DEEP RESEARCH · L&F

L&F: Battery Value-Chain Reset and the Post-Tesla Contract Inflection

A combined review of high-nickel NCMA95, mid-nickel, LFP, balance-sheet pressure, and the Tesla direct-supply reset.

0. Bottom line first

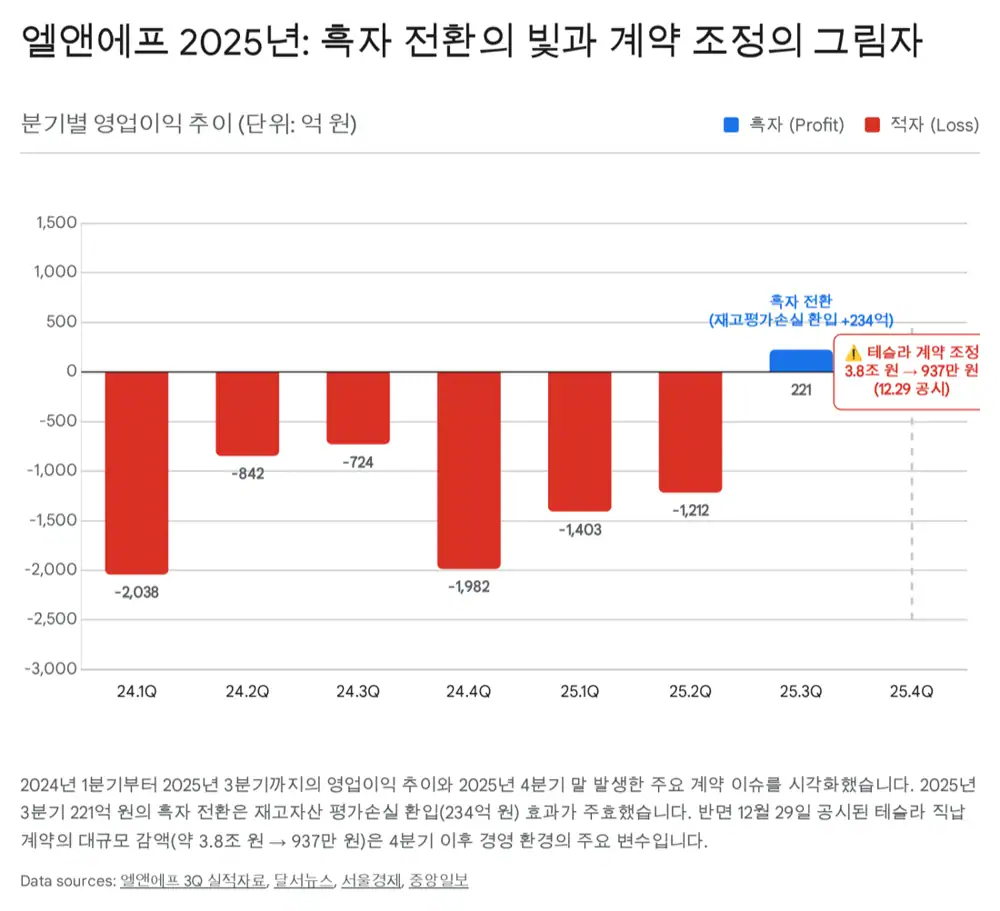

For L&F, 2025 was both a year of operating improvement and expectation reset. The company turned profitable in Q3 after eight quarters, with standalone Q3 revenue of KRW 652.3B and operating profit of KRW 22.1B. But on December 29, 2025, the Tesla direct-supply contract was revised from KRW 3.8347T to KRW 9.73M, sharply reducing future optionality.

Q3 returned to profit

Q3 revenue rose 25.4% QoQ and operating profit improved 118.2%.

High-nickel core

High-nickel products were 85% of shipments, and NCMA95 was 80% within the high-nickel mix.

Non-China supply-chain option

A 30,000-ton LFP line at Guji Plant 3 targets mass production in Q3 2026, with a plan to expand to 60,000 tons.

1. Business structure and governance

Official fact: L&F was founded in 2000, pivoted from LCD backlight units to cathode active materials, is headquartered at 11 Igokdong-ro, Dalseo-gu, Daegu, and transferred from KOSDAQ to KOSPI on January 29, 2024. As of September 30, 2025, it was classified as a mid-sized company, not a venture company, and the source cites BB+ ratings from Korea Ratings Data and NICE Investors Service.

| Entity | Source figure | Role |

|---|---|---|

| JH Chemical | 91.29% owned; assets about KRW 100.4B; liabilities about KRW 62.4B | Precursor production and localization |

| Wuxi Guangweilai New Materials | 65.81% owned by L&F | China supply-chain foothold, though recent production is understood to be suspended |

| L&F Plus | 100% subsidiary established in Q3 2025; assets about KRW 123.1B | Potential vehicle for LFP cathodes, battery recycling, and other new businesses |

Official fact: At the end of Q3 2025, shares outstanding were 36,316,174 and capital was about KRW 18.1B. Saeronics was the largest shareholder with 14.43%, and treasury shares were 7.54%.

Interpretation: Saeronics’ participation in BW subscription and share-backed borrowing can signal confidence in future growth, but margin-call risk should be monitored if the share price weakens.

2. Q3 2025 financials: quality of the turnaround

| Item | Source figure | Meaning |

|---|---|---|

| Cumulative revenue/operating loss | Revenue KRW 1.5371T; operating loss KRW 239.3B | First-half losses remain in cumulative results |

| Standalone Q3 result | Revenue KRW 652.3B; operating profit KRW 22.1B | First operating profit after eight quarters |

| Cost of sales | Cumulative KRW 1.7124T | Still above revenue on a cumulative basis |

| Inventory valuation reversal | About KRW 23.4B | Stabilizing lithium and mineral prices supported profit |

| SG&A | Cumulative KRW 63.9B | Read as a natural increase with sales scale |

Interpretation: The KRW 23.4B reversal is accounting-related, but even excluding it, core profitability appears to have moved close to breakeven. The turnaround matters because it confirms utilization recovery and product-mix improvement.

3. Balance sheet and cash flow: liquidity improved, leverage remains

| Category | Source figure | Checkpoint |

|---|---|---|

| Total assets | KRW 2.9756T, up 6.3% from KRW 2.7998T at year-end | Reflects capex and working capital |

| Current assets/cash | Current assets KRW 1.2018T; cash KRW 315.7B | Cash rose about 13% from KRW 279.5B at year-end |

| Receivables/inventory | Receivables and other receivables KRW 289.1B; inventory KRW 545.8B | Inventory fell from KRW 574.6B at year-end |

| Liabilities/equity | Liabilities KRW 2.5998T; equity KRW 375.8B | Liabilities were up 25% from year-end |

| Debt pressure | Short-term borrowings KRW 787.3B; current long-term debt KRW 146.9B | Short-term repayment pressure is the key variable |

Official fact: Cumulative operating cash flow was -KRW 8.6B, worse than KRW 216.6B a year earlier. Non-cash items included KRW 25.1B of inventory valuation loss and KRW 64.0B of depreciation. Investing cash outflow was KRW 89.1B, with PP&E purchases of KRW 73.5B versus KRW 181.8B a year earlier. Financing cash flow was a KRW 137.5B inflow, including KRW 297.5B of BW issuance and KRW 100.0B of CB issuance.

Interpretation: L&F defended liquidity proactively, but interest expense and dilution risk remain. From 2026 onward, new-line utilization and orders need to justify the cost of financing.

4. CAPA and product roadmap

Official fact: Key sites include the Daegu Dalseo headquarters/Plant 1, Waegwan Plant 2 in Chilgok, and Guji Plants 1, 2, and 3 in Daegu National Industrial Complex. At the end of Q3 2025, PP&E book value was KRW 1.2666T, with machinery KRW 470.0B, land KRW 108.3B, buildings KRW 393.2B, and construction-in-progress KRW 136.6B.

Exact utilization is not disclosed, but the source says management indicated utilization had recovered to the breakeven level. Given utilization was below 50% in 2024, the source estimates Q3 2025 utilization normalized to around 60~70%.

Official fact: The LFP line at Guji Plant 3 is being built with annual capacity of 30,000 tons, with mass production targeted for Q3 2026 and a later expansion plan to 60,000 tons. Precursor internalization through JH Chemical is described as a core response to IRA and other supply-chain rules.

5. Tesla contract reduction: less current revenue loss, more lost future optionality

Official fact: On December 29, 2025, L&F revised the value of the high-nickel cathode supply contract signed with Tesla in February 2023 from KRW 3.8347T to KRW 9.73M. The source interprets this as a 99.99% reduction and effectively a contract termination.

The source attributes the change to delays in Tesla’s 4680 cylindrical battery mass production, yield and process challenges, weak Cybertruck sales, and policy uncertainty such as the potential repeal of EV subsidies under the Trump administration. However, actual 2024~2025 revenue from the contract was presented as less than KRW 10M, so current cash-flow damage is viewed as limited.

Interpretation: This is less a collapse in earnings estimates and more a removal of future multiple support. The core pipeline is not direct Tesla supply but indirect supply to models such as Model 3/Y through LG Energy Solution; the source says LGES-bound NCMA95 shipments are increasing.

6. R&D and post-2026 checkpoints

KRW 29.45B

Cumulative Q3 2025 R&D expense, about 1.9% of revenue.

Single crystal, mid-nickel, LFP

The source cites IP across cathode active material production, precursor technologies, and recycling.

Customer diversification

Long-term growth depends on reducing LGES/Tesla concentration through SK On, European OEMs, Hyundai Motor Group, and others.

The source defines 2025 as a year of restructuring. Q3 profit was helped by raw-material rebound and FX, but it also reflected utilization recovery and NCMA95 adoption. From 2026 onward, the core checkpoints are successful LFP mass production, maintaining the NCMA95 quality gap, and proving customer diversification in numbers.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224129767276

- KIND 정정 투자설명서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250725000194&docno=&viewerhost=&

- 달서인터넷뉴스 3분기 흑자 전환: http://dalseonews.co.kr/front/news/view.do?articleId=ARTICLE_00019872

- 전자신문 3분기 흑자 전환: https://www.etnews.com/20251030000022

- 컨콜노트 LFP 신사업: https://contents.premium.naver.com/ystreet/irnote/contents/251029174546387hi

- Daum 하이니켈·LFP 전망: https://v.daum.net/v/20251029184248804?f=p

- 서울경제 테슬라 수주 축소: https://www.sedaily.com/NewsView/2H1X3FU7Q9

- Korea Daily 테슬라 계약 해지: https://www.koreadaily.com/article/20251229020543790

- KFE 특징주 보도: https://www.kfenews.co.kr/news/articleView.html?idxno=651944

- Electrek 4680 supply chain: https://electrek.co/2025/12/29/tesla-4680-battery-supply-chain-collapses-partner-writes-down-dea/

- Zacks 4680 deal slashed: https://www.zacks.com/stock/news/2810023/teslas-cybertuck-faces-major-roadblock-as-4680-battery-deal-slashed

- The Business Times: https://www.businesstimes.com.sg/international/teslas-vanishing-order-hastens-fall-us800-million-fortune

- 한국경제 새 계약 논의: https://www.hankyung.com/article/2025123015316