DEEP RESEARCH · CELLTRION

2026 K-Bio Power Map: Celltrion, Samsung Biologics, and ST Pharm

Comparing biosimilars, CDMO, and RNA therapy supply chains to identify the 2026 sector leader candidate

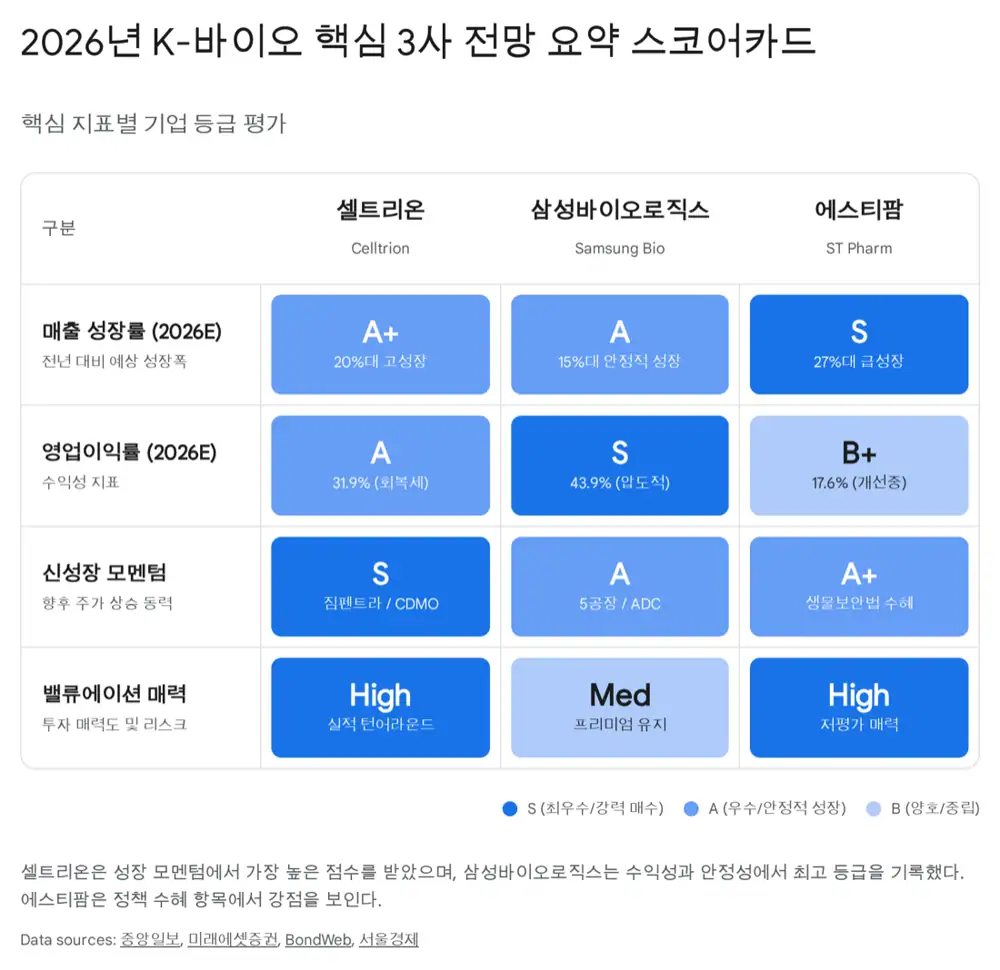

0. Bottom line first

In my view, Celltrion has the strongest 2026 combination of growth and stock momentum. Samsung Biologics remains the constant for stability and profitability, ST Pharm is a high-growth niche champion, and Celltrion is the re-rating candidate where Zymfentra and U.S. CDMO expansion can work at the same time.

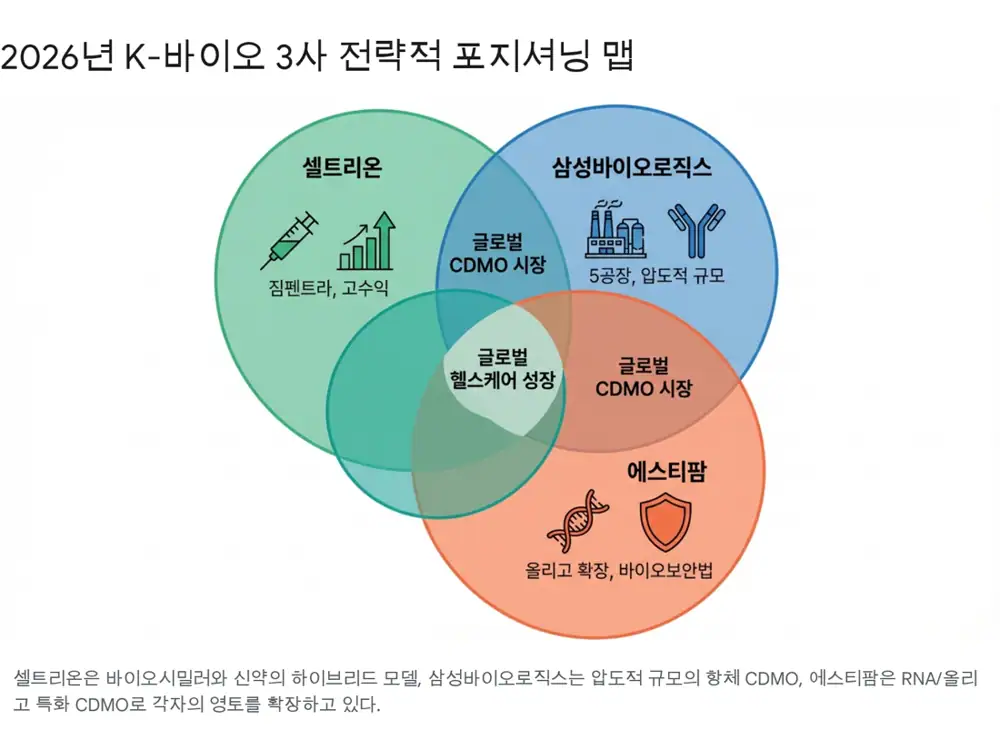

1. Industry backdrop and three-company map

Official fact: The source frames Korea's pharma and biotech industry as moving from volume expansion toward qualitative upgrading and a central role in global supply chains from 2025 onward.

Interpretation: Rate-cut expectations, the U.S. Biosecure Act, and blockbuster patent expirations together create a re-rating setup for both biosimilars and CDMO.

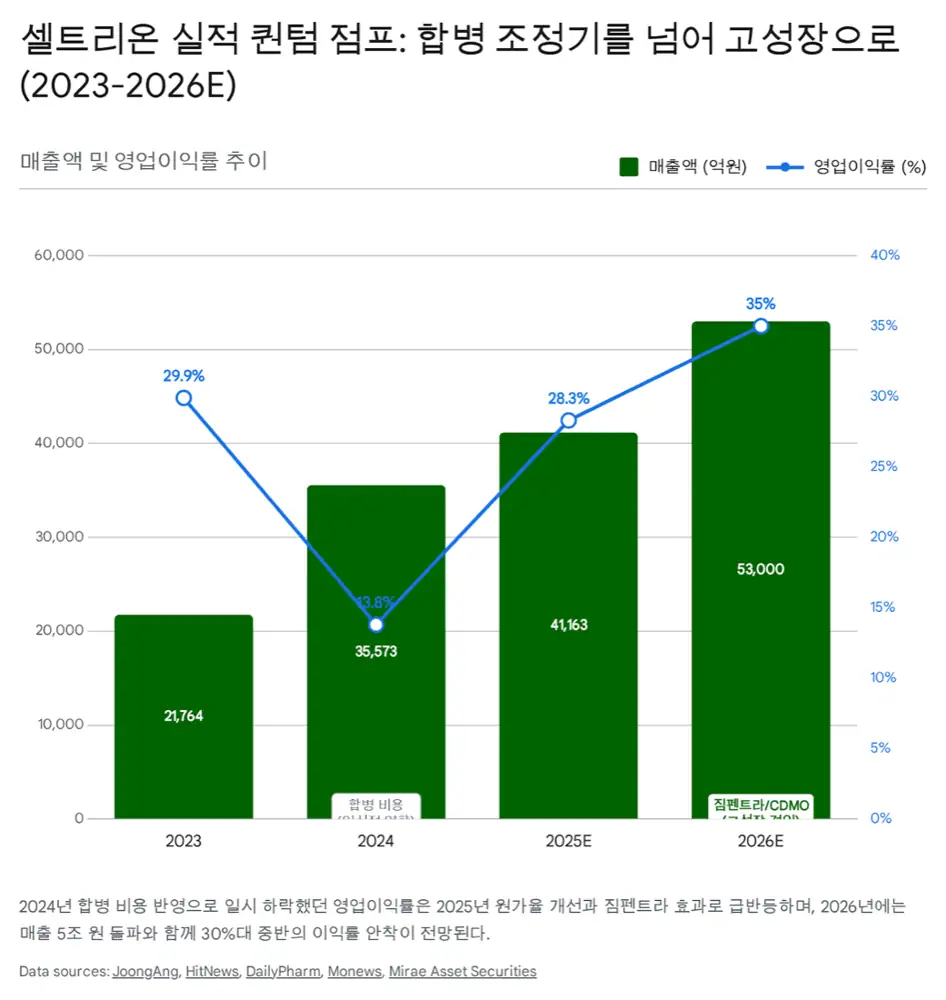

2. Celltrion: post-merger earnings recovery

Official fact: The source cites 3Q 2025 consolidated revenue of KRW 1.026 trillion (+16.3% YoY) and operating profit of KRW 301.0 billion (+44.9% YoY). The 4Q outlook is revenue of KRW 1.2839 trillion (+20.7% YoY) and operating profit of KRW 472.2 billion (+140.4% YoY).

- Annual revenue of KRW 4.1163 trillion and operating profit of KRW 1.1655 trillion are cited.

- Cost of sales is described as improving from around 39% in 3Q 2025 to a preliminary 36.1% in 4Q, roughly a 3 percentage point gain.

- High-margin new products such as Zymfentra, Yuflyma, and Vegzelma are said to account for more than 60% of total revenue.

- The 2026 revenue target is KRW 5.3 trillion.

Zymfentra is described as an FDA-approved new drug, which the source treats as a pricing-power and re-rating trigger versus conventional biosimilars. The Lilly Branchburg, New Jersey plant acquisition is described as roughly KRW 460 billion, including a USD 473 million contract manufacturing agreement.

3. Comparing Samsung Biologics and ST Pharm

Scale-led CDMO

The post highlights Korea's first pharma and biotech company to exceed KRW 4 trillion in annual revenue in 2024, plus Plant 5, a 180,000-liter facility that began operation in April 2025 and should contribute revenue in 2026.

Oligo niche champion

The second oligo facility and RNA therapy demand are the core drivers. The source cites 2026 revenue of about KRW 430 billion and operating profit of KRW 76 billion.

Non-China supply chain

The Biosecure Act is framed as a possible demand-shift catalyst away from Chinese suppliers such as WuXi AppTec and WuXi STA toward Korean partners.

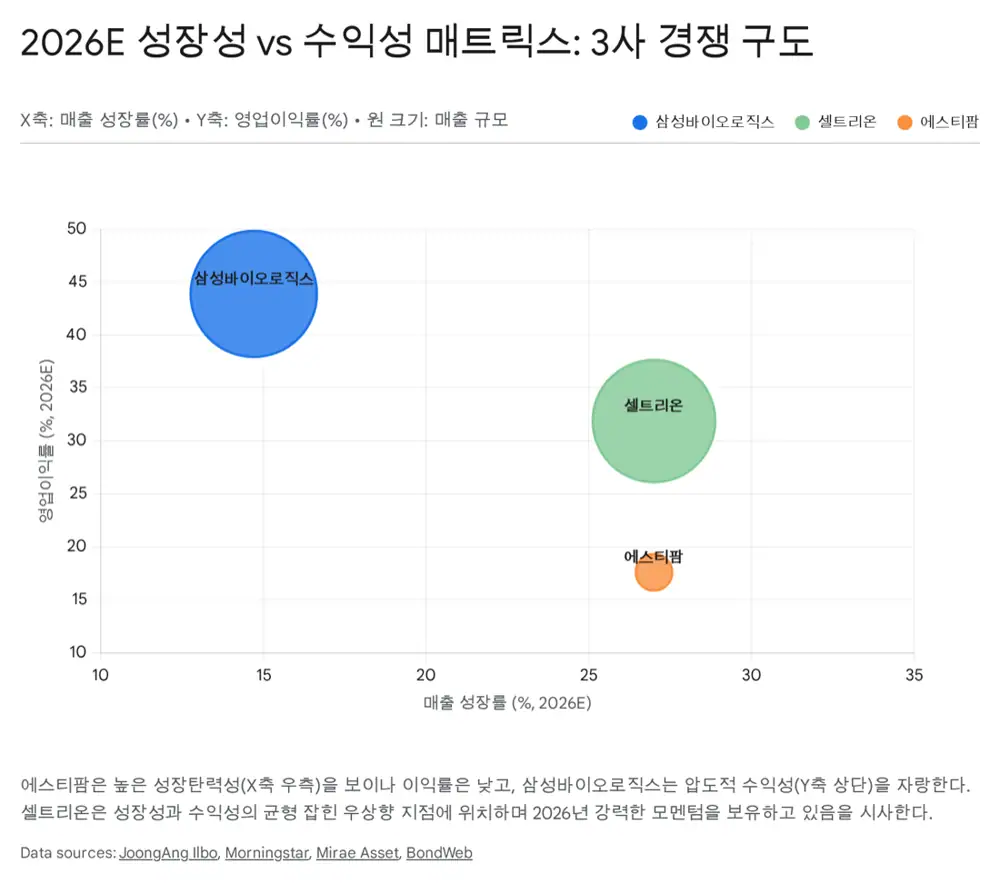

4. 2026 growth and profitability

| Company | 2026 revenue growth | OPM view | Key variable |

|---|---|---|---|

| Celltrion | About 24-27% | About 35% | Zymfentra, CDMO, merger-cost normalization |

| ST Pharm | About 27-35% | About 18-19% | Second oligo facility, RNA therapy demand |

| Samsung Biologics | About 15-20% | About 40% | Plant 5, full Plant 4 utilization, FX effect |

5. Risks and monitoring points

- FX volatility: all three exporters may face earnings pressure if the Korean won strengthens.

- U.S. policy changes: IRA-related drug-price pressure matters for Celltrion, while Biosecure Act timing and intensity matter for ST Pharm.

- Competition: price erosion in Humira, Stelara, and other biosimilar markets could cap Celltrion's margin recovery.

Sources

- 원문 블로그

- 셀트리온 Celltrion

- 셀트리온 3분기 영업이익 3천억 돌파 - 연합뉴스

- 셀트리온 매출 4조-이익 1조 보인다

- 셀트리온 올해 4조 매출 정점 예고

- Celltrion Joins 4 Trillion Won Revenue Club

- 셀트리온 4조 매출에 이익률 36%

- 셀트리온 사상 첫 연 매출 4조원 돌파

- Zymfentra efficacy

- Celltrion LIBERTY-CD post-hoc analysis - PR Newswire

- Healio: Subcutaneous infliximab effective

- PubMed Central network meta-analysis

- Morningstar: Celltrion Shares Rally

- CHOSUNBIZ: Celltrion jumps 10%

- 연합인포맥스 목표가 상향

- KFGO: Celltrion to invest up to $478 million

- Samsung Biologics 2Q 2025 results

- Samsung Biologics 2025 2Q CEO IR Newsletter

- Mirae Asset Samsung Biologics PDF

- 비즈워치 삼성바이오로직스

- 에스티팜 Bondweb

- 에스티팜 상업화 물량 확대

- 에스티팜 올리고 본격 이익 성장

- 서울경제 Why 바이오