DEEP RESEARCH · KOREA AEROSPACE INDUSTRIES/KAI

Korea Aerospace Industries: A Structural Move Toward Global Aerospace Prime Status

A review of the 2026 revenue-recognition cycle driven by KF-21 production, FA-50 exports, and aerostructures recovery

0. Bottom line first

The source report argues that KAI is moving past the 2023-2025 revenue-recognition lag and into a 2026 cycle where KF-21 production, FA-50PL and FA-50M deliveries, and a civil aerostructures recovery begin to show in reported numbers. The source presents a BUY view, a KRW 185,000 target price, a KRW 142,800 current price, and +29.5% upside.

I read the core issue as timing, not just backlog size. The backlog was already large at KRW 26.2673 trillion as of 3Q25. The key question is whether the first KF-21 production delivery in 1H26 and resumed FA-50 export deliveries from 2027 convert that backlog into higher-margin revenue.

1. Business portfolio: four cash-flow pillars

Official fact: The source describes KAI as Korea's only complete-aircraft manufacturer. It can handle aircraft development, production, test flight, and follow-on support, with four business pillars: fixed-wing, rotary-wing, aerostructures, and future businesses.

T-50/FA-50 and KF-21

The T-50/FA-50 family is a trainer and light-attack aircraft line co-developed with Lockheed Martin. The source says it is well positioned for training pilots for the 4,000-plus F-16s operated globally, while KF-21 elevates KAI into a 4.5-generation fighter prime contractor.

Surion and LAH

KUH-1 Surion has expanded into amphibious, medevac, police, fire, and forestry variants. LAH began first production deliveries at the end of 2024 and has strategic value as a MUM-T platform.

Aerostructures

KAI supplies wing and fuselage structures for B787, A350, A320 and other aircraft as a Tier 1 partner to Boeing and Airbus. The source expects the 2025 recovery in passenger demand and OEM output to support cash flow.

Space and AAM

The pipeline includes next-generation medium satellites, geostationary multipurpose satellites, Nuri launch-vehicle upgrades, mass production of microsatellite SAR systems, and AAV development. The AAV target is detailed design in 2025 and first prototype flight in 2028.

Interpretation: Fixed-wing is the earnings lever, rotary-wing is the domestic stability base, aerostructures offers civil-market recovery and dollar exposure, and space/AAM is the long-duration option. The 2026 rerating is most sensitive to the revenue-recognition pace in fixed-wing and aerostructures.

2. Technology moat and global strategy

KAI's moat comes from regulatory and security barriers, localized avionics technology, and 30- to 40-year switching costs after aircraft adoption. The source argues that KF-21 localization of AESA radar, the electronic warfare suite, and mission computers reduces dependence on U.S. export licensing and improves flexibility for Middle Eastern and Southeast Asian exports.

Official fact: The source describes CEO Cha Jae-byeong as an engineer-turned-manager and says KAI proposed local production and technology transfer in the Egypt FA-50 talks. It also highlights performance-based logistics, pilot training, and maintenance training as service revenue sources.

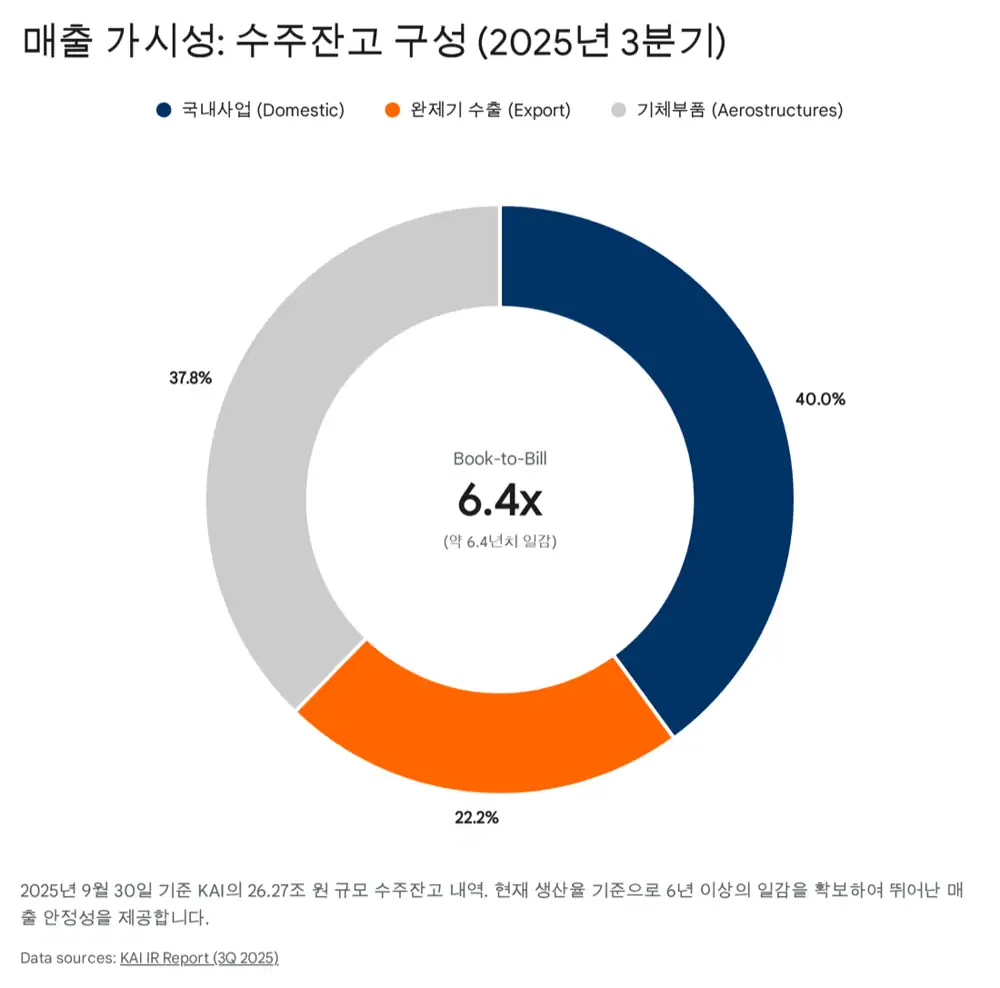

3. Backlog and future pipeline

Official fact: KAI's order backlog was KRW 26.2673 trillion at the end of 3Q25. Using the source's assumed 2025 revenue of about KRW 4.1 trillion, that equals roughly 6.4 years of work, well above the 2-3x revenue backlog level cited for global defense companies.

| Backlog component | Size/share | Source interpretation |

|---|---|---|

| Domestic | About 40%, KRW 10.5 trillion | KF-21 production and LAH deliveries. Government contracts carry lower OPM of 5-7%, but risk and cash-flow volatility are lower. |

| Exports | About 22%, KRW 5.8 trillion | Includes Poland FA-50PL and Malaysia FA-50M. The source sees export contracts as typically producing OPM above 10-15%, the key driver of margin improvement. |

| Aerostructures | About 38%, KRW 9.9 trillion | Boeing and Airbus civil-aircraft components, with FX benefits and fixed-cost absorption as volumes rise. |

The source estimates more than KRW 10 trillion of new-order pipeline for 2026-2027. Egypt's FA-50 opportunity is described as about 36 aircraft in the first phase and up to 100 aircraft, Slovakia is linked to the L-39 replacement program, the U.S. UJTS program is the “Blue Sky” case with KAI and Lockheed Martin proposing TF-50N, and the Philippines may discuss KF-21 deliveries around 2027-2029 after operating FA-50PH.

4. 3Q25 results and the 2026 inflection point

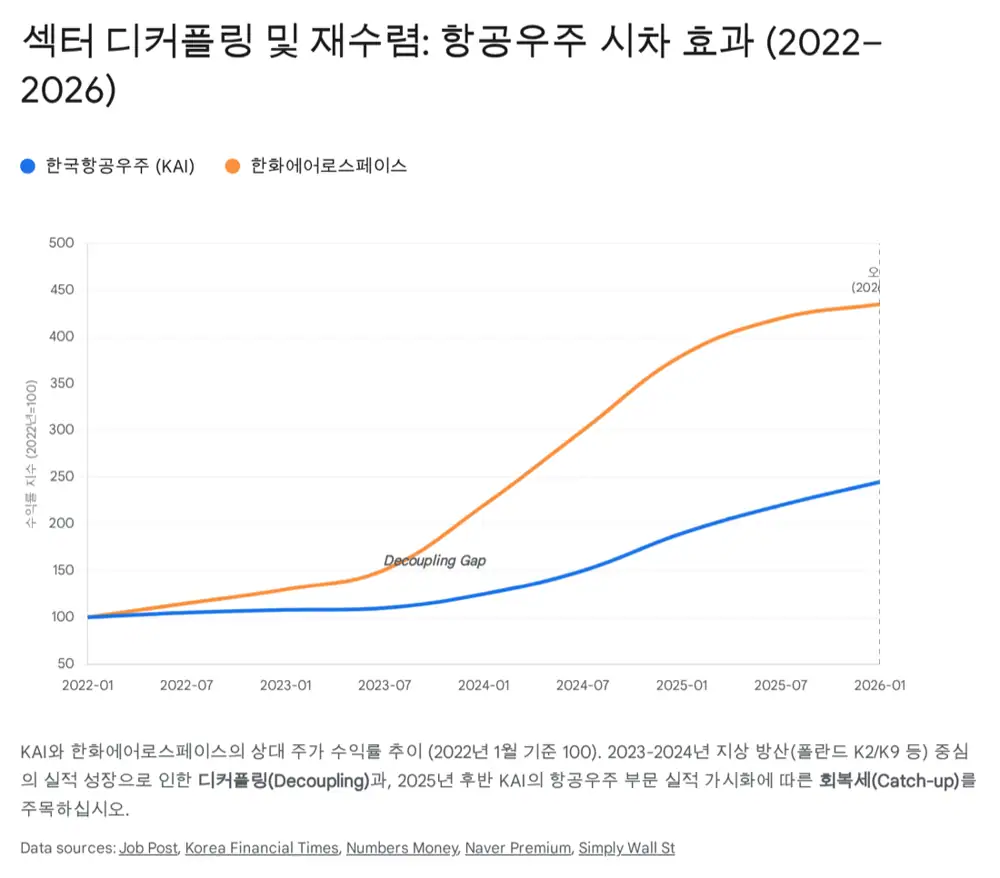

3Q25 revenue was KRW 702.1 billion, down 22.6% year over year, while operating profit was KRW 60.2 billion, down 21.1%. However, OPM improved by 0.16 percentage points year over year to 8.57%.

Interpretation: The source attributes the revenue decline to the concentration of 12 Poland FA-50GF deliveries in 2023-2024 and the revenue valley before follow-on FA-50PL development and production. I also see the key issue as what margin the production and export revenue earns after the valley, not the decline itself.

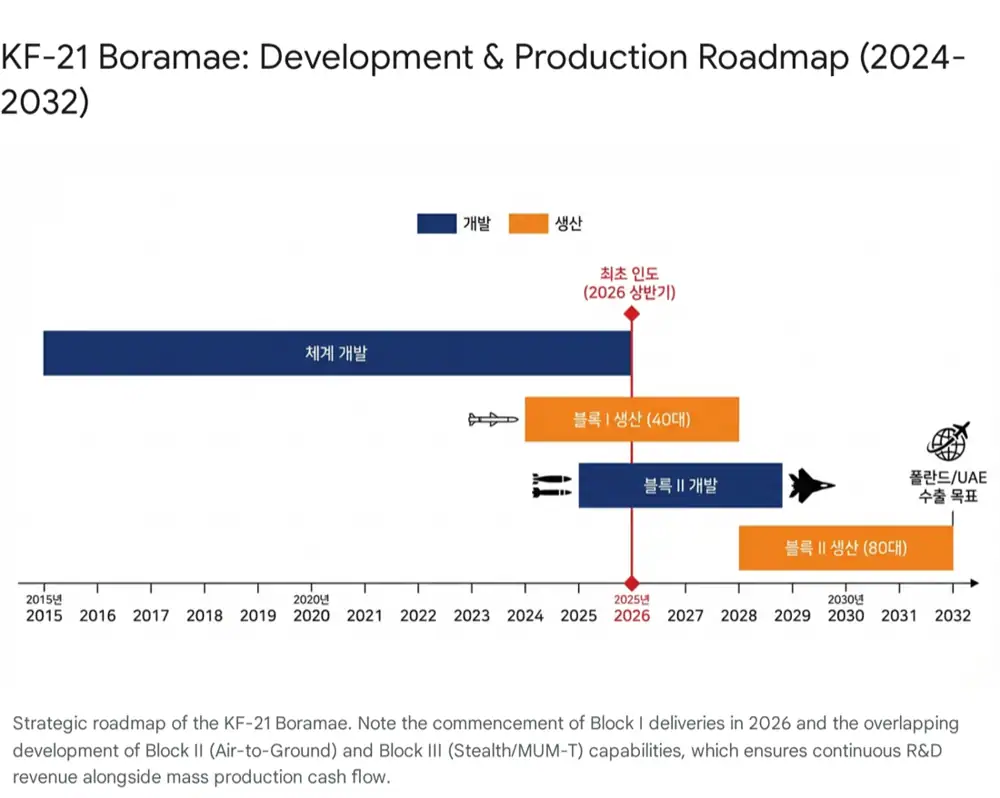

Why KF-21 is the rerating key

- KF-21 is presented as the driver that could shift KAI from a parts-manufacturer valuation of 10-15x P/E to a prime-contractor valuation above 20x P/E.

- Initial Block I assembly of 40 aircraft is underway, with the first aircraft expected to be delivered to the air force in 1H26.

- The source estimates more than KRW 1.5 trillion of annual KF-21 production revenue from 2026 to 2028.

- Block II air-to-ground development, the UAE MC-X joint-development MOU, and KF-21-linked MUM-T are listed as additional milestones.

5. DCF valuation: source assumptions preserved

Official fact: The source uses a discounted cash flow model as of January 8, 2026. Key assumptions are 2026-2030 revenue CAGR of 12.5%, OPM rising from 8.6% in 2025 to 11.5% in 2028, WACC of 7.2%, risk-free rate of 3.34%, beta of 0.70, market risk premium of 5.5%, after-tax cost of debt of 4.5%, and terminal growth of 1.5%. The beta is set above the historical five-year beta of 0.36 for conservatism.

| Item (KRW bn) | 2026E | 2027E | 2028E | 2029E | 2030E |

|---|---|---|---|---|---|

| Revenue | 5,254 | 6,150 | 7,200 | 7,950 | 8,600 |

| Growth | 28% | 17% | 17% | 10% | 8% |

| Operating profit | 507 | 657 | 828 | 954 | 1,032 |

| OPM | 9.6% | 10.7% | 11.5% | 12.0% | 12.0% |

| NOPAT | 395 | 512 | 646 | 744 | 805 |

| D&A | 220 | 230 | 240 | 250 | 260 |

| Capex | (450) | (400) | (350) | (350) | (350) |

| Change in working capital | (150) | (200) | (100) | (50) | (50) |

| FCF | 15 | 142 | 436 | 594 | 665 |

The source says 2026 FCF is low because working-capital investment is concentrated in advance purchases of titanium and other raw materials for KF-21 production and FA-50PL production. The DCF output is PV of FCF of KRW 1.35 trillion, PV of terminal value of KRW 16.85 trillion, enterprise value of KRW 18.2 trillion, net debt of KRW 1.88 trillion, equity value of KRW 16.32 trillion, 97,475,107 shares outstanding, and a fair price of KRW 167,400.

KRW 195,000

At WACC of 6.8%, assuming lower rates and export upside, the source says fair value could rise to KRW 195,000.

KRW 167,400

This is the base DCF result. The source's final KRW 185,000 target reflects both the DCF result and the possibility of the bull case.

KRW 135,000

At WACC of 8.0%, assuming easing geopolitical risk and order delays, the source still sees value around KRW 135,000 versus the current KRW 142,800.

6. Final view and risks

The source presents BUY and a KRW 185,000 target price. It frames 2026 as the start of the delivery supercycle, with more than KRW 1.5 trillion of annual revenue base from KF-21 production, strong FA-50 export momentum in Egypt and Slovakia, and post-2030 growth options from MC-X with the UAE and KAI's own AAV program.

Risks

- Export-Import Bank financing capacity: Large export deals such as Poland's second contract require government financing, and statutory capital-limit issues could delay orders.

- Geopolitical risk easing: A rapid easing of tension, including an end to the war in Ukraine, could weaken defense-sector sentiment.

- Raw materials and supply chain: Higher titanium and aluminum prices or delays in imported engines and other key components could hurt delivery schedules and margins.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224139667021

- Financial Times Korea article: https://www.fntimes.com/html/view.php?ud=202510131108032508141825007d_18

- FW-MAG KF-21 delivery article: https://www.fw-mag.com/shownews/565/kai-to-deliver-first-production-kf-21-in-2026

- AVING NEWS AAV article: https://us.aving.net/news/articleView.html?idxno=51523

- Hankyung Eureka KAI note: https://eureka.hankyung.com/insight/detail/15794

- Stockopedia KAI: https://www.stockopedia.com/share-prices/korea-aerospace-industries-KRX:047810/

- Africa Defense Forum Egypt article: https://adf-magazine.com/2025/11/egypt-south-korea-working-on-deal-for-jets/

- Hankyoreh FA-50 Europe export article: https://english.hani.co.kr/arti/english_edition/e_business/1017999.html

- Defence Security Asia Philippines KF-21 article: https://defencesecurityasia.com/en/philippines-kf21-boramae-delivery-2027-2029-south-china-sea-airpower/

- Reddit Philippines KF-21 discussion: https://www.reddit.com/r/LessCredibleDefence/comments/1q5zerk/philippines_requests_kf21_fighter_jet_delivery/

- Global Business Press MC-X article: https://gbp.com.sg/stories/kai-confident-of-market-potential-for-future-mc-x-transport-aircraft/

- Allied Market Research MC-X/UAE post: https://blog.alliedmarketresearch.com/the-development-of-the-korean-mC-x-military-transport-aircraft-has-received-a-funding-boost-from-the-uAE-as-there-is-a-growing-global-demand-for-advanced-cargo-planes-1297

- Trading Economics Korea 10-year yield: https://tradingeconomics.com/south-korea/government-bond-yield

- Stock Analysis KAI statistics: https://stockanalysis.com/quote/krx/047810/statistics/