DEEP RESEARCH · CELLTRION/CDMO

Celltrion Deep Dive: From Biosimilar Pioneer to Global Biopharma and CDMO Platform

A structural transition report linking merger synergies, Zymfentra, the Branchburg U.S. site, and CDMO expansion

0. Bottom line first

The source conclusion is that Celltrion is moving from biosimilar fast follower to a hybrid biopharma company with new drugs, global direct sales, and CDMO. The December 2023 merger with Celltrion Healthcare started the COGS normalization story, and Q3 2025 operating margin of about 29.2% plus record quarterly revenue show it in the numbers.

Official fact: The source cites Q3 2025 revenue of KRW 1.029T, operating profit of KRW 301.4B, operating margin of about 29.2%, COGS ratio of 39%, and 2025 annual guidance of KRW 4.1163T revenue and KRW 1.1655T operating profit.

Interpretation: The key is margin recovery after high-cost inventory depletion, Zymfentra’s U.S. new-drug positioning, and the immediate CDMO credibility gained from acquiring Eli Lilly’s Branchburg facility.

1. Corporate evolution and merger effects

Celltrion was founded in 1991 and pivoted into biopharmaceuticals in 2002. It developed Remsima, the world’s first antibody biosimilar, and received EMA and FDA approvals. Truxima and Herzuma expanded its first-mover position. As of the September 30, 2025 quarterly report, Celltrion is framed as an Incheon Songdo-based global biotechnology company led by CEO Seo Jin-seok.

The December 28, 2023 merger between Celltrion and Celltrion Healthcare is described as a turning point that reduced intercompany transactions, inventory-accounting opacity, and decision-making inefficiency. Removing transfer pricing created final-price flexibility, while integrated development, production, and sales improved responsiveness to market demand.

| Post-merger change | Source detail | Meaning |

|---|---|---|

| COGS ratio | From the 60% range at end-2023 to 39% in Q3 2025 | High-cost inventory depletion and direct-sales benefits |

| Time to market | Integrated development, production, and sales | Product launch and marketing integration |

| Pricing power | Transfer-price structure removed | Better U.S. and European tender flexibility |

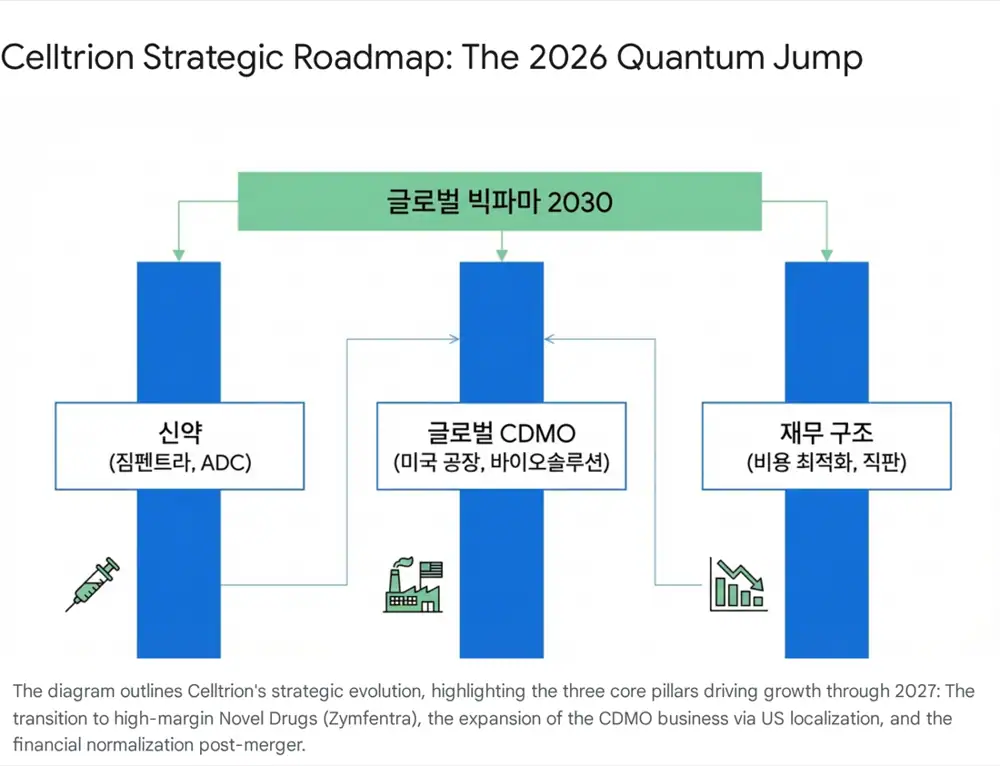

2. Three growth engines: biosimilars, new drugs, CDMO

Biosimilars

Remsima, Truxima, and Herzuma are joined by Yuflyma, Vegzelma, Steqeyma, Omlyclo, and Eylea biosimilar Aydenselt, with a goal of 22 biosimilars by 2030.

Zymfentra

The IV-to-SC infliximab product received FDA approval as a new drug, with higher pricing than biosimilars and patent protection until 2040.

CDMO

Celltrion BioSolutions and the U.S. facility acquisition support a hybrid CDMO model combining internal base-load with external contracts.

The BIOSECURE Act is presented as a U.S. effort to exclude Chinese biotech firms from federal grants and procurement. That pushes global pharma toward China-free supply chains and raises demand for trusted CDMO partners. Acquiring Eli Lilly’s Branchburg facility in New Jersey gives Celltrion U.S.-based manufacturing and an existing cGMP history.

3. Technology and next-generation pipeline

Celltrion’s technology has moved beyond “making copies” toward yield improvement and new-drug problem solving. The Titer Improvement project uses high-productivity cell-line selection, fed-batch process optimization, and purification-loss reduction to raise antibody output. The source links this to COGS improvement from 63% to 39%.

- Zymfentra: The source highlights formulation technology that solves viscosity and aggregation challenges in high-concentration antibody SC products.

- ADC: cMET ADC CT-P70 and Nectin-4 ADC CT-P71 target non-small cell lung cancer and bladder cancer, with PinotBio camptothecin payloads as a differentiator.

- Open innovation: Iksuda Therapeutics investment, PinotBio linker-payload collaboration, WuXi XDC cooperation, and Kaigene KG006 and KG002 licensing are cited.

- Platform expansion: Bispecific antibodies and microbiome therapies broaden the pipeline beyond biosimilars.

4. Quality control and global production capacity

Quality is existential in biologics. Celltrion received FDA warning letters in 2017-2018 related to aseptic processing, vial breakage procedures, and environmental monitoring. The source says Celltrion responded with outside consulting, quality staffing, and real-time process-data monitoring, then received VAI status on reinspection and won U.S. approvals for Truxima and Herzuma.

In a July 2024 FDA inspection, Form 483 was issued, but the source characterizes the eight observations as manageable and correctible. It says no severe aseptic-processing or data-integrity issue was found and production or approval processes were not disrupted.

| Site | Capacity/investment | Role |

|---|---|---|

| Songdo campus | Plant 1 100,000L, Plant 2 90,000L, Plant 3 60,000L, total 250,000L | Flexible multi-product biosimilar production |

| Branchburg | Acquired for about USD 330M, or KRW 460B; current capacity about 66,000L | U.S. cGMP manufacturing site |

| Branchburg expansion | Additional KRW 700B investment, expansion to 132,000L | Two phases, each adding three 11,000L bioreactors |

| Korean expansion | About KRW 4T blueprint for Songdo, Yesan, and Ochang facilities including finished-product and prefilled-syringe lines | Long-term scale economy |

5. CDMO model and financial normalization

Celltrion’s CDMO strategy differs from a pure-play model like Samsung Biologics. It uses internal product demand as base-load and then fills spare capacity with external orders. The Branchburg acquisition came with a KRW 678.7B manufacturing contract with Eli Lilly, creating immediate utilization and revenue visibility.

| Metric | Source figure | Interpretation |

|---|---|---|

| Q3 2025 revenue | KRW 1.029T, up 16.3% YoY | Record quarterly revenue |

| Q3 2025 operating profit | KRW 301.4B, up 44.9% YoY | Operating margin about 29.2% |

| COGS ratio | 39% in Q3 2025, 36.1% expected in Q4 | High-cost inventory depletion and low-cost product sales |

| 2025 guidance | Revenue KRW 4.1163T, operating profit KRW 1.1655T | Revenue +15.7%, operating profit +136.9% YoY |

| 2026 goal/consensus | Revenue KRW 5.3T | Zymfentra and CDMO acceleration |

| Balance sheet | Assets about KRW 21T, debt about KRW 4.2T, cash about KRW 810B | Base capacity to fund planned CAPEX |

6. Investment view and risks

The source cites Celltrion trading around 27x 2026E EV/EBITDA, a slight discount to Samsung Biologics around 30x and Lonza. If Celltrion is evolving from a biosimilar company into a broader new-drug and CDMO platform, the source argues that discount is excessive.

- Buy reason 1: High-cost inventory after the merger has been resolved and margins are normalizing.

- Buy reason 2: Zymfentra’s U.S. market adoption can drive structural revenue growth.

- Buy reason 3: The U.S. plant acquisition creates immediate CDMO cash flow and possible BIOSECURE Act benefit.

- Risk: The failed August 2024 Celltrion Pharm merger vote leaves governance debate alive.

- Risk: Private issues related to Chairman Seo Jung-jin are cited, though the source sees limited enterprise-value impact because professional management and board functions are strengthening.

My read is that Celltrion is past the hardest part of the merger digestion and now must prove earnings, new drugs, and CDMO together. It has both fundamentals and momentum, but CAPEX scale, quality execution, and U.S. prescription uptake remain the variables to track.

Sources

- Naver Blog source: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224133544322

- Celltrion posts record Q3 profit - The Korea Herald: https://www.koreaherald.com/article/10598105

- Celltrion eyes record high sales in 2025 - KED Global: https://www.kedglobal.com/earnings/newsView/ked202507210007

- Celltrion completes acquisition of US Eli Lilly plant - The Korea Herald: https://www.koreaherald.com/article/10647910

- Celltrion completes acquisition of Eli Lilly manufacturing facility - KBR: https://www.koreabiomed.com/news/articleView.html?idxno=30155

- Celltrion European Union press release: https://www.celltrion.com/en-us/company/media-center/press-release/3620

- Celltrion to break ground on CDMO plant in 2025 - KED Global: https://www.kedglobal.com/bio-pharma/newsView/ked202411280003

- Celltrion growth strategy and prospects - Porter Five Forces: https://portersfiveforce.com/blogs/growth-strategy/celltrion

- Celltrion CDMO expansion strategy - KBR: https://www.koreabiomed.com/news/articleView.html?idxno=25850

- BIOSECURE Act note - Latham & Watkins: https://www.lw.com/en/insights/biosecure-act-becomes-law-limiting-grants-with-biotechnology-companies-of-concern

- Celltrion US plant upgrade - Fierce Pharma: https://www.fiercepharma.com/manufacturing/celltrion-jacks-us-investment-plan-478m-outlay-upgrade-former-lilly-plant

- Celltrion ADC ambition with Pinot tech deal - BioProcess International: https://www.bioprocessintl.com/deal-making/celltrion-bulks-out-adc-ambition-with-pinot-tech-deal

- Celltrion Kaigene candidate technology-transfer analysis - Google Drive: https://drive.google.com/open?id=1c71Puq_4Cbtm9_iB2wpmbi3MZ3N0948tTRcqKxSp_i0

- Celltrion Q1 revenue - KBR: https://www.koreabiomed.com/news/articleView.html?idxno=27510

- Cell culture processes for monoclonal antibody production - NIH: https://pmc.ncbi.nlm.nih.gov/articles/PMC2958569/

- Cell culture titer and protein quality - Cytiva: https://www.cytivalifesciences.com/en/us/insights/titer-and-protein-quality

- Celltrion strategic vision at J.P. Morgan Healthcare Conference - PR Newswire: https://www.prnewswire.com/news-releases/celltrion-unveils-strategic-vision-for-advancing-its-innovative-drug-pipeline-at-the-43rd-annual-jp-morgan-healthcare-conference-302351202.html

- Celltrion FDA 483 observations - BioProcess International: https://www.bioprocessintl.com/regulations/celltrion-receives-fda-483-with-8-manageable-and-correctible-observations

- How a 483 turned into a Warning Letter for Celltrion - ECA Academy: https://www.gmp-compliance.org/gmp-news/how-a-483-turned-into-a-warning-letter-for-celltrion-in-south-korea

- FDA Compliance Record 483 Celltrion 2018: https://www.fda.gov/files/drugs/published/Compliance-Record-483--Celltrion-Inc.--July-17-17--2018.pdf

- FDA Inspection Reports for Celltrion Pharm - ProPublica: https://projects.propublica.org/rx-inspector/facilities/3012279978/

- Celltrion Healthcare Ireland: https://www.celltrionhealthcare.ie/

- Celltrion story page: https://www.celltrion.com/en-us/company/media-center/stories/3934

- Celltrion acquires Eli Lilly facility with KRW 680B CMO contract - Business Korea: https://www.businesskorea.co.kr/news/articleView.html?idxno=260120

- Celltrion CAPEX - Finbox: https://finbox.com/KOSE:A068270/explorer/capex

- Celltrion US plant tariff-risk upgrade - The Korea Herald: https://www.koreaherald.com/article/10619386

- Celltrion oral weight-loss market - KED Global: https://www.kedglobal.com/bio-pharma/newsView/ked202511190008

- Celltrion expected to pass KRW 4T sales and KRW 1T OP - MK: https://www.mk.co.kr/en/it/11919938

- Celltrion forecasts 137% profit growth - The Korea Times: https://www.koreatimes.co.kr/business/companies/20251231/celltrion-forecasts-137-year-on-year-growth-in-2025-profits

- Celltrion Mirae Asset report PDF: https://securities.miraeasset.com/bbs/download/2139727.pdf?attachmentId=2139727

- Korea Investment raises Celltrion target - ChosunBiz: https://biz.chosun.com/en/en-finance/2026/01/02/TSEP4EHPINDDNB3XT6ZY47X7MI/

- Celltrion Bondweb report: https://www.bondweb.co.kr/_research/downloadPage.asp?number=858149&gn=1

- Celltrion merger dashed - The Korea Times: https://www.koreatimes.co.kr/business/companies/20240816/celltrions-merger-with-unit-dashed-amid-shareholder-opposition