DEEP RESEARCH · CATL/LRS

CATL: Global Energy Power Realignment and the LRS Geopolitical Hedge

How the LFP shift, North American licensing, and 90% utilization reshape the battery winner-takes-all cycle

0. Bottom line first

The source argues that the EV chasm and oversupply are not simply negative for CATL. As the market shifts from high-cost NCM toward cost-efficient and safer LFP, CATL is expanding its lead through near-90% utilization, the LRS model, and strong cash generation.

Official fact: The source identifies CATL’s top three customers as Tesla, Geely/Zeekr, and Xiaomi, and cites 38.1% global battery share for January-October 2025, Q3 2025 revenue of RMB 104.2B, net profit of RMB 18.5B, and inventory of RMB 80.2B.

Interpretation: The case is less about volume alone and more about cost spread from high utilization plus the ability to enter the U.S. through technology fees without direct factory CAPEX.

1. Customer portfolio and LFP-led winner-takes-all

Even as customer risk rises, the source argues that order-book damage to CATL is asymmetrically smaller than for Korean battery peers. Higher rates and weaker demand hit expensive electric trucks and large SUVs, while consumers increasingly prefer affordable EVs; that keeps or raises demand for LFP batteries.

13%-14% revenue contribution

LFP supply for Model 3/Y standard range, return to Qilin and Shenxing products, and Nevada Megapack manufacturing partnership are the key points.

About 10% revenue contribution

Zeekr 001 and 009 use CATL’s third-generation CTP and Qilin batteries, helping defend shipments.

About 10% revenue contribution

Xiaomi became one of CATL’s fastest-growing tolling customers in April 2025, with SU7 and future derivative models supporting expansion.

The SNE Research data cited in the source puts CATL’s January-October 2025 global share at 38.1%, with BYD at 16.9%. The source treats this as structural outperformance versus competitors losing share.

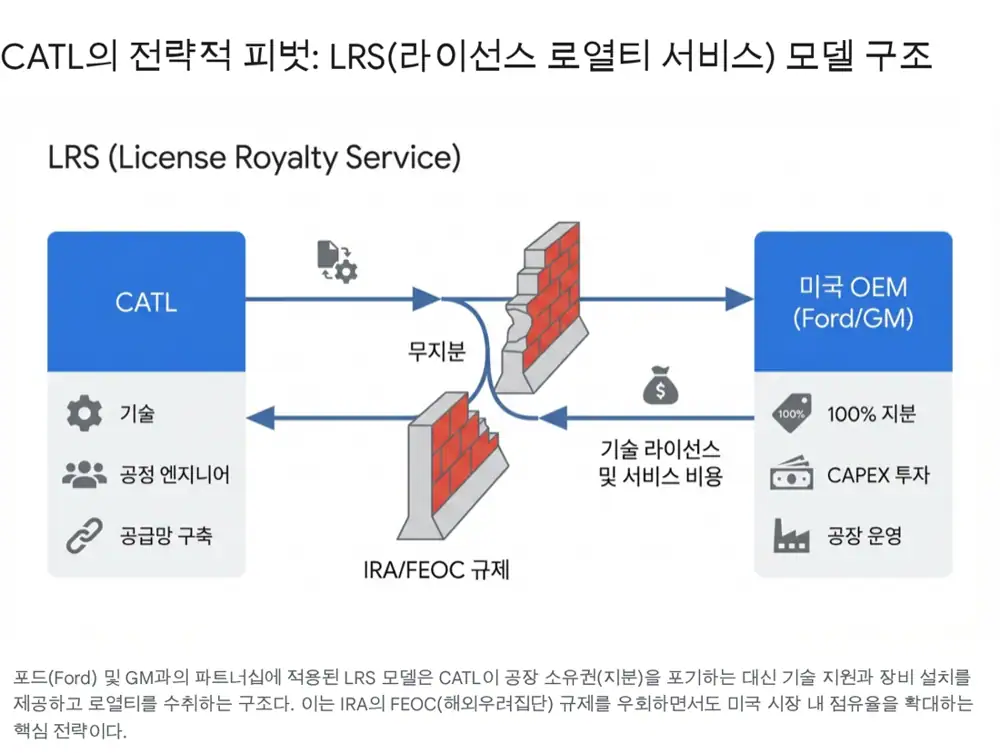

2. Ford-CATL and the LRS model

LRS, or License Royalty Service, is presented as a legal and business structure that bypasses trade barriers rather than a standard joint venture. Ford’s BlueOval Battery Park Michigan was reduced from 35GWh to 20GWh amid political controversy, but the CATL-technology LFP project is still targeting 2026 operation.

| Element | Source detail | Meaning |

|---|---|---|

| Ford | CATL LFP project remained while LG Energy Solution and SK On NCM projects were cancelled or delayed | Low-cost LFP technology is treated as essential for U.S. mass-market EVs |

| GM | Discussion of a similar LRS contract and U.S./Mexico LFP plant | Possible standardization beyond Ford |

| Tesla | CATL equipment and technology used for Nevada ESS line expansion | Technology-platform role in ESS as well as EVs |

| Capital efficiency | OEM owns the factory; CATL earns from technology licensing, equipment installation, and production support | Dollar cash flow without multi-trillion-won factory CAPEX and operating risk |

Interpretation: While Korean rivals shoulder debt and interest costs for U.S. joint ventures, CATL builds a North American technology-fee pipeline with minimal capital burden.

3. Utilization and operating leverage

Utilization determines profit quality in battery manufacturing. CAPEX from the 2021-2023 boom is now a depreciation burden for many rivals, but CATL still invested about RMB 10.1B in R&D alone during H1 2025 and continues to fund sites in Debrecen, Germany, and Indonesia.

- Second- and third-tier Chinese battery makers are described as operating below 50%, while CATL stayed around 90% in H1 2025 and “extremely high” in Q3.

- At 90% utilization, the company is well above a typical 70% break-even zone, so incremental revenue can flow through strongly to profit.

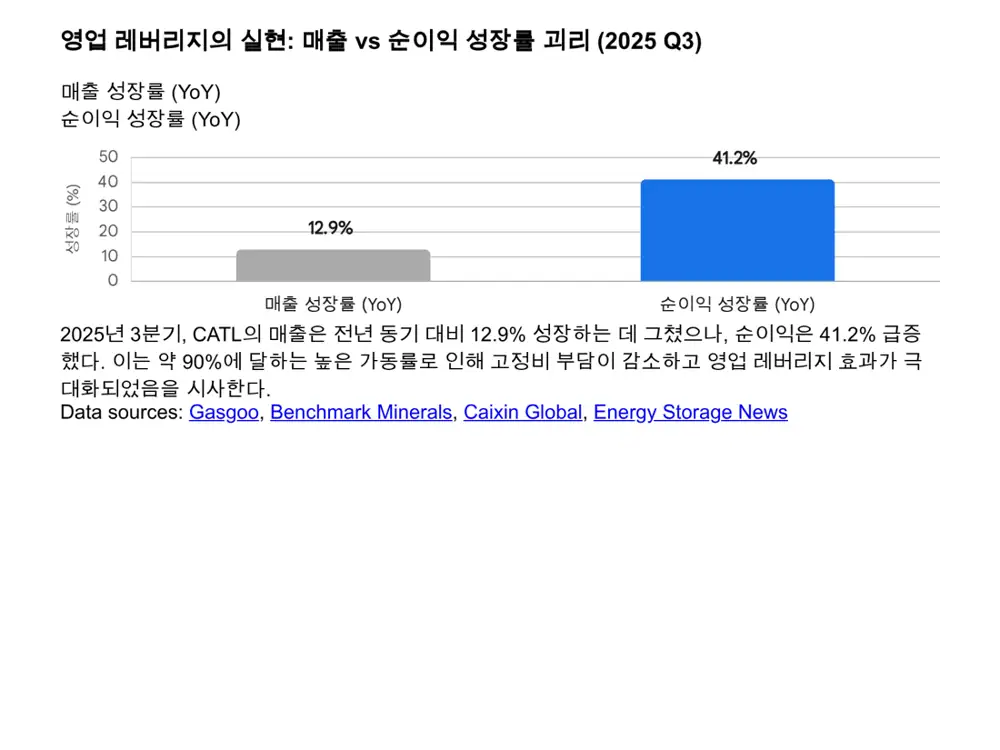

- Q3 2025 revenue was RMB 104.2B, up 12.9% year over year, while net profit jumped 41.2% to RMB 18.5B.

- The gap between revenue growth and earnings growth is interpreted as fixed-cost leverage despite raw-material price declines limiting reported revenue growth.

Inventory is not treated as toxic. Q3 2025 inventory was about RMB 80.2B, up 34% from year-end 2024, but inventory turnover days were stable. The source reads this as working capital tied to larger scale plus strategic stockpiling for Q4 China EV policy changes and year-end demand.

4. Hong Kong listing, overhang, and vertical integration

CATL diversified capital access with its May 2025 Hong Kong H-share secondary listing. But in November 2025, co-founder and third-largest shareholder Huang Shilin announced a plan to sell about 45 million shares, reducing his stake from 10.2% to 9.2%. The end of the six-month lockup for cornerstone investors opened the possibility of about 77.5 million additional shares entering the market.

Vertical integration is the raw-material hedge. Brunp Recycling closes the loop by recovering lithium, cobalt, and nickel from used batteries and feeding them back into cathode precursors. Sichuan lithium resources and Indonesian nickel projects raise internal mineral coverage, while mineral-resource revenue grew 27% year over year in H1 2025. The Tianhua New Energy stake increase is presented as a move to control lithium refining and processing.

5. Re-rating triggers and investment view

The source argues CATL is already beyond turnaround on earnings, but three leading indicators are needed to resolve the China discount and drive structural re-rating.

- Formal GM LRS agreement and construction start: a named U.S. or Mexico site would signal that FEOC risk is easing.

- Sodium-ion battery vehicle sales: before large-scale 2026 commercialization, early Chery models need to reach about 10,000 monthly units.

- ESS revenue share stabilizing above 20%: the source compares this with the current roughly 16%-19% share and looks for margins above the EV battery segment.

The final investment opinion in the source is Buy, or overweight. The reasons are cost competitiveness from 90% utilization, the LRS cash pipeline, and financial strength shown by 40% cumulative net-profit growth in the third quarter. Key risks remain shareholder-selling overhang, policy uncertainty in Europe and the U.S., and U.S.-China escalation such as a possible full ban on LRS structures.

Sources

- Naver Blog source: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224130191952

- Global Electric Vehicle Market Share: Quarterly - Counterpoint Research: https://counterpointresearch.com/en/insights/global-electric-vehicle-market-share-quarterly

- State of China Auto Market - December 2025 - Automobility: https://automobility.io/2025/12/state-of-chinas-auto-market-december-2025/

- CATL signs battery supply deal with Tesla until 2025 - electrive.com: https://www.electrive.com/2021/06/29/catl-signs-battery-supply-deal-with-tesla-until-2025/

- CATL technology licensing cooperation with GM - EqualOcean: https://equalocean.com/news/2024032920704

- Tesla Model Y, Geely Xingyuan, and Model 3 top global EV sales in Q3 - CnEVPost: https://cnevpost.com/2025/12/10/tesla-model-y-geely-xingyuan-model-3-top-global-ev-sales-q3/

- Xiaomi becomes CATL largest customer with 100000 vehicles sold - Metal News: https://news.metal.com/newscontent/103354504/Xiaomi-Motors-Emerges-as-CATLs-Largest-Customer-with-April-2025-Battery-Sales

- Global EV battery market share Jan-Oct 2025 - CnEVPost: https://cnevpost.com/2025/12/02/global-ev-battery-market-share-jan-oct-2025/

- Global EV Battery Installations Hit 933.5 GWh - ChinaEVHome: https://chinaevhome.com/2025/12/02/global-ev-battery-installations-hit-933-5-gwh-in-jan-oct-2025-catl-holds-38-1-byd-16-9/

- Ford expands CATL partnership scope - MarkLines: https://www.marklines.com/en/news/338085

- BlueOval Battery Park Michigan construction update - Ford: https://www.fromtheroad.ford.com/us/en/articles/2024/blueoval-battery-park-michigan-construction-progresses-alongside

- Ford gave up on beating China on batteries - Carscoops: https://www.carscoops.com/2025/12/ford-michigan-battery-plant-catl-lfp-tech/

- Ford partners with Chinese battery giant - Auto123: https://www.auto123.com/en/news/ford-catl-lfp-batteries-michigan-energy-storage/73531/

- CATL plans plant with GM through tech licensing - Moomoo: https://www.moomoo.com/news/post/35868181/catl-plans-to-build-plant-with-gm-in-north-america

- CATL YoY growth in H1 2025 - World-Energy: https://www.world-energy.org/article/53204.html

- CATL YoY growth in H1 2025 - Shanghai Metal Market: https://www.metal.com/en/newscontent/103458096

- CATL readies Hungary battery cell plant for production: https://www.batteriesinternational.com/2025/12/16/catl-readies-hungary-battery-cell-plant-for-production/

- CATL H1 profit soars 33% - ESS News: https://www.ess-news.com/2025/08/01/catl-h1-profit-soars-33-as-energy-storage-and-overseas-expansion-get-results/

- CATL Q3 revenue returns to over 100 billion yuan - Moomoo: https://www.moomoo.com/news/post/59970510/catl-s-q3-revenue-returns-to-over-100-billion-yuan

- CATL strong Q3 earnings - Gasgoo: https://autonews.gasgoo.com/m/70039496.html

- CATL Q3 energy storage shipments 36GWh - Tiger Brokers: https://www-web.itiger.com/news/1137812627

- CATL major shareholder stake reduction - Yicai Global: https://www.yicaiglobal.com/news/catl-drops-after-unveiling-third-largest-shareholder-plans-to-slash-its-holdings

- Lithium battery material stock abnormal fluctuation - Moomoo: https://www.moomoo.com/news/post/61620859/the-subsidiary-currently-has-no-plans-to-expand-production-capacity

- CATL shares fall over 8% after lockup ends - Tech in Asia: https://www.techinasia.com/news/catl-shares-fall-8-early-investors-sell-lockup-ends

- Charting the evolution of CATL revenue streams - Benchmark Source: https://source.benchmarkminerals.com/article/charting-the-evolution-of-catls-revenue-streams

- CATL invests RMB 2.6 billion to acquire stake - EnergyTrend: https://www.energytrend.com/news/20251103-50321.html

- CATL licensing LFP tech to GM - CarNewsChina: https://carnewschina.com/2024/03/28/catl-negotiating-licensing-lfp-battery-tech-to-gm-and-to-build-joint-factory/

- CATL new cell technology in 2026 - Electrek: https://electrek.co/2025/12/29/ev-battery-leader-catl-launching-new-cell-technology-2026/

- CATL sodium-ion batteries in 2026 - Caixin Global: https://www.caixinglobal.com/2025-12-30/catl-to-roll-out-sodium-ion-batteries-in-2026-to-cut-lithium-reliance-102398736.html

- CATL Q3 ESS battery shipments 36GWh - Energy-Storage.News: https://www.energy-storage.news/catls-q3-ess-battery-shipments-36gwh-market-share-capacity-constraints/