DEEP RESEARCH · AIRBUS

Airbus Deep Investment Analysis Report

Structural moat and industrial ramp-up in the shadow of Boeing’s crisis

0. Bottom line first

Airbus currently offers the lower-risk, higher-visibility side of the commercial aircraft duopoly. The case depends less on demand and more on A320/A350 ramp-up and supply-chain control.

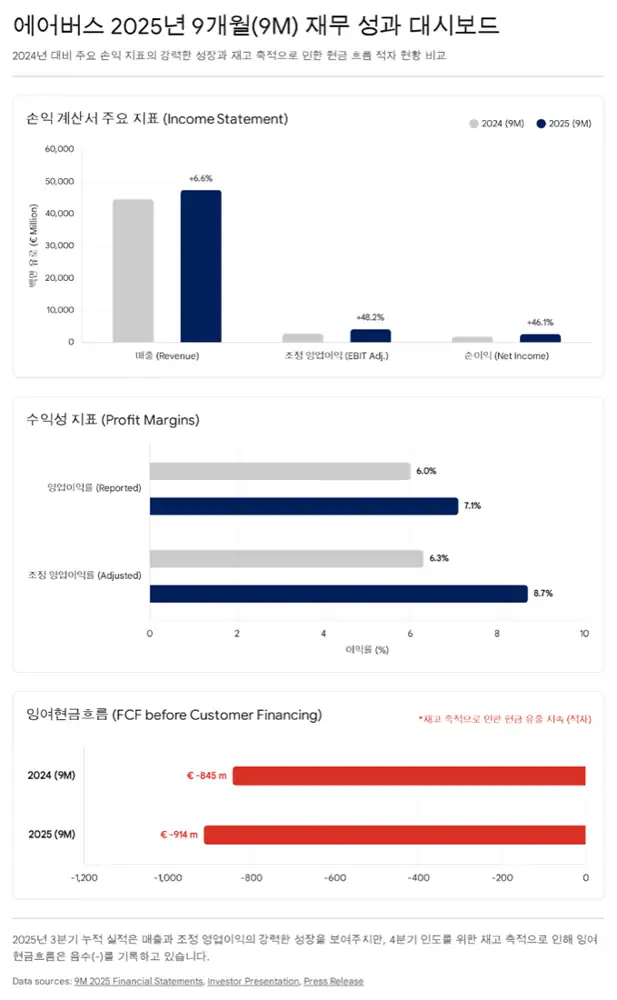

Official fact: The source cites 9M 2025 revenue of EUR 47.4B, 7% growth from EUR 44.5B, 507 commercial deliveries, adjusted EBIT of EUR 4.146B, net income of EUR 2.641B, and EPS of EUR 3.34.

Interpretation: Airbus’s premium is not only Boeing weakness. It is the combination of A321neo/A321XLR, net cash, backlog, and diversified production capacity.

1. 9M 2025 fundamentals

| Item | Number | Read-through |

|---|---|---|

| Revenue | EUR 47.4B | 7% growth from EUR 44.5B |

| Commercial deliveries | 507 aircraft | About 2% up from 497 |

| Adjusted EBIT | EUR 4.146B | 48% growth from EUR 2.798B |

| Net income / EPS | EUR 2.641B / EUR 3.34 | Shareholder-value capacity |

| FCF before customer financing | -EUR 914M | Inventory build for Q4 deliveries |

| Net cash | About EUR 7B | Room for R&D, buybacks, and supply-chain investment |

The cash-flow pressure should be read as inventory for ramp-up and late-year deliveries, not operational failure. The source contrasts Airbus’s “good inventory” with Boeing’s rework-driven “bad inventory.”

2. Backlog and product portfolio

Official fact: The source states Airbus backlog of 8,665 aircraft at the end of September 2025, Boeing backlog around 6,600 aircraft, and a gap of more than 2,000 aircraft.

The source says A321neo represents more than about 60% of the A320-family backlog. A321XLR expands into routes previously associated with widebodies, giving airlines a new route-planning tool.

3. Production ramp-up and Spirit assets

75 per month by 2027

Toulouse, Tianjin, Mobile expansion, and A321neo line conversion are key.

12 per month by 2028

Ramp from the current 5-6 per month level.

5 per month by 2029

Complements long-haul demand and the widebody portfolio.

The main risk is supply chain. The source highlights CFM and Pratt & Whitney part shortages, cabin interior delays, titanium and raw-material instability, and A320 fuselage-panel quality issues. The 2025 delivery target was cut from 820 to about 790 aircraft.

Official fact: Airbus is described as acquiring Airbus-related Spirit AeroSystems sites in Kinston, Belfast, Saint-Nazaire, and Casablanca, with about $439M in compensation from Spirit.

Interpretation: This is defensive vertical integration: Airbus accepts short-term losses to keep A220 and A350 supply away from competitor control and to manage quality and cost directly.

4. Airbus versus Boeing investment case

| Category | Airbus | Boeing |

|---|---|---|

| Balance sheet | About EUR 7B net cash | Source cites about $53B total debt |

| Valuation | 2026E P/E about 24-25x; EV/EBITDA about 17x | Traditional P/E difficult due to losses |

| 12-month share performance | About +25% | About +20% |

| Investment style | Quality Growth | Turnaround |

Risks

- A320neo production at 75 per month depends on supplier capacity.

- Raw materials, Russia-Ukraine, and China exposure can disrupt production or demand.

- If Boeing normalizes after 2026 and begins 777X deliveries, widebody competition could intensify.

5. Final view

Airbus is more than a beneficiary of Boeing’s problems. It is a quality-growth aerospace asset with the A321neo category killer and a stronger balance sheet. Supply-chain noise remains, but an 8,665-aircraft backlog and net cash support the long-term thesis.

I classify Airbus as a lower-risk, medium-high-return candidate. Because the stock already carries a premium, production execution and supplier issues will matter heavily.

Sources

- Naver source: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224130143067

- Hill Law Boeing crashes: https://www.jahlawfirm.com/boeing-plane-crashes/

- Wikipedia MAX groundings: https://en.wikipedia.org/wiki/Boeing_737_MAX_groundings

- Airbus 9M 2025 results: https://www.airbus.com/en/newsroom/press-releases/2025-10-airbus-reports-nine-month-9m-2025-results

- Forecast International Sep orders: https://flightplan.forecastinternational.com/2025/10/14/airbus-and-boeing-report-september-2025-commercial-aircraft-orders-and-deliveries/

- Forecast International Oct orders: https://flightplan.forecastinternational.com/2025/11/12/airbus-and-boeing-report-october-2025-commercial-aircraft-orders-and-deliveries/

- ePlaneAI 2025 orders: https://www.eplaneai.com/news/airbus-and-boeing-order-totals-for-2025-compared

- EngineCowl Boeing Q3: https://www.enginecowl.com/boeing-q3-2025/

- Forecast International production rates: https://flightplan.forecastinternational.com/2025/10/05/airbus-and-boeing-september-2025-production-rates-and-unofficial-deliveries/

- Aerospace Global News Airbus 2026: https://aerospaceglobalnews.com/news/airbus-2026-targets-expectations/

- ePlaneAI A320 flaw: https://www.eplaneai.com/news/regulator-orders-inspections-of-select-airbus-a320s-over-fuselage-flaw

- Airbus Spirit agreement: https://www.airbus.com/en/newsroom/press-releases/2025-04-airbus-signs-definitive-agreement-with-spirit-aerosystems

- Spirit acquisition: https://www.spiritaero.com/news/acquisition/

- Boeing Q3 results: https://investors.boeing.com/investors/news/press-release-details/2025/Boeing-Reports-Third-Quarter-Results/default.aspx

- Leeham Boeing CFO: https://leehamnews.com/2025/12/03/boeing-cfo-jay-malave-priorities-are-debt-investments-then-shareholders/

- Airbus buyback tranche: https://www.airbus.com/en/newsroom/press-releases/2025-11-airbus-launches-second-tranche-of-previously-announced-limited

- Airbus buyback commencement: https://www.airbus.com/en/newsroom/press-releases/2025-09-airbus-commences-limited-share-buyback-to-support-future-employee

- Finbox forward P/E: https://finbox.com/OTCPK:EADS.F/explorer/pe_fwd/

- Finbox EV/EBITDA: https://finbox.com/ENXTPA:AIR/explorer/ev_to_ebitda_ltm/

- Alpha Spread AIR vs BA: https://www.alphaspread.com/comparison/par/air/vs/nyse/ba

- Seeking Alpha Boeing FCF: https://seekingalpha.com/news/4527660-boeing-flies-9-after-cfo-sees-positive-free-cash-flow-next-year-turning-around-from-cash-burn

- Fintel Airbus forecast: https://fintel.io/sfo/us/eadsf