DEEP RESEARCH · SAMSUNG SDI

Samsung SDI: Turnaround Conditions and the Trap in a Premium Strategy

A review of the EV chasm, delayed LFP pivot, idle assets, and whether the ESS shift can work.

0. Bottom line first

My conclusion is that Samsung SDI looks cheap, but still needs proof. P/B of 0.7-0.8x creates valuation appeal, but the large Q3 2025 operating loss, KRW 2.3tn CAPEX burden, demand weakness at Rivian, Stellantis, and BMW, and delayed LFP response all require structural competitiveness to be verified. The real reversal signals are actual ESS shipments after line conversion, confirmed Rivian R2 supply, and STM returning to profit.

1. Q3 2025: the scorecard that challenged the premium strategy

Official fact: The source reports Samsung SDI's Q3 2025 revenue at KRW 3.05tn, down 22.5% YoY. Operating profit swung to a KRW 591.3bn loss, and cumulative CAPEX from 2024 through Q3 2025 is presented at about KRW 2.3tn.

The issue is that this weakness is not just cyclical. Samsung SDI has emphasized profitable growth through premium products such as NCA and Gen 5/6 batteries, but the mass-market EV phase is moving quickly toward LFP, price, and safety.

2. Customer risk: Rivian, Stellantis, BMW

LFP backlash

The source flags slowing R1T and R1S sales, liquidity pressure, and adoption of Gotion LFP in Standard Range trims. Samsung SDI's share in R2 is not guaranteed.

SPE ramp-up dilemma

StarPlus Energy's Kokomo 1 plant began ahead of schedule in December 2024 but faced lower-than-expected market demand. Flexible operation of a new factory can mean low utilization and wider early losses.

Last stronghold

BMW has maintained prismatic-battery demand in premium EVs, but European EV slowdown and cylindrical adoption from Neue Klasse add supply-chain diversification pressure.

Official fact: The source cites SNE Research data saying Samsung SDI's global EV battery usage from January to October 2025 declined 4.6% YoY.

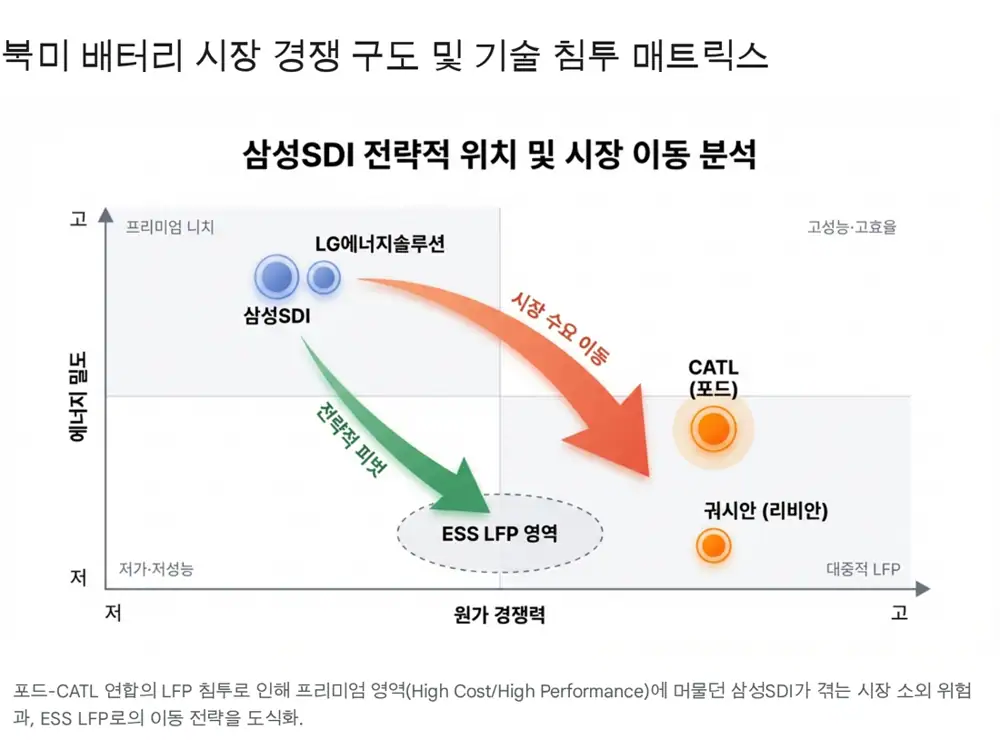

3. Ford-CATL model and technological decoupling risk

The source sees Ford's North American LFP plant using CATL technology under a licensing royalty service model as a central threat. It could set a precedent for Chinese low-cost and high-safety LFP technology to enter North America while working around IRA FEOC restrictions.

Interpretation: Even if Samsung SDI's premium products are technically strong, they may not be chosen if market criteria shift from longer range toward lower price and fire safety. That is the technological decoupling risk described in the source.

Samsung SDI has announced plans to convert some ternary lines in Ulsan and overseas plants to LFP and to mass-produce ESS LFP batteries in North America after 2026. The source still treats the 2027-ish full LFP ramp as a risk because CATL's scale and cost advantage may be hard to overcome.

4. Asset efficiency: idle capacity and negative operating leverage

| Item | Source figure/view | Meaning |

|---|---|---|

| Cumulative CAPEX | About KRW 2.3tn as of Q3 2025 | Hungary Plant 2, Malaysia cylindrical Plant 2, and StarPlus Energy |

| Some-line utilization | Some small-battery lines estimated below 50% | Delayed power-tool recovery and lower Rivian volume |

| BEP utilization | Battery plants are described around 60-70% | New North American lines and small-battery lines may be below break-even |

| Inventory turnover | About 3.6x at end-2024 | Likely worsened after Q3 2025 revenue decline and customer inventory adjustment |

Battery cell manufacturing is an equipment-heavy business with large fixed costs. Depreciation continues even when revenue falls. That is why a 22.5% Q3 2025 revenue decline turning into a large operating loss is a textbook case of negative leverage.

5. Governance and STM: stability and burden coexist

Official fact: The source says Samsung SDI's largest shareholder is Samsung Electronics, with a stake of about 19.58%.

The governance structure is stable, but the source is cautious about the absence of meaningful insider buying during the share-price decline. STM, the cathode-material subsidiary, was a cost-competitiveness weapon in boom times, but in a downturn it can transmit lower parent utilization into consolidated fixed-cost pressure.

6. Turnaround checklist and my view

- North American ESS line conversion and real shipments: large shipments of ESS batteries such as SBB 1.7 or SBB 2.0 need to be confirmed. The source views the recent KRW 2tn North American ESS contract positively, but the revenue recognition timing in 2027 leaves a gap.

- Confirmed Rivian R2 platform supply: whether Samsung SDI's 46-series cylindrical or prismatic battery is adopted in R2 is the key to the small-battery growth engine.

- STM utilization rebound and profit turn: STM earnings are presented as a leading indicator for Samsung SDI cell-plant utilization.

Therefore my view is Hold, or wait-and-see. Until successful LFP ESS mass production and fixed-cost reduction appear in numbers, confirmation before entry is more rational than simply buying weakness. I would also assume the earnings winter can continue through Q4 2025 and H1 2026.

Sources

- Source 1: Original Naver Blog post · https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224129847662

- Source 2: Samsung SDI Q3 2025 earnings results · https://www.samsungsdi.com/sdi-now/sdi-news/4562.html

- Source 3: AlphaSense: Samsung SDI Q3 2025 earnings highlights · https://www.alpha-sense.com/earnings/006400.kr

- Source 4: SNE Research: Jan-Oct 2025 non-Chinese EV battery usage · https://www.sneresearch.com/en/insight/release_view/548/page/0

- Source 5: Korea JoongAng Daily: Samsung SDI Q2 loss · https://koreajoongangdaily.joins.com/news/2025-07-31/business/industry/Samsung-SDI-shifts-to-Q2-loss-on-extended-EV-slowdown/2366085

- Source 6: The Diplomat: Ford-CATL deal · https://thediplomat.com/2025/12/the-ford-catl-deal-should-become-the-model-for-china-us-economic-cooperation/

- Source 7: Samsung SDI ESS LFP supply deal in the U.S. · https://www.samsungsdi.com/sdi-now/sdi-news/4642.html

- Source 8: Samsung SDI Q1 2025 earnings results · https://samsungsdi.com/sdi-now/sdi-news/4344.html

- Source 9: Finbox: inventory turnover data · https://finbox.com/DB:SSU/explorer/inventory_turnover/

- Source 10: Samsung 2025 3Q Interim Report PDF · https://images.samsung.com/is/content/samsung/assets/global/ir/docs/2025_3Q_Interim_Report.pdf

- Source 11: Samsung SDI consolidated financial statements 2024/2023 · https://www.samsungsdi.com/upload/download/ir/SDI_Audit%20report_2025.02.21_eng.pdf

- Source 12: Mirae Asset: Samsung SDI report · https://securities.miraeasset.com/bbs/download/2138268.pdf?attachmentId=2138268