DEEP RESEARCH · SUPREMA INC.

Suprema's Physical AI & Robotics Ecosystem: Strategic Pivot to Spatial-Intelligence Infrastructure

Why the Suprema AI merger, the Hyundai / Kia RTS partnership and BioStar X / CLUe reframe Suprema as a "spatial intelligence" platform

0. Bottom line first

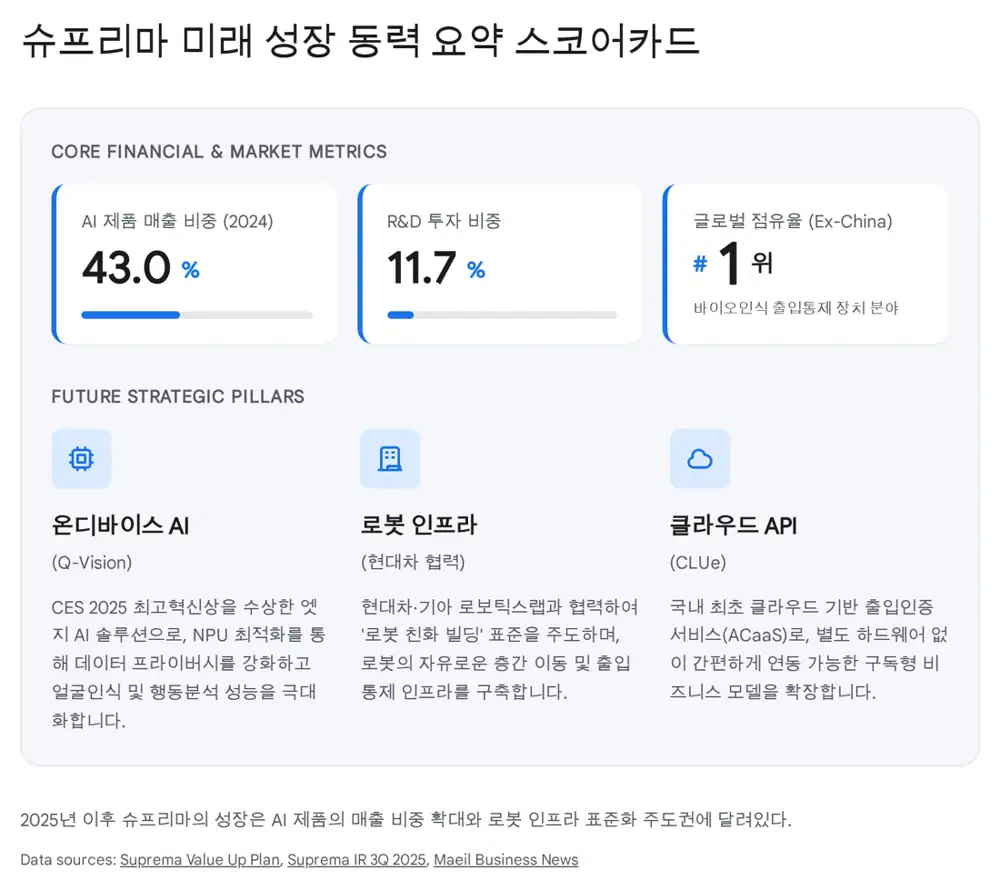

Suprema is rapidly outgrowing its "fingerprint reader company" label. The Suprema AI merger (Feb 2025) brought AI back into the parent, while the Hyundai / Kia RTS partnership secured the reference customer for "robot-friendly buildings." AI-product revenue mix jumped from 7.3% in 2020 to 43.0% in 2024.

Interpretation: This note applies the user's four-layer framework — sensor / edge, platform API, integrated control, security infrastructure — to Q-Vision Pro, CLUe / BioStar 2 API, BioStar X, and the Factorial Seongsu deployment.

1. Company overview — strong balance sheet behind the pivot

Official fact: 3Q25 revenue KRW 80.9 bn, operating profit KRW 19.3 bn. Gross profit margin sits in the mid-60s — a high-value technology profile rather than commodity hardware.

Official fact: Debt ratio 9.9% (effectively debt-free), current ratio 509%. 2024 R&D / revenue ratio of 11.7%.

Interpretation: The Suprema AI absorption is not mere consolidation — it (1) verticalizes hardware ↔ AI software, (2) redefines AI as part of the core "biometric solutions" line, (3) accelerates the path from R&D to revenue.

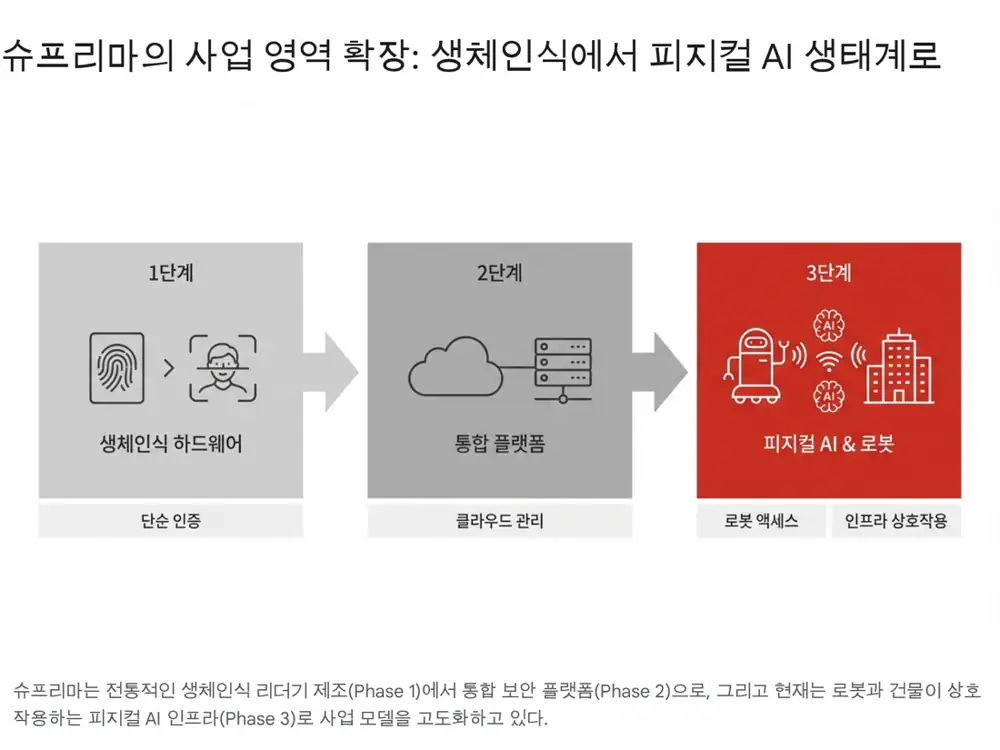

2. The four-layer Physical AI framework

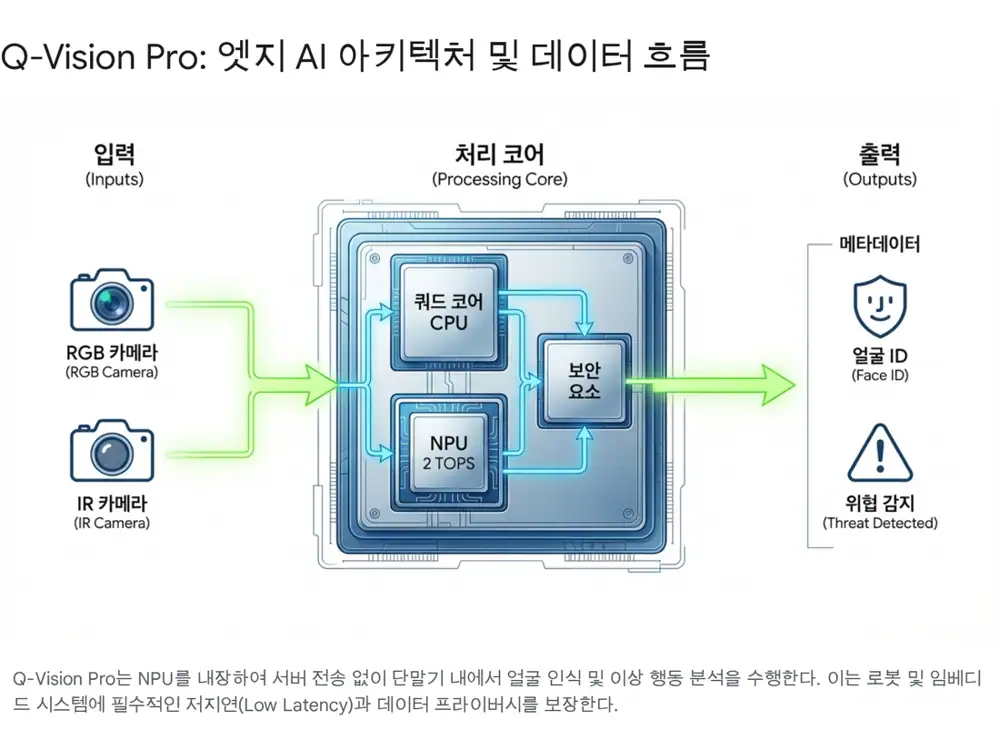

2.1 ① Sensor / edge — Q-Vision Pro

Q-Vision Pro

Runs AI inference at the device, removing latency and surviving network outages. Won CES 2025 Best of Innovation in Embedded.

Robot's "eyes"

Embedded into robots for face / gesture recognition and anomaly detection (loitering, intrusion, fall, weapons) → mobile guard role.

BioSign-derived algorithms

Low-power, lightweight algorithms originally built for smartphone fingerprinting — ideal for battery-constrained mobile robots.

2.2 ② Platform API — Suprema CLUe & BioStar 2 API

BioStar 2 API (on-prem): Internal-network TCP/IP integration for data centers and critical-infrastructure sites. Robots keep running even if external networks drop.

2.3 ③ Integrated control — BioStar X

- Unifies access control and VMS in a single dashboard.

- AI analyzes CCTV streams for robot malfunctions, tipovers and tailgating.

- Maps robot movement on a 3D building map.

- Scenario-based control — in fires / earthquakes, forces robots to safe zones.

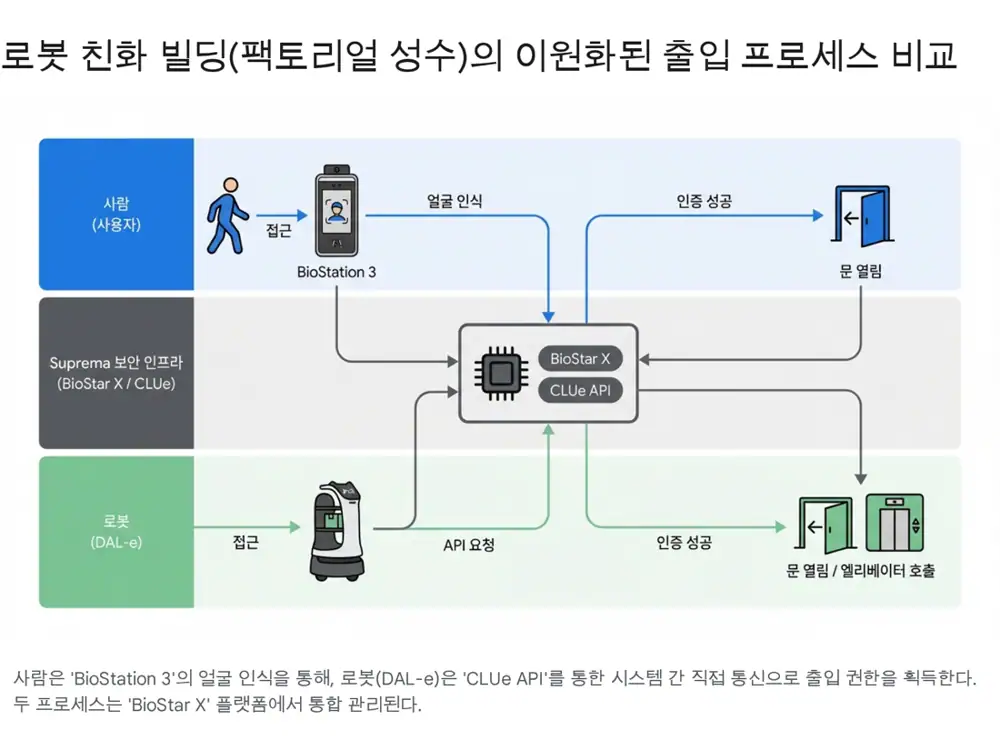

2.4 ④ Security infrastructure — Factorial Seongsu

Official fact: Factorial Seongsu in Seoul is Korea's first robot-friendly-building-certified smart office, where Hyundai / Kia's "DAL-e Delivery" and parking robots actually serve tenants.

- Human Flow: Employees walk through the speed gate via BioStation 3 face recognition without stopping.

- Robot Flow: DAL-e Delivery approaches the elevator lobby → Suprema receives the API signal → elevator is called, floor entered, doors opened automatically.

- Heterogeneous systems (robot fleet ↔ elevator ↔ access control) were successfully integrated, locking in the security reference for robot-friendly-building certification.

3. Hyundai / Kia RTS partnership

Official fact: March 2025 — MOU with Hyundai / Kia for a "Robotics & AI-based total security solutions" program.

- RTS (Robotics Total Solution): Robot hardware bundled with space-infrastructure. Suprema is the partner for the "security & access" module.

- Standards leadership: Joint development of robot-building integration standards → potential de-facto standard.

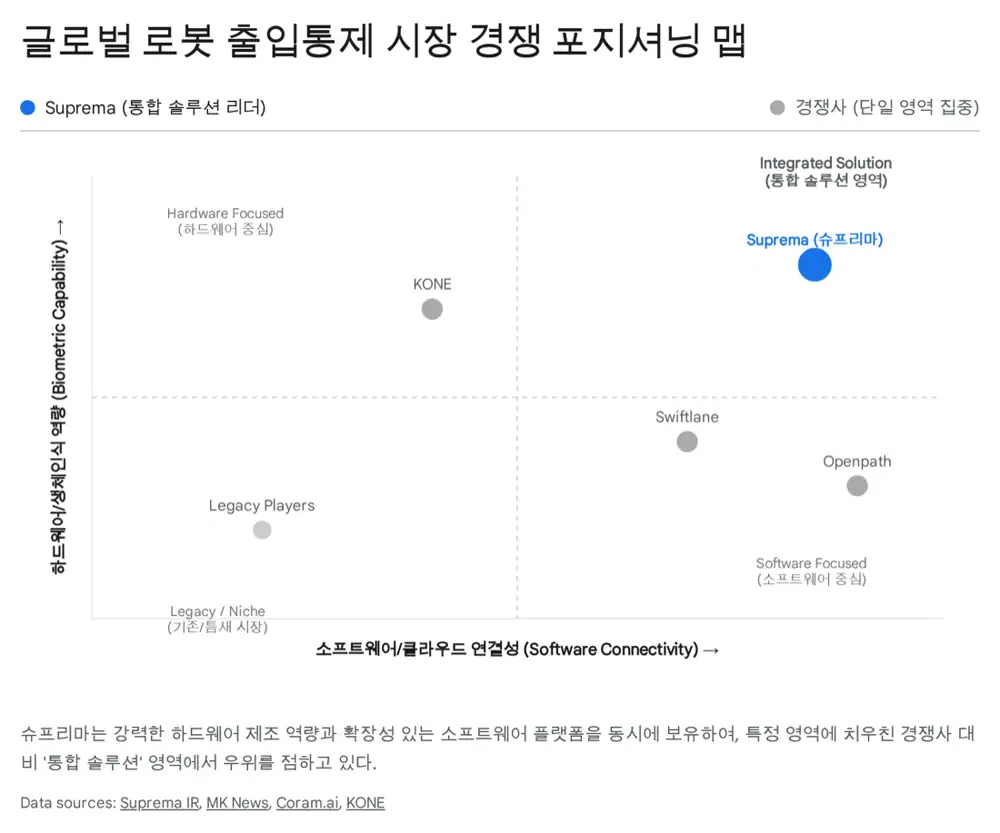

4. Global peers — the full-stack generalist

| Peer | Strength | Robot integration | Suprema's edge |

|---|---|---|---|

| KONE | Elevator market dominance, own API | Elevator API for vertical movement | Elevator + door + speed-gate + workforce — full-building security with biometrics |

| Openpath | Cloud-native, mobile credentials | Mobile SDK / open API | Edge hardware (Q-Vision Pro) + vertically integrated SW |

| Swiftlane | Video intercom + face recognition | Remote video intercom control | Enterprise-grade ISO 27001 / 27701, large-site references |

5. Financial impact and outlook

5.1 Quality of revenue mix

Official fact: AI-product revenue mix moved from 7.3% (2020) to 43.0% (2024). It is expected to cross 50% in 2025. BioStation 3 / FaceStation F2 carry far higher ASPs than commodity devices.

Interpretation: Cloud APIs like CLUe open a recurring-revenue (RMR) line. If usage-based billing scales, Suprema can be re-rated from a hardware multiple to a software-platform multiple.

5.2 Risks

- Construction cyclicality: Robot-friendly building deployments lean on new builds and large renovations → push retrofit-focused wireless / cloud solutions.

- Standards risk: Big-tech-led standards could fragment compatibility → maintain OSDP / international-standard compliance.

6. Conclusion — into the spatial-intelligence era

Suprema sits on three reinforcing pillars: (1) Q-Vision Pro / edge AI as a robot's perception layer, (2) the Factorial Seongsu reference for robot-building communication, (3) the financial proof of the pivot — AI mix >43%. Together they justify a re-rating from "security hardware" to "spatial intelligence" infrastructure.

Sources

- Original Naver blog post

- Suprema — Q-Vision Pro product page: supremainc.com

- CES — Q-Vision Pro innovation award: ces.tech

- Suprema — CLUe platform: supremainc.com

- Hyundai Newsroom — Suprema collaboration: hyundai.com

- BioStar 2 API: bs2api.biostar2.com

- Suprema — BioStar X: supremainc.com

- MK — Robot-friendly building partnership: mk.co.kr

- EconoVill — MOU signed: econovill.com

- DigitalChosun — Robot-friendly building expansion: digitalchosun.dizzo.com