from lower-margin development revenue to higher-margin mass-production revenue.

Interpretation: The surface number is profit decline, but the details show a resilient defense core. The issue is Philly Shipyard normalization. Whether the 2025 loss ends as entry cost or becomes a structural burden is the main re-rating fork.

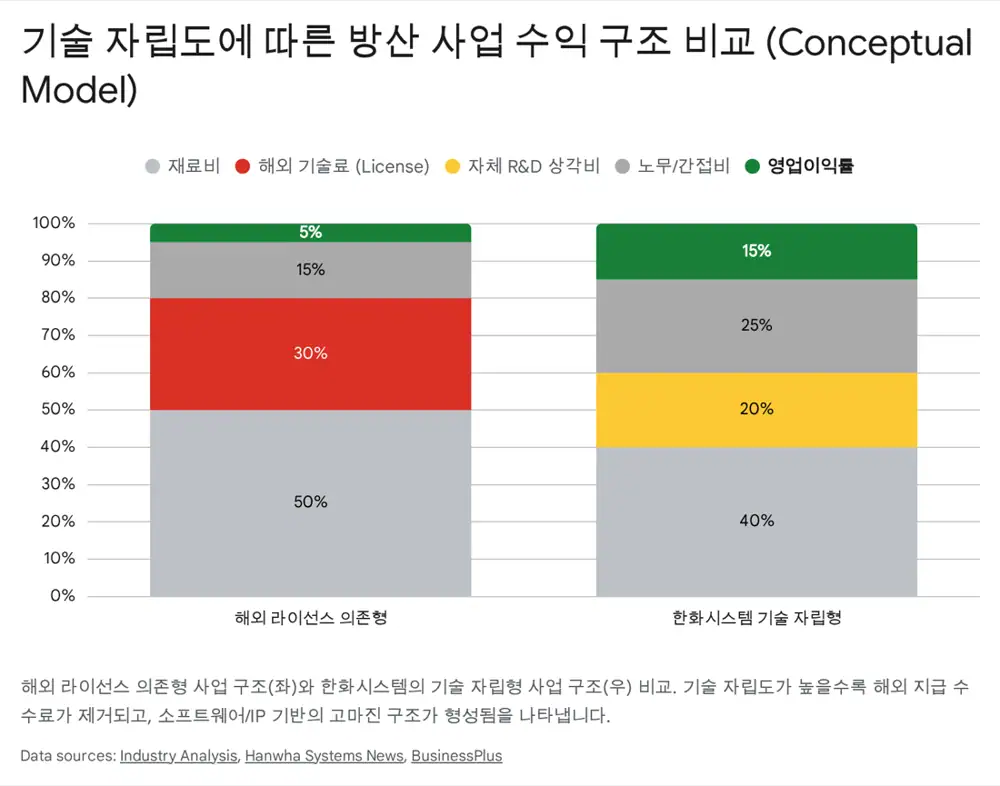

3. How localization affects margins and revenue recognition

The source's key variables are localization rate and technology independence. A higher localization rate means lower dependence on foreign license fees and imported components, while internally developed software and algorithms can turn revenue growth into operating leverage.

Official fact: Defense contracts usually recognize revenue by percentage of completion under K-IFRS 1115. Progress is measured as cumulative cost incurred divided by total estimated cost.

Interpretation: If core components depend on overseas partners, technology-transfer approval, export controls, and supply-chain bottlenecks can stop progress and delay revenue recognition. Because Hanwha Systems internalized key AESA radar and CMS technology, it can control schedules and cost input more directly, improving revenue visibility.

Peer comparison

| Company | Strength in the source | Margin-structure feature |

|---|---|---|

| KAI | Aircraft platform integration | Imported engines, ejection seats, and avionics create cost pressure |

| LIG Nex1 | Missile leadership | Consumable demand is attractive, but hardware manufacturing remains meaningful |

| Hanwha Systems | Platform brain: electronics and software | Upgrade demand and software mix leave more margin upside |

4. Philly Shipyard, satellites, and UAM: options with real cost

U.S. Navy MRO bridgehead

Hanwha Systems acquired a 60% stake in Philly Shipyard in December 2024. The source highlights its strategic value as a U.S.-based site protected by the Jones Act.

Jeju satellite hub

The source says Hanwha is building capacity to produce more than 100 satellites per year from the Jeju factory starting in 2026.

Selective focus

The Overair Butterfly commercialization timeline appears to have shifted beyond 2028, making avionics and UATM a more financially disciplined focus.

Official fact: The source says Philly Shipyard is losing money while clearing legacy low-priced orders, but management guidance and sell-side analysis expect most problematic orders to be cleared by the end of 2025 and a 2026 turnaround as NSMV and other new orders are recognized.

Interpretation: I treat Philly Shipyard as a valuation option, but one where cost is visible before upside. The satellite business depends on proprietary space semiconductors and expansion from B2G to B2B satellite communications. For UAM, narrowing the focus from airframes to avionics and traffic-management systems is financially more convincing.

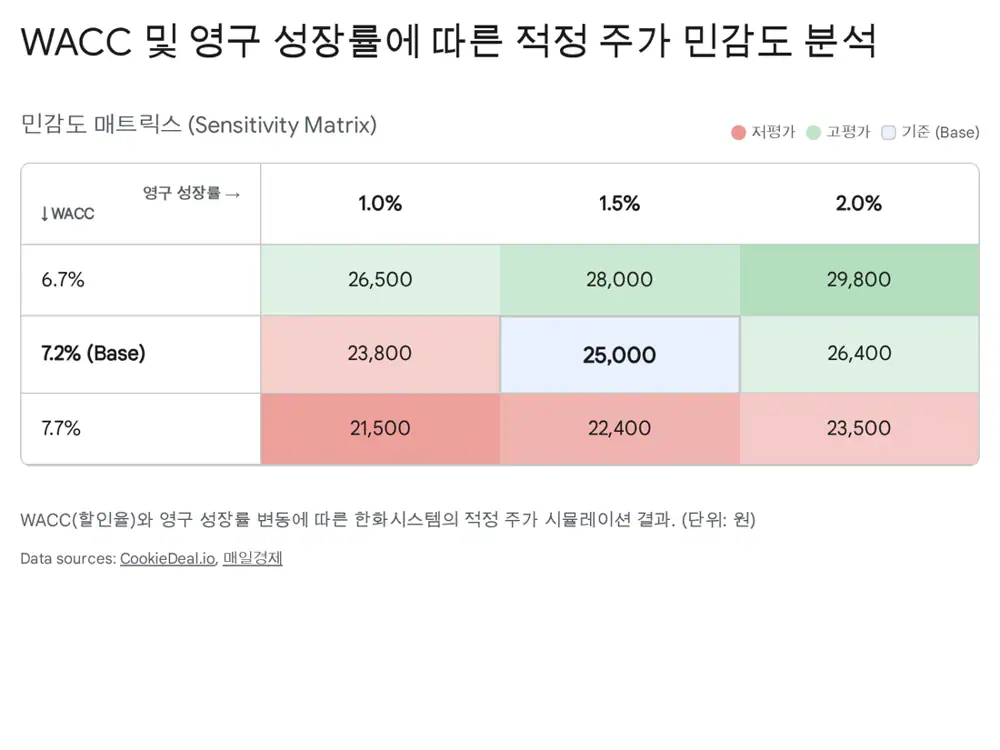

5. DCF valuation and risks

| DCF item | Source assumption/result |

|---|---|

| WACC | 7.2% |

| Risk-free rate | 3.5%, considering Korean 10-year government bond yield |

| Beta | 1.1, above the 0.8-0.9 defense-sector average for conservatism |

| Equity risk premium | 5.5% |

| Terminal growth | 1.5% |

| Operating value | About KRW 4.2T |

| Non-operating asset value | About KRW 0.5T |

| Net debt | About KRW 0.8T |

| Equity value | About KRW 3.9T |

| Shares outstanding | About 189M shares |

| Fair value per share | KRW 25,000, implying about 20-25% upside versus the current price in the source |

On FCF, the source treats 2025 as a transition year, with Philly Shipyard losses, PMI costs, and Jeju satellite-factory CAPEX suppressing free cash flow. It frames 2026-2027 as harvest years, when Philly Shipyard turnaround and KF-21 AESA mass-production revenue should lift operating cash flow.

Risk factors

- Delayed Philly Shipyard normalization: U.S. shipbuilding labor shortages and supply-chain issues could disrupt the 2026 turnaround scenario.

- Geopolitical reversal: If geopolitical tension eases, defense-demand sentiment could weaken temporarily.

- Internal K-defense competition: Overlapping business areas with LIG Nex1 and KAI could raise low-price bidding pressure.

6. Final view

Interpretation: My conclusion is that Hanwha Systems should be read less as a defense-parts maker and more as an integrated solution company with proprietary IP and electronics/software platforms. High localization and technology independence are the main evidence for superior margin and stable revenue recognition.

Near term, earnings damage from the Philly Shipyard acquisition looks unavoidable. I see 2025 as a foundation year for a potential 2026+ step-up rather than as a clean earnings year, but the key items to verify are Philly Shipyard turnaround, easing satellite-factory CAPEX burden, and repeatability of AESA mass-production revenue.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224140727737

- Daishin Securities/Daum: https://v.daum.net/v/0gsrd1cnNB

- Alpha Economy: https://alphabiz.co.kr/news/view/1065580180010310

- KAI analysis request: https://drive.google.com/open?id=1yt2mbERLWBGUENM96MOxkiuuxUfaJmxQaNzmMphYL0U

- Hanwha Systems company news: https://www.hanwhasystems.com/kr/prcenter/newsView.do?bbidx=459

- Business Plus: https://www.businessplus.kr/news/articleView.html?idxno=105011

- Toss Securities news: https://www.tossinvest.com/stocks/A272210/news?symbol-or-stock-code=A272210&contentType=news&contentParams=%7B%22id%22%3A%22newspim_20250207000585%22%7D&menu=news&contentPrev=%5B%5B%22disclosure%22%2C%7B%22id%22%3A%22kind_2025008397%22%7D%5D%5D

- Biztribune: https://www.biztribune.co.kr/news/articleView.html?idxno=328547

- MS TODAY: https://www.mstoday.co.kr/news/articleView.html?idxno=99824

- THE AI: https://www.newstheai.com/news/articleView.html?idxno=7536

- Cookie Deal WACC explainer: https://cookiedeal.io/blog/post/%EA%B0%80%EC%A4%91%ED%8F%89%EA%B7%A0%EC%9E%90%EB%B3%B8%EB%B9%84%EC%9A%A9-wacc-weighted-averge-cost-of-capital

- Hanwha Systems report: https://www.hanwhawm.com/main/common/common_file/fileView.cmd?category=2&depth3_id=anls1&key1=63956&key2=1&bldid=bbs10031

- Maeil Business Newspaper: https://www.mk.co.kr/news/stock/11059425

- Hanwha Aerospace deep-dive report: https://drive.google.com/open?id=1EN1e-i4kmZNLaQorDZlwu0EJoXi6_aI02syP_2bZQhI