DEEP RESEARCH · NEXTEER AUTOMOTIVE

2025 Nexteer Automotive Comprehensive Analysis

A review of financial performance, bookings, and the technology roadmap as Nexteer shifts from steering supplier to intelligent motion-control company

0. Bottom line first

My read is that Nexteer's key change is a shift in identity from traditional Tier-1 steering supplier to intuitive motion-control technology company. First-half 2025 results already show this transition in the numbers, while third-quarter bookings show the growth axis moving toward APAC and electrification.

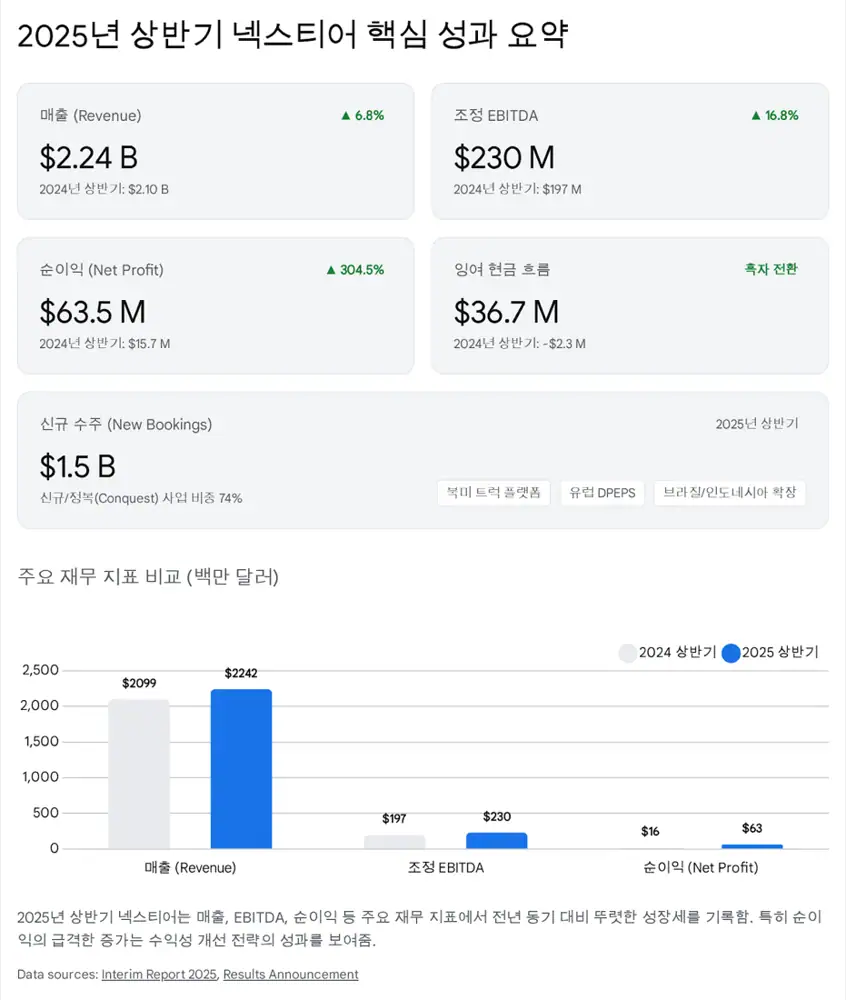

Official fact: First-half 2025 revenue was $2.242 billion, up 6.8% year over year, and adjusted EBITDA was $230.4 million, up 16.8%. Net profit attributable to shareholders was $63.5 million, up 304.5% from $15.7 million in the prior-year period.

Interpretation: This is not just a recovery in auto production. The story combines growth above market production, cost-structure improvement, APAC customer expansion, and a Motion-by-Wire technology roadmap.

1. First-half 2025 financial performance

Nexteer generated first-half 2025 revenue of $2.242 billion, up 6.8% year over year. Since global OEM production rose only 3.1% over the same period, Nexteer achieved roughly 370bp of growth-over-market. Excluding FX and pricing pass-through from lower raw-material costs, adjusted revenue growth was 7.6%, or 450bp above the market. Source links include Nexteer official first-half results and PR Newswire release.

| Metric | H1 2025 | Year-over-year/comparison | Read-through |

|---|---|---|---|

| Revenue | $2.242 billion | +6.8% | Record first-half result |

| Global OEM production | +3.1% | Nexteer outperformed by about 370bp | Growth over market |

| Adjusted revenue growth | +7.6% | 450bp above market | Still strong after FX and raw-material effects |

| Adjusted EBITDA | $230.4 million | +16.8% | Operating leverage visible |

| Net profit attributable to shareholders | $63.5 million | Up 304.5% from $15.7 million | Mix of base effect and cost improvement |

Three items drove profitability. First, higher revenue created operating leverage, with APAC volume improving utilization. Second, manufacturing efficiency and material-cost savings lifted gross margin from 10.0% in H1 2024 to 11.5% in H1 2025, a 150bp improvement. Third, impairment from a cancelled customer program fell from $37.7 million in H1 2024 to $1.6 million in 2025, creating a strong base effect in net income.

Official fact: Free cash flow turned from a $6.6 million outflow in H1 2024 to a $36.7 million inflow in H1 2025. Cash and equivalents as of June 30, 2025 were $459.2 million, about $37 million above year-end 2024, and the gearing ratio declined to 2.3% from 2.4%.

Interpretation: Low leverage is defensive in a high-rate environment and also preserves optionality for alliances, investment, or M&A in robotics and software. The key question is how this balance-sheet flexibility is used to support the technology transition.

2. Regional performance: APAC becomes the growth axis

Regional revenue shows Nexteer's center of growth moving from North America toward Asia Pacific, especially China.

$686.5 million

Revenue grew 15.5% year over year. Adjusted growth excluding FX was 16.7%, more than double the region's 8% OEM production growth.

$1.1383 billion

Revenue grew only 1.7%. That was resilient versus a 4.2% decline in North American OEM production, but a $2.7 million pricing reduction from lower raw materials and supplier issues limited growth.

$400.85 million

Revenue rose 9.4%. Despite European production declining 3.7%, South America recovered 8.9% and new European program launches supported growth.

The important point is that APAC growth is not just a regional mix shift; it comes with a customer mix shift. Chinese EV and EREV makers, premium EV brands, and export models are appearing together in the launch list, broadening the adoption of Nexteer's technology.

3. Third-quarter bookings and program launches

In its Q3 2025 business update, Nexteer reported $2.2 billion of cumulative new bookings from the start of the year through quarter-end. This consisted of $1.5 billion in the first half and $700 million in Q3 alone.

| YTD Q3 bookings mix | Share | Meaning |

|---|---|---|

| Product mix: EPS | 69% | Electric power steering remains the core growth engine |

| Product mix: driveline | 16% | Secondary motion-control axis |

| Product mix: CIS | 15% | Column and intermediate-shaft foundation remains |

| New/conquest business | 33% | New customer wins continue |

| Incumbent business | 67% | Existing relationships remain solid |

| EV-related programs | 50% | Clear electrification exposure |

| Region: APAC | 49% | Largest booking region |

| Region: North America/EMEASA | 30% / 20% | Diversification remains, but future growth is more APAC-weighted |

Fourteen new programs launched in Q3, and all were in APAC. The source reads this as evidence that near-term growth and engineering resources are concentrated in Asia, especially China's rapidly evolving EV ecosystem.

- Li Auto: REPS for L6 and L8, steering column for L7.

- Zeekr: REPS and halfshaft for 9X.

- BYD: CEPS for export Seal model.

- Geely: REPS for Galaxy V900.

- SGMW: CEPS for Xingguang 730/560.

- Ford: REPS and column for Bronco.

Eight of the fourteen programs were EV-only models, confirming the portfolio's shift toward electrification. At the same time, programs such as Ford Bronco keep exposure to internal-combustion and off-road categories, preserving flexibility during an EV demand chasm.

4. Six strategies for profitable growth

Nexteer's management operates around six principles for profitable growth. The source argues that 2025 results and bookings show these principles being executed in the field.

Expand and diversify revenue

Chinese OEM bookings represented 39% of H1 2025 bookings, about $600 million. Indonesia and Brazil are also framed as emerging-market diversification.

Strengthen technology leadership

The first RWS booking in Europe and first DPEPS launch in China show the company trying to set technology standards.

Align with megatrends

EV-related bookings were 50% of the total, while high-output EPS and software-defined chassis solutions align with electrification, connectivity, and autonomy.

Optimize cost structure

Workforce rotation at Mexico and APAC technical centers and supply-chain digitalization supported the free-cash-flow turnaround.

Selective alliances

CNXMotion with Continental and the Tactile Mobility investment target integrated steering/braking control and software capability. Source: Tactile Mobility investment release.

Target China and emerging markets

Changshu, Liuzhou, and Suzhou projects are investments in local R&D and manufacturing response speed.

5. Technology roadmap: Motion-by-Wire and robotics

Nexteer's technology strategy can be summarized as a move from mechanical linkage to digital control, or Motion-by-Wire. If completed, steering, braking, rear-wheel steering, and software control can converge into one chassis-control platform.

Official fact: The source highlights the DD-HWA, or Direct Drive Hand Wheel Actuator, announced in October 2025. It connects a high-performance motor directly to the steering wheel to deliver refined steering feel without a physical linkage, supports both 12V and 48V architectures, and uses multi-channel angle sensing for redundancy and safety. Source: DD-HWA announcement.

| Technology | Role | Strategic meaning in the source |

|---|---|---|

| Steer-by-Wire | Removes the physical steering column and controls steering electrically | Essential for autonomy; more bookings expected in Q4 2025 |

| DD-HWA | Direct motor connection and steering-feel feedback | Premium feel, High-Mount/Low-Mount flexibility, retractable-wheel possibility |

| RWS | Reduces turning radius and improves high-speed stability for long-wheelbase EVs | First European RWS booking in H1 2025 |

| EMB | Removes hydraulic lines and uses electric motor braking | Extends toward integrated steering and braking control |

| MotionIQ | Chassis control, development acceleration, and vehicle health monitoring | Software suite for the SDV trend. Source: Nexteer Software |

Robotics and Physical AI are still more optional than proven, but the source cites Morgan Stanley's humanoid value-chain analysis and hiring posts to suggest Nexteer is interested in humanoid robot actuators. EPS core capabilities such as precision motor control, reduction gears, and sensors overlap with robot joint actuators. Links: Morgan Stanley report, humanoid robot actuator job post, and ZipRecruiter job link.

6. APAC expansion strategy and 2025 guidance

Nexteer's APAC strategy is not just factory expansion. It localizes R&D and supply chains to respond to China Speed.

- Changshu plant: opened in January 2025 as a manufacturing and testing hub for Chinese COEM demand and EPS/driveline capacity.

- Liuzhou smart plant: groundbreaking in July 2025, with operations targeted for H1 2026. The co-location model with key suppliers is designed to improve logistics efficiency and response speed. Source: Liuzhou groundbreaking release.

- Suzhou smart manufacturing project: MOU in September 2025 and groundbreaking in November. It combines APAC headquarters, R&D center, and smart manufacturing hub. Source: Suzhou project release.

Management reaffirmed a 2025 full-year new-booking target of about $5.0 billion. With $2.2 billion booked through Q3, the company needs about $2.8 billion in Q4. It points to a strong Q4 pipeline, especially large Steer-by-Wire bookings.

7. Risks and final read

There are three main risks. First, tariffs and trade policy from U.S.-China tensions and protectionism. The company responds through USMCA-compliant supply-chain adjustments, Mexico technical-center expansion, and dual sourcing. Related link: Assembly Magazine article. Second, supply-chain instability such as North American supplier issues. Third, EV demand slowing. Nexteer partially offsets that risk with high-output EPS bookings for PHEV/EREV platforms.

Interpretation: Near term, the critical test is whether Nexteer can close the roughly $2.8 billion Q4 booking gap. Long term, the question is whether Motion-by-Wire and robotics actuator optionality can shift the company's multiple from a component supplier toward an integrated actuator-solutions provider.

Sources

- 네이버 블로그 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224134323286

- Nexteer Reports Strong First-Half 2025 Results - PR Newswire: https://www.prnewswire.com/in/news-releases/nexteer-reports-strong-first-half-2025-results-302528757.html

- Nexteer Reports Strong First-Half 2025 Results: https://www.nexteer.com/release/nexteer-reports-strong-first-half-2025-results/

- Nexteer Invests in Tactile Mobility: https://www.nexteer.com/blog/nexteer-invests-in-tactile-mobility-to-support-software-offerings-next-level-steering-feel/

- ANNUAL REPORT 2017 - Nexteer: https://www.nexteer.com/wp-content/uploads/EW01316-1-1-1.pdf

- Nexteer Signs Agreement for New Smart Manufacturing Project in Suzhou, China: https://www.nexteer.com/release/nexteer-signs-agreement-for-new-smart-manufacturing-project-in-suzhou-china/

- Nexteer Announces Direct Drive Hand Wheel Actuator: https://www.prnewswire.com/news-releases/nexteer-announces-direct-drive-hand-wheel-actuator-latest-in-motion-by-wire-innovation-302576068.html

- Software - Nexteer: https://www.nexteer.com/software/

- Mapping the Humanoid Robot Value Chain - Morgan Stanley: https://advisor.morganstanley.com/john.howard/documents/field/j/jo/john-howard/The_Humanoid_100_-_Mapping_the_Humanoid_Robot_Value_Chain.pdf

- Nexteer Automotive Project Manager - Humanoid Robot Actuators: https://jobs.weekday.works/nexteer-automotive-project-manager--humanoid-robot-actuators

- AI Project Manager Jobs in Bloomfield Hills, MI: https://www.ziprecruiter.com/Jobs/Ai-Project-Manager/-in-Bloomfield-Hills,MI

- Nexteer Breaks Ground on New Manufacturing Facility in Liuzhou, China: https://www.nexteer.com/release/nexteer-breaks-ground-on-new-manufacturing-facility-in-liuzhou-china/

- News Releases - Nexteer: https://www.nexteer.com/news-releases/

- Nexteer to Expand Mexico Operations - Assembly Magazine: https://www.assemblymag.com/articles/98428-nexteer-to-expand-mexico-operations