DEEP RESEARCH · HANWHA AEROSPACE

Hanwha Aerospace: The Arsenal of Democracy at the Peak of a Structural Supercycle

A focused review of K9, Chunmoo, Redback, space and naval optionality, and the DCF case.

0. Bottom line first

My conclusion is that Hanwha Aerospace is being re-rated from a domestic defense supplier into a global tier-1 prime contractor with delivery speed, cost efficiency, and technological sovereignty. The source presents a BUY view and a KRW 480,000 target price, anchored in a KRW 100tn-plus backlog and export mix improvement.

1. Investment thesis: the K-defense trinity

Delivery alpha

While European competitors may require 3-5 years of lead time for self-propelled howitzers, the source argues Hanwha can deliver K9 units within months.

Export mix shift

The mix is moving from domestic procurement at 3-5% OPM to export contracts at 15-20% OPM.

Space and naval expansion

Hanwha Ocean consolidation and Nuri launch-vehicle work add long-duration optionality.

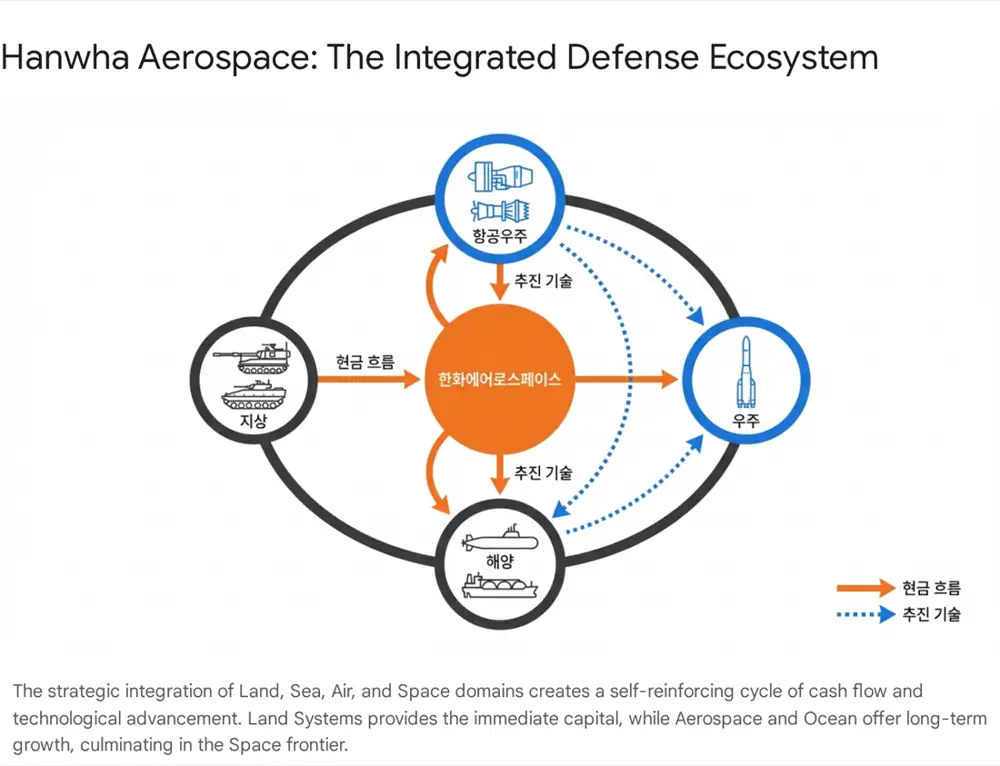

2. Business structure: land, aerospace, ocean, space

Official fact: The source says Hanwha Defense integration, the September 2024 spin-off of security and industrial equipment, and Hanwha Ocean acquisition established four pillars: land systems, aerospace, ocean systems, and space.

- K9 Thunder is presented as holding more than 50% of the global self-propelled howitzer export market.

- Redback is highlighted for winning Australia's LAND 400 Phase 3 against Rheinmetall's Lynx KF41.

- Chunmoo absorbs Eastern European demand with firepower and cost efficiency versus HIMARS.

- Aerospace rests on licensed F-15K, T-50, and KF-21 engine production and RSP participation with P&W and GE.

3. Technology sovereignty and hidden milestones

Interpretation: The moat in this post is not only product quality. It is availability and export-control freedom. Localizing the 1,000-horsepower K9 engine reduces German BAFA-related export-control risk for Middle Eastern opportunities.

- Next launch vehicle KSLV-III: Hanwha leads system integration and large liquid-fuel engine work after selection in late 2024.

- Submarine batteries: KSS-III Batch-II lithium-ion systems and solid-state battery R&D are framed as variables in Canadian and Polish tenders.

- Unmanned systems: Redback-based unmanned combat vehicles connect to manned-unmanned teaming.

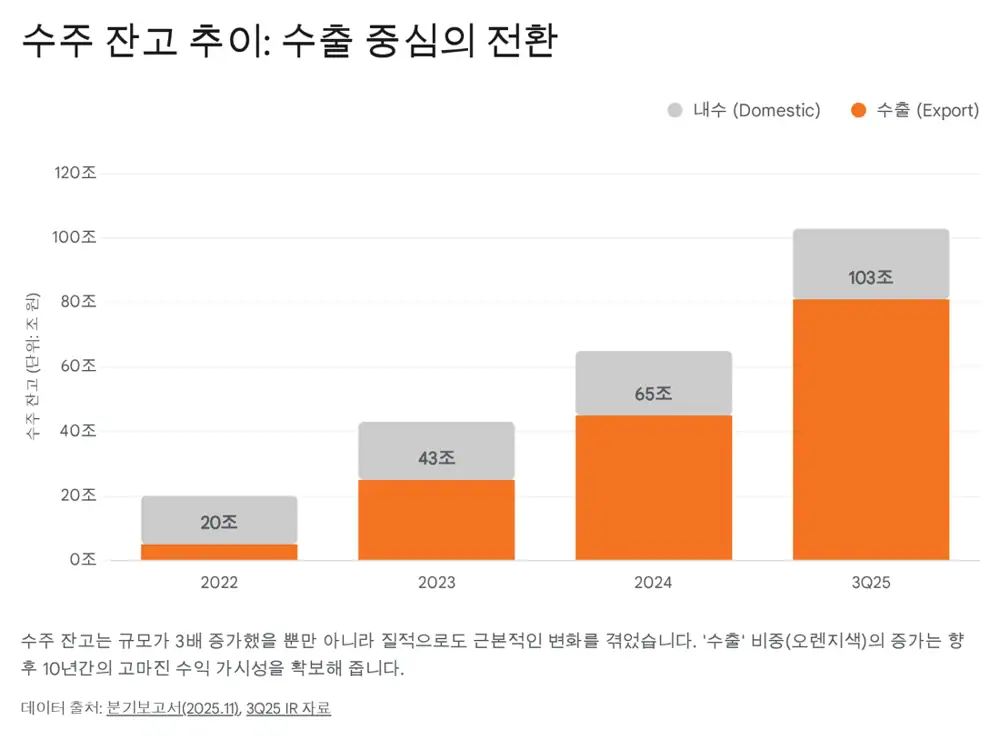

4. Orders and financials: KRW 100tn visibility

Official fact: The source reports consolidated backlog of about KRW 103.1tn at the end of Q3 2025, equivalent to about 9.2 years of work against 2024 revenue of about KRW 11.2tn.

| Item | Source figure/assumption | Meaning |

|---|---|---|

| Export OPM | 15-20% | Mix benefit versus domestic 3-5% |

| Q3 2025 cumulative revenue | About KRW 18.2tn, YoY about +185% | Hanwha Ocean and Poland deliveries |

| Q3 2025 cumulative operating profit | KRW 2.28tn | High-margin export delivery effect |

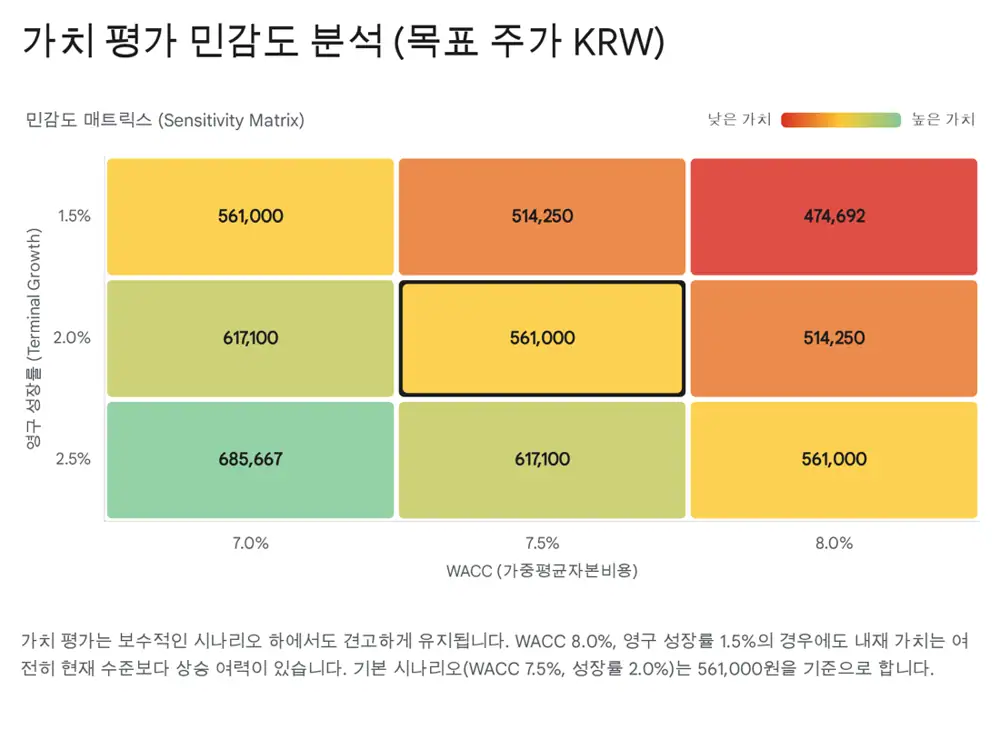

| DCF assumptions | Risk-free 3.39%, ERP 6.0% | Conservative discount framework |

| Final target price | KRW 480,000 | After 15% conglomerate/geopolitical discount |

5. Pipeline and risks

- Poland's second execution contract depends on the remaining roughly KRW 30tn and Export-Import Bank financing execution.

- Romania decided to acquire 54 K9 units for roughly USD 1bn, with Redback follow-on potential discussed.

- Canada's CPSP submarine project could reach up to 12 vessels and tens of trillions of won if won.

- Risks include delayed Polish financing, lower security premiums if geopolitical tension eases, and higher special steel, copper, and explosive-material costs.

6. My conclusion

I read the key point as backlog quality, not just backlog size. More delivery-based export revenue can raise quarterly volatility, but the operating leverage at delivery can structurally lift margins. For defense stocks, however, financing, diplomacy, input costs, and the war premium all matter, so execution risk deserves as much attention as the target price.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224139680803

- Source 2: https://www.hankookilbo.com/News/Read/A2025092908040002944

- Source 3: https://www.kari.re.kr/kor/contents/50

- Source 4: https://eiec.kdi.re.kr/policy/materialView.do?num=248763

- Source 5: http://www.healthtomato.com/view.aspx?seq=1235090

- Source 6: https://ko.tradingeconomics.com/south-korea/government-bond-yield

- Source 7: https://v.daum.net/v/20251121143120916

- Source 8: https://theguru.co.kr/news/article.html?no=96191