DEEP RESEARCH · SHIPBUILDING AND LNG

The Opening of the North American LNG Supercycle and Korea's Shipbuilding Value Chain

What HD Hyundai Heavy Industries' January 6, 2026 LNGC order signals for shipbuilders and equipment suppliers

0. Bottom line first

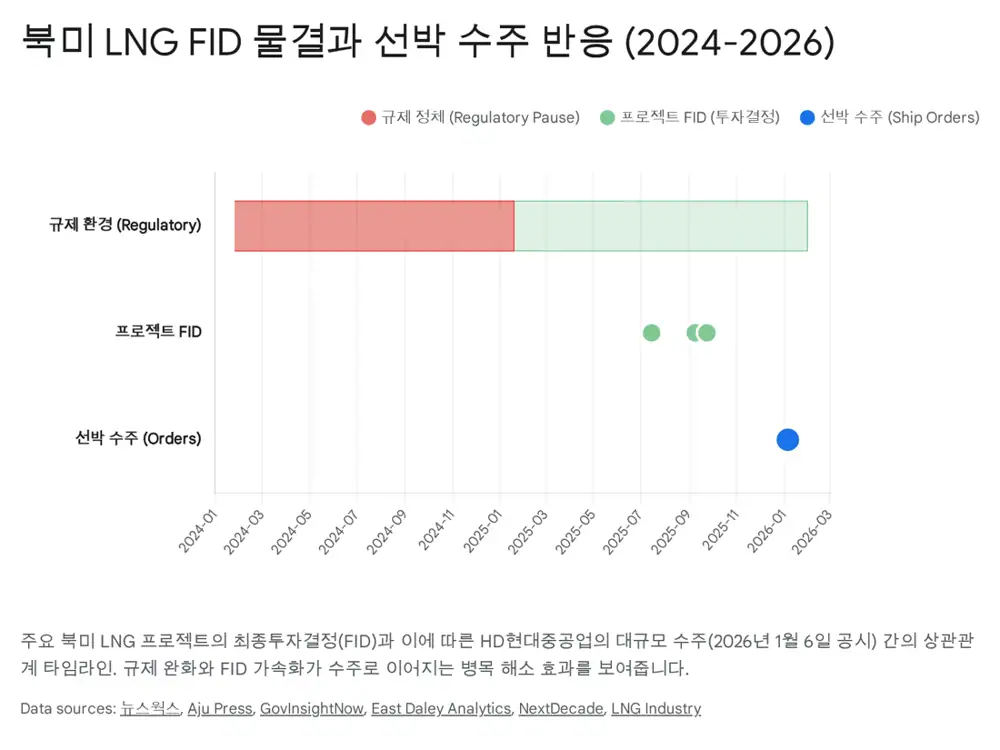

HD Hyundai Heavy Industries' January 6, 2026 order for four LNG carriers from a North American shipowner is not just another contract. I read it as a signal that the second North American LNG wave has moved from expectations into earnings reality. The bottleneck and pricing power now extend across shipyards, engines, insulation, fittings, and valves.

1. The contract confirms a new normal

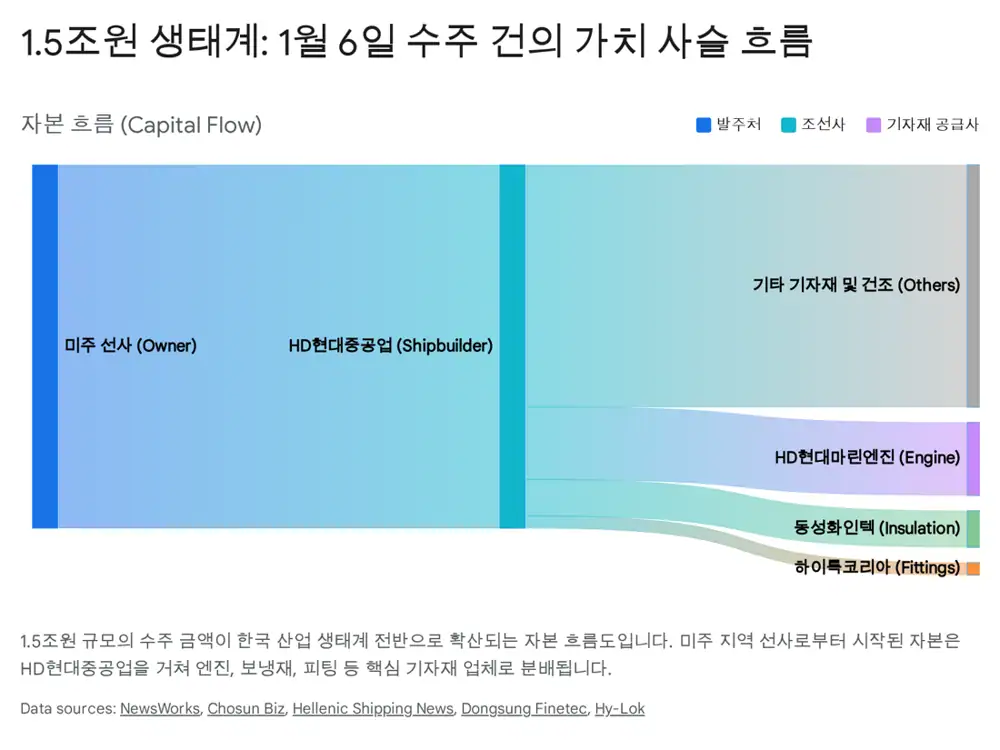

Official fact: The source states that on January 6, 2026, HD Hyundai Heavy Industries under HD KSOE won four ultra-large LNG carriers from a North American shipowner for KRW 1.4993 trillion, or about USD 1.1 billion.

- The implied value per ship is about KRW 375 billion, or about USD 275 million assuming KRW 1,360 per dollar.

- The vessels are described as 200,000 cbm class ships, 294.8m long, 48.9m wide, and 26.7m high.

- Delivery is scheduled by the first half of 2029, implying tight 2027-2028 delivery slots.

- After the disclosure, HD Hyundai Heavy Industries closed up 7.21% at KRW 550,000; HD Hyundai Marine Engine rose 7.98%, and Hanwha Engine rose 3.58%.

Interpretation: A high-priced 2029-delivery LNGC order in an already tight dock market suggests pricing power has shifted toward the shipbuilders.

2. North American LNG FIDs and likely ordering pressure

The disclosure only identifies the buyer as a North American shipowner. The source narrows the likely background to Venture Global's CP2 LNG project and Sempra Infrastructure's Port Arthur LNG Phase 2. In either case, the key point is that this looks like demand backed by committed volumes, not speculative ordering.

3. Value chain: more flood effect than trickle-down

Selective ordering

When docks are already full, the strategy shifts from volume to choosing higher-margin projects.

HD Hyundai Marine Engine and Hanwha Engine

High-value LNGC orders directly support utilization and profitability for engine makers.

Dongsung Finetec and Hankuk Carbon

LNG cargo-tank insulation for minus 163 degrees Celsius is tight, and larger 200k vessels require more insulation per ship than 174k vessels.

Sung Kwang Bend, TK, and Hy-Lok

This is a double-dip setup: North American onshore liquefaction plants and Korean offshore vessel construction require components at the same time.

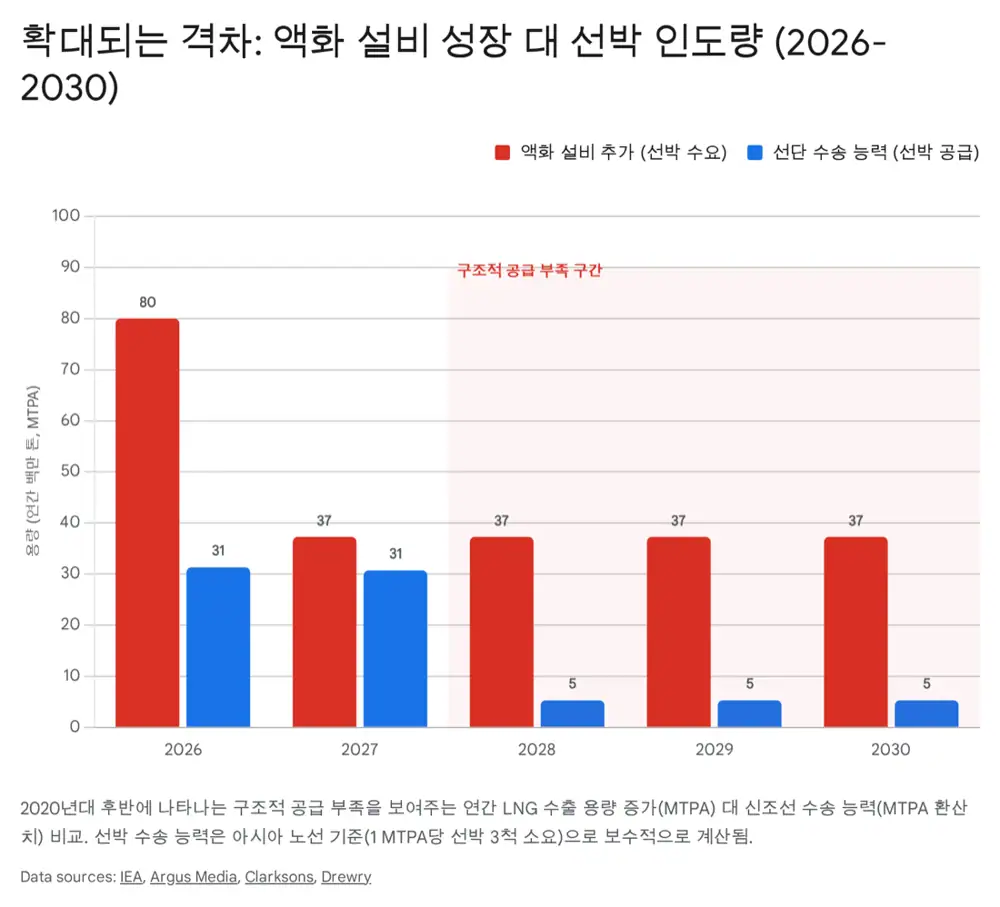

4. 2026-2027 order scenario

| Period | Estimated additional orders | Basis |

|---|---|---|

| 1H 2026 | 12-16 ships | Remaining CP2 LNG volume and Port Arthur Phase 2 procurement |

| 2H 2026 | 10-14 ships | Lake Charles targeting a 1Q 2026 FID and possible initial-delivery orders |

| 2027 | 40+ ships for the year | Rio Grande additional trains, Delfin LNG, Commonwealth LNG, and a second wave of projects |

The source estimates roughly 40-50 ships from North American projects in 2026-2027. At USD 275 million per ship, that implies a market of about USD 11.0-13.7 billion, or roughly KRW 15-18 trillion.

5. Risks and strategy

- The core bottleneck is moving from shipyard docks to suppliers such as insulation, engines, fittings, and valves.

- Equipment suppliers need to assess both CAPA expansion and pricing power.

- Investors should look not only at shipbuilder top-line growth but also at bottom-line leverage in insulation and fitting suppliers.

Sources

- Original blog

- Newsworks HD Hyundai LNG carrier order

- AJU PRESS Hot Stock

- Youthdaily HD KSOE LNG carrier order

- East Daley CP2 FID

- Venture Global CP2 FID

- LNG Industry Sempra Port Arthur Phase 2

- KPENews HD KSOE first order of the year

- Chosunbiz Dongsung Finetec stocks soar

- Dongsung Finetec KRW 1.1 trillion orders

- Korea Times US LNG MASGA projects

- Hellenic Shipping News US LNG MASGA projects

- Sempra Infrastructure Port Arthur LNG Phase 2

- Fedorchak LNG restrictions

- Majority Leader Floor Lookout

- Offshore Energy US LNG export projects on hold

- Insurance Journal Lake Charles decision

- Daily Money Guide US LNG exports

- Clarksons LNG Shipping

- Drewry LNGCs by 2030

- Argus LNG carrier orderbook

- Offshore Energy HD Hyundai HMM

- Design Development Today HD Hyundai

- KED Global Samsung Heavy FLNG

- RAND shipbuilding cooperation

- Marine Link HMM $2.8B order

- Chosunbiz HiMSEN engines

- Korea Times engine competition

- Chosunbiz Dongsung Finetec Hankuk Carbon

- Chosunbiz Korean shipbuilders backlog

- Hy-Lok LNG industries

- Hy-Lok USA distributors