DEEP RESEARCH · SK NETWORKS/001740

SK Networks: Strategic Shift Toward an AI-Centric Operating Holding Company

A review of post-rent-a-car divestiture capital allocation, the AI value chain, balance-sheet repair, and SOTP re-rating potential.

0. Bottom line first

The central change is SK Networks moving from SKN 1.0 general trading and SKN 2.0 ICT distribution/rental toward SKN 3.0, an AI-centric operating holding company. The roughly KRW 820B proceeds from the 2024 SK Rent-a-Car sale provide the financial base to reduce asset-heavy exposure and move toward an AI and data-centered asset-light model.

P/B 0.43x

The source uses roughly KRW 1T market capitalization and P/B of 0.43x to argue that AI transition upside is barely reflected.

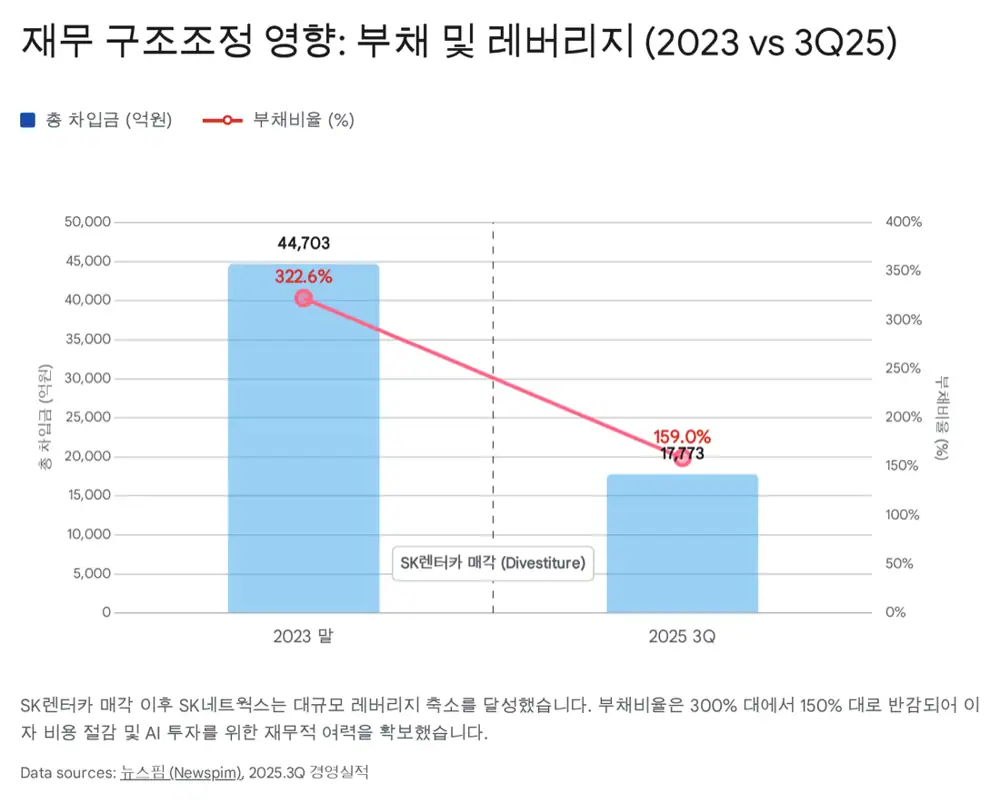

Debt ratio 322%→159%

The rent-a-car sale is described as lowering the debt ratio from about 322% at 2023 year-end to 159% in Q3 2025.

En-core, PhnyX, Upstage, S2W

The strategy bundles data, vertical AI, sLLM technology, and security intelligence for internal businesses and external B2B markets.

1. Identity shift

Official fact: SK Networks began as Sunkyong Textile in March 1953 and listed on KOSPI in 1977. It entered ICT handset distribution through the 1999 SK Distribution merger, added Walkerhill in 2009, acquired Tongyang Magic, now SK Magic, in 2016, and acquired AJ Rent-a-Car in 2019.

The source defines SKN 3.0, announced in 2024, as a shift of the center of gravity toward intangible assets: data and AI. The company has 30 consolidated subsidiaries and seven major subsidiaries across ICT, Walkerhill, SK Magic, En-core, and Speedmate. The creation of NAMUHX AMERICAS INC. and Haengboknamu is cited as evidence of AI and wellness-robotics expansion.

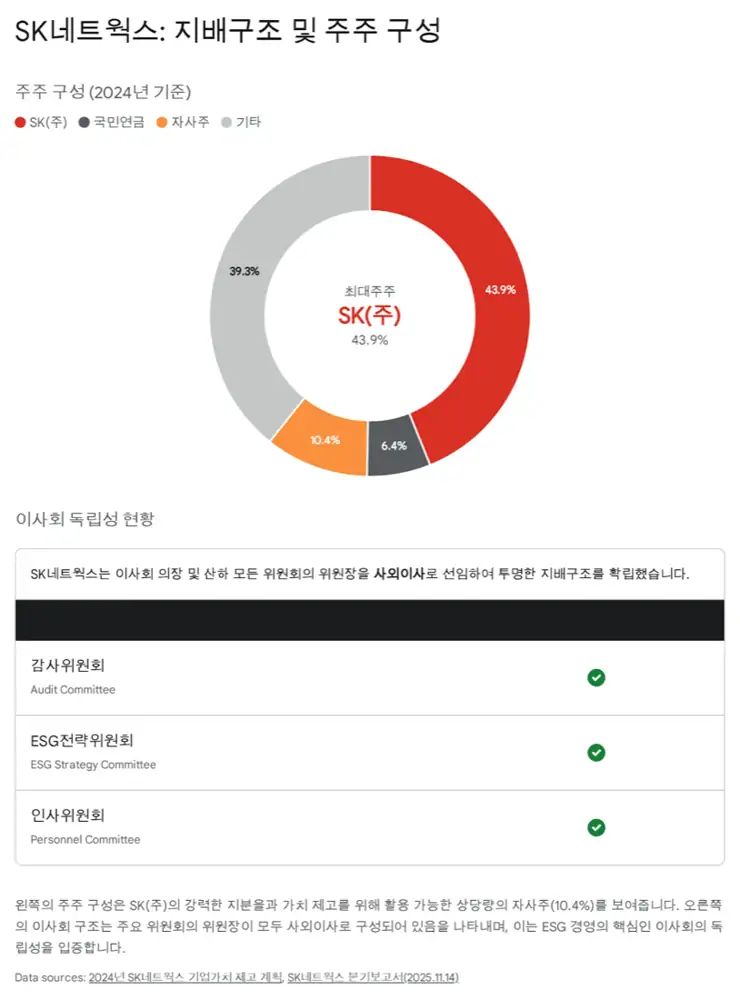

Official fact: SK Inc., the largest shareholder, is cited as holding roughly 43.90~45.6%, while the National Pension Service is presented as a key institutional investor with roughly 5.2~6.43%. Treasury shares are cited at roughly 10.4~12.4%, providing optionality for cancellation or strategic share swaps.

Official fact: Since 2019, the board chair and the chairs of audit, HR, strategy/ESG committees have all been outside directors, and the company discloses a Board Skills Matrix. The audit committee consists of three outside directors, and the KCGS governance rating improved from B+ in 2022 to A in 2023.

2. AI transition: making legacy businesses intelligent while importing external tech

| Axis | Role in the source | Investment point |

|---|---|---|

| En-core | Acquired in 2023; a domestic leader in data management and consulting | Data layer and B2B AI-readiness market |

| SK Magic/SK Intelix | Wellness robotics and NAMUH X launch in 2025 | Extending purifier rentals into AI home robots and vital-sign checks |

| Speedmate | Spun off in September 2024; AI estimating with DAT | Transparency and efficiency in auto aftermarket maintenance |

| Walkerhill | AI guide and AI lounge | Customer-service automation and personalized service data |

| PhnyX Lab | Founded in Silicon Valley in 2024; developer of Cheiron | Adopted by about 60 companies including 10 leading Korean pharma companies; raised $4M externally |

Interpretation: SK Networks is not trying to build its own foundation model. The approach is closer to using En-core for data, Upstage’s Solar sLLM for model capability, PhnyX for industry-specific applications, and S2W for security trust.

3. Management and execution

Ho-jung Lee

Presented as leading AI democratization and business-model innovation, including major restructuring decisions such as the SK Rent-a-Car sale.

Sung-hwan Choi

Presented as the CIO/CSO-like leader behind HICO Capital, PhnyX Lab, Upstage investment, and future-business sourcing.

Yong-min Hwang

Analyzed as the capital-allocation coordinator balancing debt repayment, new investment, and shareholder returns after the rent-a-car sale.

4. Q3 2025 financials: structure matters more than headline shrinkage

| Item | Source figure | Interpretation |

|---|---|---|

| Q3 consolidated revenue | KRW 1.9726T, down 3.4% YoY | Strategic downsizing after Globalwide split-off and low-margin trading reduction |

| Operating profit | KRW 22.3B, down 22.0% YoY | Reflects NAMUH X launch marketing and early AI R&D costs |

| ICT segment | Revenue up 46.9% QoQ | New handset releases show cash-cow resilience |

| Rent-a-car sale | About KRW 820B | Debt reduction and AI investment funding |

| Debt ratio | About 322% at 2023 year-end → 159% in Q3 2025 | Deleveraging from asset/liability removal and sale gains |

| Total borrowings | About KRW 20T → KRW 17.7T | Reduced lease-debt and interest burden |

| Cash and short-term financial products | About KRW 554.9B at Q3 2025 | Dry powder for AI M&A, new investments, and shareholder returns |

Official fact: The source cites AA- stable corporate bond ratings and A1 commercial-paper ratings.

Interpretation: Headline revenue and operating profit look weak, but the company is also exiting low-return activities and strengthening the balance sheet. The risk is that AI spending becomes a structural burden rather than a temporary investment phase.

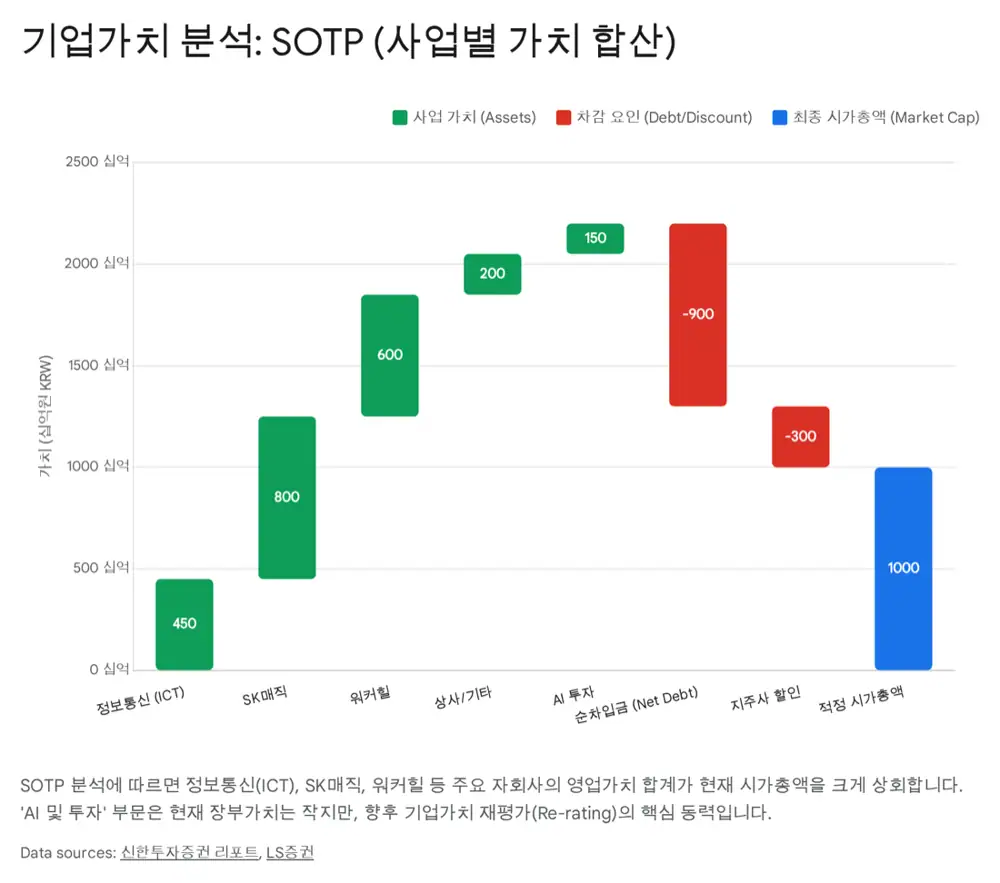

5. Competition and SOTP valuation

Unlike POSCO International or LX International, which focus on energy, food, and minerals, the source frames SK Networks as an “AI general trading company” that trades data and AI capability. In Korea’s AI market, it is not directly challenging foundation-model leaders such as Naver HyperCLOVA X, Kakao, or LG EXAONE; it is focusing on vertical AI plus data preparation and security infrastructure.

| SOTP component | Source valuation logic |

|---|---|

| ICT | Stable annual operating profit of KRW 40~50B; applying a distribution multiple implies about KRW 400~500B in value |

| Walkerhill | Gwangjin-gu real estate value provides asset downside support above book value |

| Speedmate & Globalwide | Potential re-rating from independent profitability-focused operations after spin-offs |

| SK Magic/Intelix | Potential for above-rental-sector multiples if re-rated as a robotics company |

| AI portfolio | En-core, Upstage stake, and PhnyX Lab are lightly reflected on book value but function like call options if listed or externally funded |

Official fact: The source cites current market capitalization at about KRW 1T and P/B at 0.43x. It also cites consensus target prices around KRW 6,000~6,233, implying more than 30~40% upside from the current share price.

6. Shareholder returns, risks, and final view

Official fact: The dividend policy targets about KRW 200 per share annually and a dividend yield around 4~5%. The company introduced an interim dividend from 2024 and changed the dividend record date to after the dividend amount is confirmed. Treasury shares are about 10~12% of total shares.

| Risk | Metric to monitor |

|---|---|

| Delayed AI monetization | PhnyX and En-core B2B revenue growth and recurring revenue |

| Weakening legacy cash cows | Domestic consumption, SK Magic, and Speedmate profitability |

| Treasury-share overhang | Potential shareholder-value dilution if shares are used for acquisitions instead of cancellation |

Interpretation: The setup is downside support from Walkerhill real estate and ICT cash flow plus upside optionality from AI transition. Near-term triggers are concrete shareholder-return plans and early 2026 KPIs from new AI products. The source states a BUY view, but this report records that as the source scenario, not as a recommendation.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224130116887

- 뉴스핌 LS증권 3Q25 Review: https://www.newspim.com/news/view/20251112001006

- Goover SK네트웍스 분석: https://seo.goover.ai/report/202512/go-public-report-ko-c819c9e4-0d1b-41c3-95e6-23e2ca5947e7-0-0.html

- SK Networks 뉴스룸 2026 조직개편: https://www.sknetworks.co.kr/pr/news-room/5aq12UXV7bwodc6P

- 파이노미 2025 최고의 순간: http://www.finomy.com/news/articleView.html?idxno=246657

- 뉴스로드 AI로 빛난 2025년: http://www.newsroad.co.kr/news/articleView.html?idxno=51727

- 문화경제 SK스피드메이트: http://m.weekly.cnbnews.com/m/m_article.html?no=188309

- 조선일보 워커힐 AI 라운지: https://www.chosun.com/special/special_section/2025/08/29/BGUKCQJGSZH55CQP56OIGRYQIA/

- SK Networks 워커힐 AI 작품: https://www.sknetworks.co.kr/pr/news-room/migzybfulRC2qQ5P

- 시사오늘 SK네트웍스 AI WAVE 2025: http://www.sisaon.co.kr/news/articleView.html?idxno=175540

- 디지털비즈온 피닉스랩 400만 달러 투자: http://www.digitalbizon.com/news/articleView.html?idxno=2340590

- Shinhan SK네트웍스 PDF: https://drive.google.com/open?id=1dRSxpccpOoZhZOLWKKLp8o2nBubgvoZJ

- S2W 기업 분석 Google Drive: https://drive.google.com/open?id=1k_zkeNm1WmzH-e6g6bCWjX197UNJrw45-DsG10aINyg

- 조선비즈 S2W SK AI 서밋 2025: https://biz.chosun.com/it-science/ict/2025/11/03/FDDRSR6N35C4BCXXTQEZMNXYHE/

- SK Networks 구성원 AI 역량 강화: https://www.sknetworks.co.kr/pr/news-room/SxGmedehLLmpsMZq

- 뉴스포스트 이호정 대표 나무엑스: https://www.newspost.kr/news/articleView.html?idxno=213837

- 오피니언뉴스 AI 투자기업 변곡점: https://www.opinionnews.co.kr/news/articleView.html?idxno=122529

- 한국금융신문 소버린 AI: https://www.fntimes.com/html/view.php?ud=2025091812351354257fd637f543_18

- 주달 SK네트웍스 투자분석 2025.12.29: https://www.judal.co.kr/?view=stockAI&shareToken=CiECXtjYXJYj1wC1

- 주달 SK네트웍스 투자분석 2025.12.21: https://www.judal.co.kr/?view=stockAI&shareToken=K30C43x3qpr29cFD

- 더파워 2분기 깜짝 실적: https://www.thepowernews.co.kr/view.php?ud=202507141346124022de3f0aa1be_7