DEEP RESEARCH · Oklo

Oklo: An Advanced Nuclear Platform Targeting the AI Power Bottleneck

A look at Aurora, HALEU, DOE pilots, cash runway, and short-seller risks

0. Bottom line first

Oklo is not just a reactor designer. It aims to own and operate plants and sell power and heat under long-term contracts as an Energy-as-a-Service company. The AI data-center power bottleneck is a large market, but the 2027 operation target, HALEU supply, NRC licensing, and FOAK cost are major risks.

Official fact: The source says Oklo was founded in 2013 by MIT alumni Jacob DeWitte and Caroline Cochran, and its name comes from the 1.7-billion-year-old natural reactor phenomenon in Oklo, Gabon.

Interpretation: Oklo's investment appeal is not only the reactor design but the business model: selling long-term power and heat through PPAs without forcing customers to carry plant CAPEX.

1. Technology: Aurora's Design Logic

Fast neutron reactor

Maintains fission with fast neutrons, aiming for higher uranium utilization and waste-burning potential.

Liquid metal cooling

Sodium boils around 883°C at atmospheric pressure, reducing high-pressure-system burden.

Simplification and modularity

Fewer moving parts and factory-built modules aim to reduce construction time and quality variance.

5-20% enriched fuel

Central to the technology and also the central supply-chain risk.

2. Licensing and Government Tracks

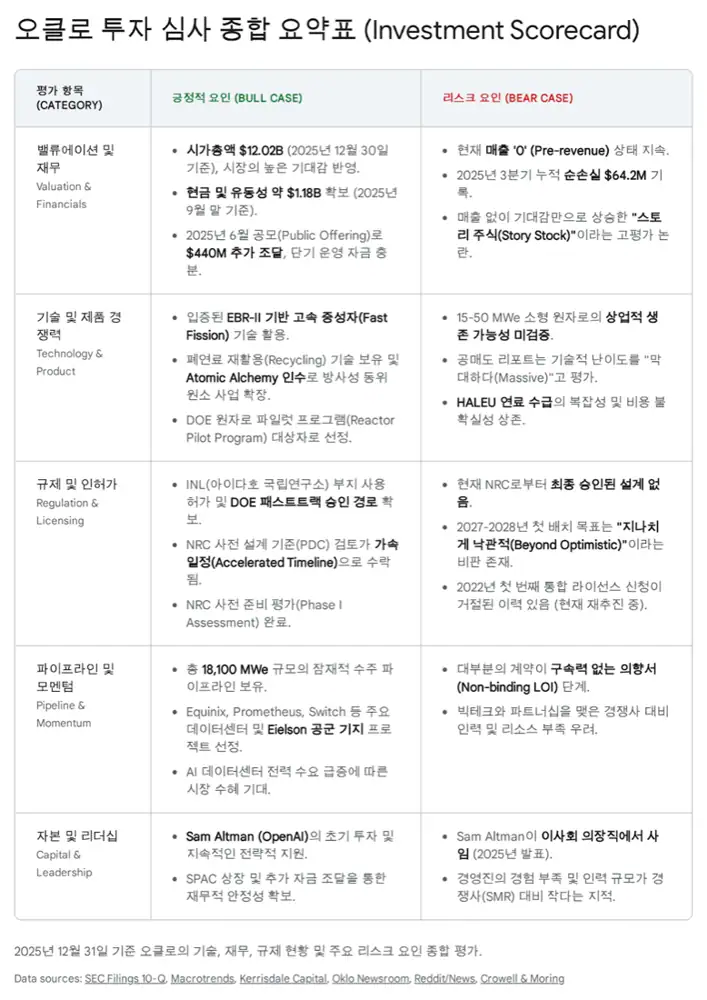

The source highlights Oklo's 2020 first-of-kind COLA filing and the NRC's 2022 denial for insufficient information as an important failure lesson. In September 2025, the NRC accepted Oklo's principal design criteria topical report for accelerated review, which the source reads as an improved regulatory signal.

Official fact: The source says Oklo was selected for the DOE Reactor Pilot Program in August 2025, enabling Aurora-INL construction and operation under DOE oversight, and was selected for the U.S. Air Force Eielson AFB microreactor project.

Interpretation: DOE and defense tracks can accelerate demonstration outside the ordinary commercial-license path, but mass commercial deployment still requires safety proof and repeatable construction execution.

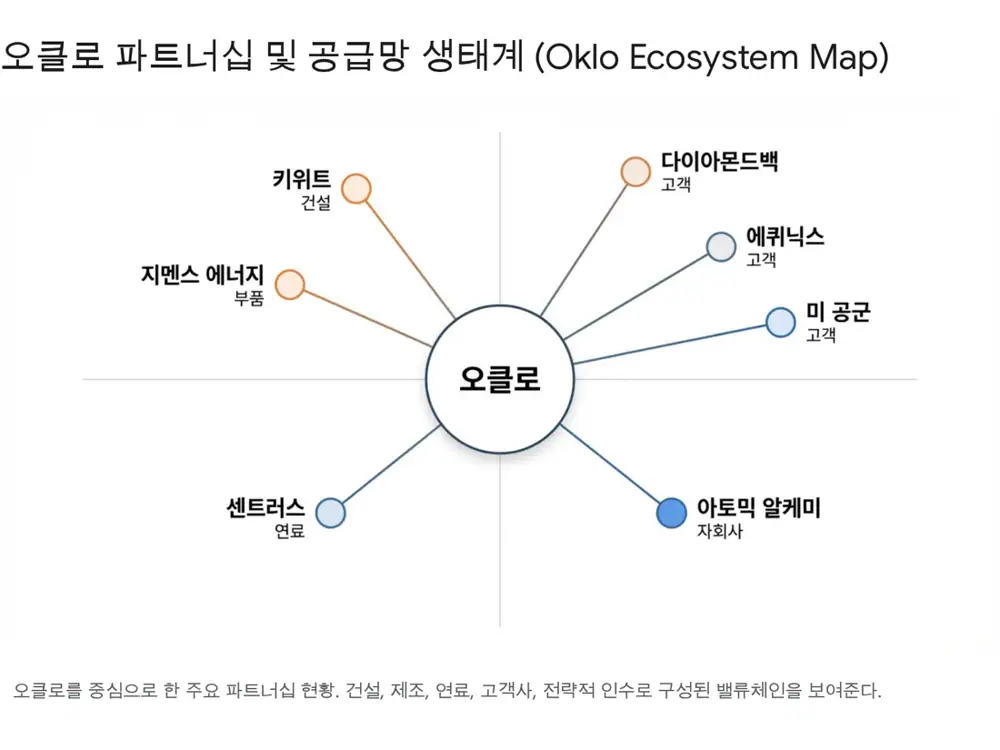

3. Partnerships: A Fabless Nuclear Ecosystem

| Area | Partner/customer | Source detail |

|---|---|---|

| Construction | Kiewit | July 2025 MSA; design and construction for the INL project |

| Power conversion | Siemens Energy | November 2025 binding contract for power conversion system |

| Fuel | Centrus Energy | Partnership with a U.S. HALEU license holder |

| Data centers | Equinix | LOI for up to 500 MWe |

| Industry | Diamondback Energy | 20-year Permian Basin power LOI, 50 MW |

| Isotopes | Atomic Alchemy | February 2025 all-stock acquisition for USD 25 million |

4. Financials and Valuation

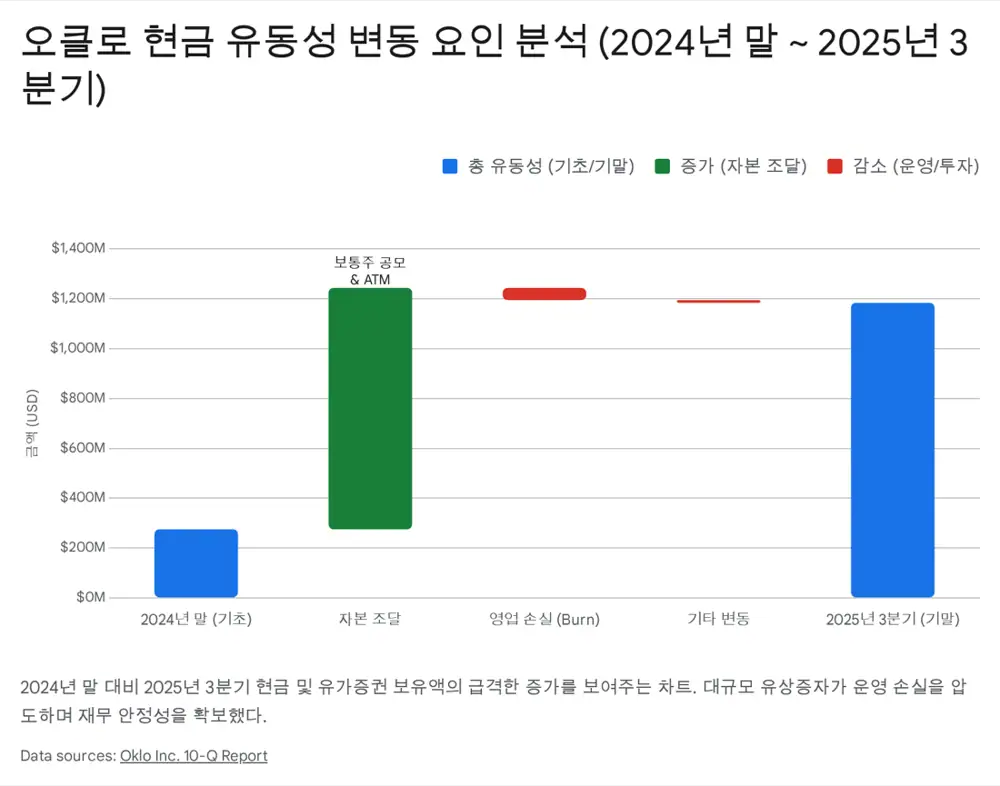

Official fact: As of September 30, 2025, the source lists USD 410 million of cash and equivalents, USD 511.56 million of current marketable securities, and USD 261.96 million of non-current marketable securities, or about USD 1.183 billion of liquid assets.

| Item | Source figure | Read |

|---|---|---|

| Liquid assets at 2024 year-end | About USD 227.8 million | Before 2025 financing |

| Liquid assets at Sep. 30, 2025 | About USD 1.183 billion | Follow-on and ATM funding effect |

| Q3 2025 net loss | About USD 29.72 million | Deep-tech growth-company loss profile |

| YTD Q3 2025 net loss | USD 64.22 million | Higher R&D, G&A, and acquisition costs |

| Simple runway | About 7-10+ years | Buffer before full construction ramp |

| Market cap | About USD 11-12 billion in late Dec. 2025 | AI infrastructure premium and overheating debate coexist |

5. Risks: Short Report and Technical Execution

- Kerrisdale Capital disclosed a short position in November 2024, questioning the realism of 2027 operations, HALEU cost assumptions, and management's lack of large nuclear construction experience.

- The source accepts some criticism as valid but argues DOE RPP and Air Force selection show some government confidence in execution.

- Liquid sodium can react violently with air or water, so design controls must be proven.

- FOAK cost is a chronic first-unit nuclear risk. Cash may look sufficient, but long delays could accelerate burn.

6. My Conclusion

Oklo could become an energy-sector Tesla, but today it is still a pre-revenue deep-tech nuclear company. Near term, I would track NRC/DOE milestones, quarterly burn rate, HALEU supply, insider sales, and short-seller arguments. For long-term investors, the source's conclusion remains sensible: only a very limited allocation as a hedge on AI-infrastructure power bottlenecks.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224129765902

- Reference: https://www.macrotrends.net/stocks/charts/OKLO/oklo/market-cap

- Reference: https://www.nasdaq.com/articles/heres-why-i-wouldnt-touch-oklo-10-foot-pole

- Reference: https://www.world-nuclear-news.org/articles/oklo-selects-constructor-for-first-aurora-powerhouse

- Reference: https://oklo.com/newsroom/news-details/2025/Oklo-and-Siemens-Energy-Sign-Binding-Contract-to-Expedite-Procurement-of-the-Power-Conversion-System-for-Commercial-Power-Plant/default.aspx

- Reference: https://www.kerrisdalecap.com/wp-content/uploads/2024/11/OKLO-Kerrisdale.pdf

- Reference: https://www.kerrisdalecap.com/investments/oklo-inc/

- Reference: https://www.world-nuclear-news.org/articles/us-companies-sign-up-with-oklo-for-microreactor-po

- Reference: https://www.reddit.com/r/OKLOSTOCK/comments/1nv75h1/oklo_selected_by_us_department_of_energy_for/

- Reference: https://www.ans.org/news/2025-06-16/article-7114/air-force-issues-notice-to-partner-with-oklo-on-microreactor-deployment-in-alaska/

- Reference: https://oklo.com/newsroom/news-details/2025/Oklo-Closes-Acquisition-of-Radioisotope-Producer-Atomic-Alchemy/default.aspx

- Reference: https://en.wikipedia.org/wiki/Oklo_Inc

- Reference: https://www.ycombinator.com/blog/jacob-dewitte-oklo-interview/

- Reference: https://oklo.com/investors/governance/executive-management/default.aspx

- Reference: https://alum.mit.edu/slice/commercializing-next-generation-nuclear-energy-technology

- Reference: https://mcj.vc/inevitable-podcast/caroline-cochran

- Reference: https://oklo.com/newsroom/news-details/2025/Oklo-Announces-Chairman-Transition/default.aspx

- Reference: https://www.world-nuclear-news.org/articles/oklo-and-siemens-energy-sign-power-conversion-system-contract

- Reference: https://oklo.com/newsroom/news/default.aspx

- Reference: https://www.centrusenergy.com/news/oklo-and-centrus-energy-sign-memorandum-of-understanding-for-fuel-components-and-power-procurement-to-support-the-deployment-of-advanced-fission-technologies-in-southern-ohio/

- Reference: https://investor.equinix.com/news-events/press-releases/detail/1079/equinix-collaborates-with-leading-alternative-energy

- Reference: https://www.crowell.com/en/insights/firm-news/crowell-and-moring-represents-nuclear-energy-startup-atomic-alchemy-in-its-acquisition-by-oklo

- Reference: https://robinhood.com/us/en/stocks/OKLO/

- Reference: https://www.investing.com/analysis/red-screens-green-future-2-ways-to-buy-the-nuclear-sector-dip-200672553

- Reference: https://www.trefis.com/data/companies/OKLO/no-login-required/ztIiXH9i/OKLO-Stock-Falls-14-With-A-5-day-Losing-Spree-On-Insider-Selling