DEEP RESEARCH · SK INNOVATION/SK ON RESTRUCTURING

SK Innovation: Structural Transformation or Financial Life Support?

A quality-of-turnaround review through the EV chasm, Ford-BlueOval SK restructuring, AMPC optics, and the SK E&S merger.

0. Bottom line first

I do not treat SK Innovation’s 2025 profit swing as a clean turnaround. The SK E&S merger is a liquidity breakwater, but it does not fix SK On’s low asset turnover, weak North American utilization, or AMPC-dependent earnings structure. The source conclusion is Hold due to structural competitiveness erosion.

Ford JV reset

Kentucky Plants 1 and 2 move to Ford; the Tennessee plant moves to SK On.

45GWh idle-asset risk

If alternative customers cannot fill more than 70% utilization by 2026 start-up, the site can become stranded.

Need subsidy-excluded profit

SK On’s Q3 operating profit of KRW 17.9B reflects AMPC benefits; underlying manufacturing profit is still estimated to be negative.

1. EV chasm and customer risk

As of Q3 2025, the global battery industry is going through more than a demand slowdown; it is in an EV chasm. SK Innovation is using cash flow from refining, lubricants, and LNG to support SK On, a battery subsidiary that has not yet reached structural profitability.

Interpretation: The order-backlog logic supporting SK On’s value has weakened after the BlueOval SK restructuring with Ford. The belief that signed contracts do not change has been broken, and backlog only becomes cash flow if customer EV production plans remain intact.

2. BlueOval SK split: Kentucky and Tennessee are asymmetric

Official fact: The source interprets the December 2025 dissolution and asset split of the BlueOval SK JV between Ford and SK On as a structural change in North American battery supply chains. The original 50:50 plan to build three plants in Kentucky and Tennessee was revised because of EV demand weakness and Ford’s strategic shift.

| Asset | Ownership | Source interpretation |

|---|---|---|

| Kentucky Glendale Plant 1 | Ford sole ownership | Started operation in August 2025 and supplies batteries for F-150 Lightning and others |

| Kentucky Plant 2 | Ford sole ownership | Construction paused; Ford gains battery-supply control |

| Tennessee Stanton BlueOval City | SK On sole ownership | About 45GWh of CAPA, but with risk from the absence of committed captive volume |

The Tennessee plant was designed for Ford’s next-generation electric trucks, but now SK On must secure third-party customers or urgently convert the line for ESS. The source says that if utilization above 70% is not secured by the 2026 start-up point, the site could become a stranded asset with depreciation pressure.

Official fact: Ford’s Marshall, Michigan battery plant uses licensed CATL LFP technology rather than SK On’s NCM. The source sees this as a signal that North America is shifting from high-performance NCM toward lower-cost LFP.

3. Top-three customers: revisit backlog quality

| Customer | Status | Meaning for SK On |

|---|---|---|

| Ford | F-150 Lightning cuts, next-gen EV delays, indefinite Kentucky Plant 2 delay | Lower Kentucky utilization and weaker volume guarantees are the largest risk |

| Hyundai/Kia | HMGMA in Georgia is preparing operation, while battery internalization and LGES cooperation also expand | Potential outlet for Tennessee idle volume, but full absorption is uncertain as EV targets are adjusted |

| Volkswagen | European EV demand weakness has led to production cuts or pauses at Zwickau and Emden | Delays utilization recovery at SK On’s Hungary plants in Ivancsa and Komarom |

Interpretation: Every customer risk ultimately converts into utilization risk. Battery plants are fixed-cost-heavy assets, so lower volume hurts profitability nonlinearly.

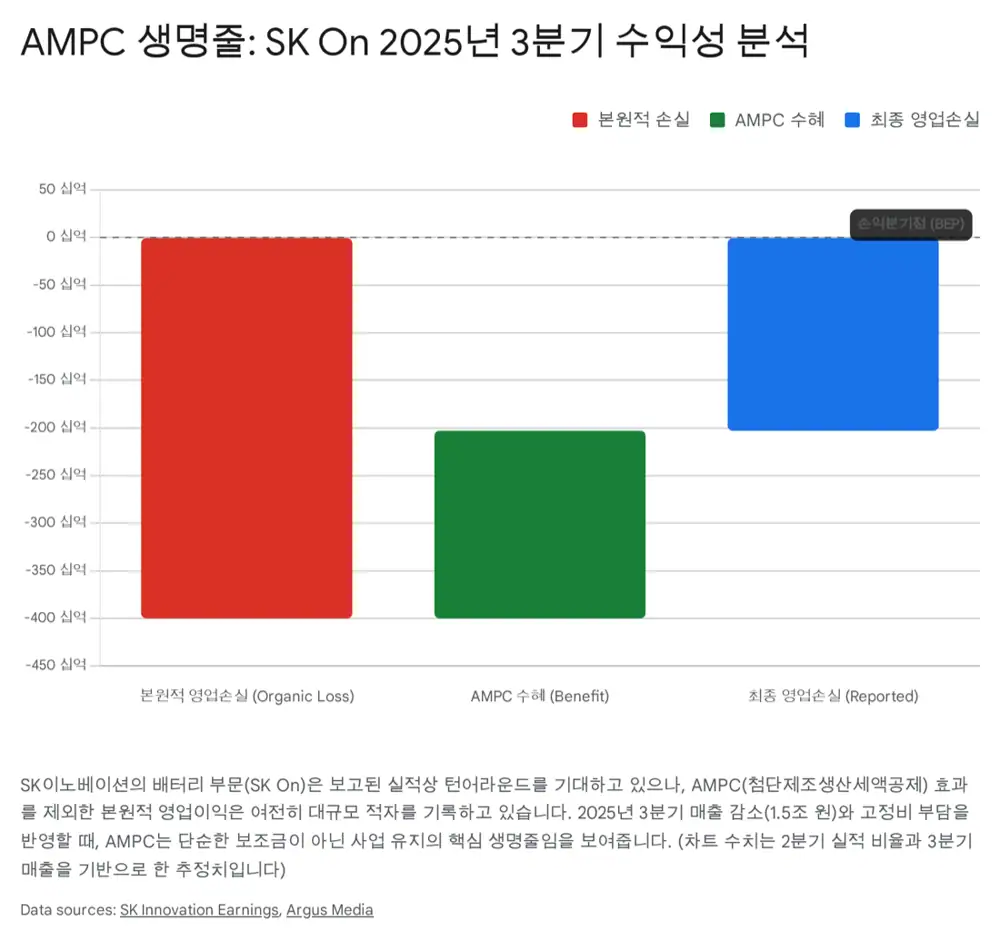

4. Earnings quality: strip out AMPC

Official fact: In Q3 2025, SK Innovation reported consolidated operating profit of KRW 573.5B, and SK On reported operating profit of KRW 17.9B on the surface.

Interpretation: The source argues that this figure must be analyzed after removing AMPC, the U.S. IRA advanced manufacturing production credit. Using Q2 AMPC scale and market consensus in the mid-to-high KRW 200B range, it estimates SK On’s underlying manufacturing operating loss remained in the KRW 200B range.

Global utilization estimated at 60~70%

North American lines likely sit below breakeven because of Ford Kentucky Plant 2 delays and Tennessee volume gaps.

Depreciation burden

Even idle factories generate hundreds of billions of won in annual depreciation.

Inventory-turnover check

Weak OEM sales can leave cell inventory at both SK On and OEM warehouses, creating valuation-loss risk if raw-material prices fall.

A true turnaround should be confirmed when inventory turnover rises for two consecutive quarters and the production-sales-cash conversion cycle accelerates. If the current profit swing comes from subsidies, oil-price tailwinds, and merger effects, it must be separated from manufacturing competitiveness.

5. Mergers and governance: synergy or financial support?

Official fact: SK Innovation completed its merger with SK E&S on November 1, 2025, and also merged subsidiaries SK On and SK Enmove. The source frames this as capital reallocation for SK On’s survival.

| Restructuring | Effect | Risk |

|---|---|---|

| SK E&S merger | Stable gas and LNG-power earnings/EBITDA can support SK On’s CAPEX and losses | Existing shareholders face merger-ratio controversy and conglomerate-discount risk |

| SK On-SK Enmove merger | Lubricant-base-oil profit can offset SK On losses and help IPO preparation | Immersion-cooling synergy is a long-term R&D topic; near term, it looks like internal subsidy |

| FI overhang | The merger buys time against put options and until IPO timing | If SK On’s own profitability is delayed, parent burden grows |

Interpretation: SK E&S is a cash-flow safety net for SK On. But if strong subsidiaries’ cash is used for too long to support weak or low-return businesses, the equity market can apply a conglomerate discount.

6. Three signals for a real turnaround

- North American utilization recovery: watch for Ford Kentucky Plant 2 construction restart, hiring spikes, F-150 Lightning inventory clearing, and monthly improvement in Korean cathode exports to the U.S.

- Tennessee ESS order win: confirmed POs with Hyundai Motor Group or large energy/utilities are needed. It must be a committed contract, not merely “under discussion.”

- LFP yield and price competitiveness: official announcement of more than 90% LFP production yield or large supply contracts for value EVs are needed.

The source says SK Innovation’s investment case ultimately depends on utilization, or Q. Current PBR is near historical lows and the SK E&S merger lowers bankruptcy risk, but without utilization above breakeven, apparent undervaluation can become a value trap.

7. Final investment view

Interpretation: The conclusion is Hold. The Ford partnership split shows SK On’s technology and price competitiveness are not irreplaceable, and AMPC-dependent profitability plus Tennessee idle-asset risk remain unresolved.

- Valuation: Much of the bad news is reflected, and the SK E&S merger supports downside.

- Trap: Subsidy-dependent profit is vulnerable to policy change.

- Strategy: Watching for visible merger synergy and new Tennessee customers is more rational than new entry. A longer horizon into H1 2026, when North American EV inventory adjustment may finish, is needed.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224129849266

- The EV Report: https://theevreport.com/ford-and-sk-on-dissolve-blueoval-sk-joint-venture

- electrive.com SK On and Ford split: https://www.electrive.com/2025/12/12/sk-on-and-ford-split-us-battery-venture/

- WDRB Ford ends partnership: https://www.wdrb.com/news/business/ford-ends-sk-on-partnership-takes-full-control-of-kentucky-battery-plant-amid-ev-downturn/article_31999428-a218-4ca9-a25c-5d366c3a6b21.html

- electrive.com Kentucky plant: https://www.electrive.com/2025/08/20/blueoval-sk-opens-battery-cell-plant-in-kentucky/

- Just Auto: https://www.just-auto.com/news/sk-on-ford-to-end-us-battery-jv/

- Battery Tech Online: https://www.batterytechonline.com/battery-manufacturing/what-the-ford-sk-on-split-means-for-the-battery-supply-chain

- Electrek Ford LFP plant: https://electrek.co/2025/06/25/ford-stands-by-controversial-lfp-battery-plant-to-cut-ev-costs/

- Ford From the Road LFP plant: https://www.fromtheroad.ford.com/us/en/articles/2025/ford-owned-american-battery-plant-future-electric-vehicles

- Seeking Alpha Ford write-down: https://seekingalpha.com/news/4531652-ford-shifts-ev-strategy-takes-195b-write-down-and-drops-current-lightning-production

- Ford strategy update: https://www.fromtheroad.ford.com/us/en/articles/2025/ford-reinvests-trucks-hybrids-affordable-electric-vehicles

- HMGMA grand opening: https://www.hmgma.com/2025/03/26/hyundai-motor-group-metaplant-america-celebrates-grand-opening-powering-u-s-economic-growth/

- Hyundai Motor Group Metaplant: https://www.hyundaimotorgroup.com/en/story/CONT0000000000174940

- SK On-HMG MOU: http://eng.sk-on.com/company/press_view.asp?idx=47&page=1&schtxt=&CompanyCode=011

- EV.com Volkswagen: https://ev.com/news/volkswagen-pauses-ev-production-at-two-german-plants-amid-slower-demand

- Electrek Volkswagen: https://electrek.co/2025/09/26/volkswagen-cuts-id-4-other-ev-output-as-plant-shutdowns-loom/

- Chosun SK Innovation Q3: https://www.chosun.com/english/industry-en/2025/10/31/WEVCJABFURBSXMQCY4IVUXZVEE/

- SK merged entity launch: https://eng.sk.com/news/sk-innovations-merged-entity-officially-launches-setting-sail-as-the-largest-private-energy-company-in-asia-pacific