DEEP RESEARCH · KOREAN AIR

Korean Air: The Hidden Defense Giant Taking Flight with Stealth UAVs

A re-check of aerospace and unmanned-system integration capabilities hidden inside an airline valuation

0. Bottom line first

The source reframes Korean Air not only as a flag carrier, but as an aerospace and unmanned-system integrator. The key catalysts are the aerospace division’s return to profit, cooperation with Anduril, the ADD low-observable loyal-wingman project, and improved cash-flow potential after the Asiana merger.

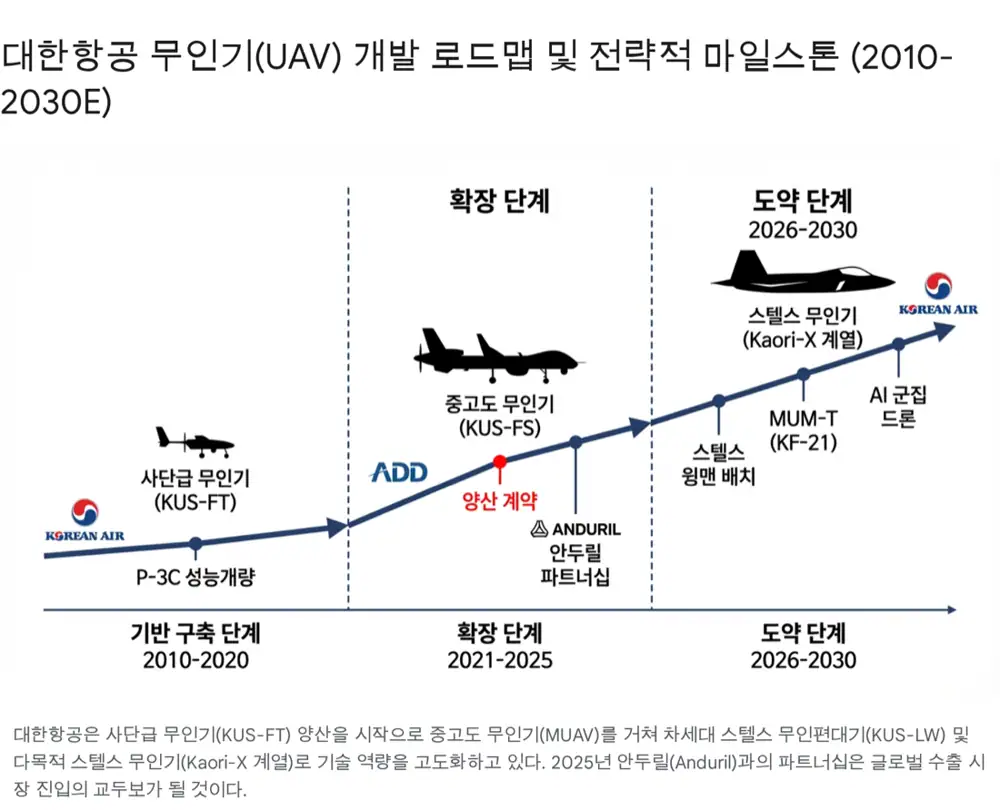

1. Why this is a defense platform, not just an airline

Official fact: The post states that Korean Air’s aerospace division has expanded since 1976 from 500MD helicopters and F-5 production into military MRO, civil aircraft structures, and UAV systems.

Stable cash flow

The post cites maintenance and upgrade experience on F-4, F-15, F-16, A-10, P-3C, and CH-47 platforms.

Global supply chain

Key items include the B787 aft fuselage, raked wing tip, flap support fairing, and A350 cargo door and sharklet.

Growth driver

The source highlights the late-2023 KRW 471.7 billion MUAV KUS-FS mass-production contract with deliveries through 2028.

2. Stealth UAVs and manned-unmanned teaming

Korean Air is described as the preferred bidder for the 2025 ADD low-observable unmanned wingman development project. The source interprets this as a core MUM-T platform linked to manned fighters such as the KF-21. The February 2025 rollout of the first low-observable UAV flight prototype and the Seoul ADEX 2025 UAV showcase are treated as milestones.

3. Valuation scenario

Official fact: The DCF assumptions in the source use 8.0% annual growth for 2026-2027, 4.0% for 2028-2030, OPM rising from 9-10% to 11.0%, WACC of 6.8%, risk-free rate of 3.34%, beta of 0.83, market risk premium of 6.0%, after-tax cost of debt of about 4.5%, target capital structure of 40% equity and 60% debt, and terminal growth of 1.5%.

| Item | Source figure |

|---|---|

| Sum of PV | KRW 9,591bn |

| Terminal Value PV | KRW 37,230bn |

| EV | KRW 46,821bn |

| Net Debt | About KRW 13,500bn |

| Equity Value | KRW 33,321bn |

| Shares outstanding | About 368,220,610 shares |

| Target Price | About KRW 36,000 |

| Reference Price | About KRW 21,000-23,000 |

| Upside | More than +56% |

4. Risks

- PMI costs after the Asiana merger, including labor, mileage, and IT integration.

- Oil price spikes, FX volatility, foreign-currency debt valuation losses, and aircraft acquisition costs.

- Schedule delays in national projects such as stealth UAVs and financing limits for large defense exports.

Sources

- 원문 블로그

- 프라임경제 대한항공-안두릴

- 대한항공 뉴스룸 안두릴 협력

- KB의 생각 항공우주 흑자

- Korean Air Aerospace history

- Defense News reconnaissance drone

- 에어뉴스 스텔스 무인편대기

- 대한항공 ADEX 2025 무인기 3종

- 뉴스와이어 ADEX 2025

- Korea Times aerospace portfolio

- AviTrader Boeing order

- Boeing 103 jets

- IBA aircraft backlog

- 연합인포맥스 항공우주 흑자

- Trading Economics Korea 10Y

- StockInvest 003490.KS

- 대한항공 003490 AWS PDF