DEEP RESEARCH · LG Energy Solution

LG Energy Solution: Battery Leader Waiting for a Structural Pivot Through the Chasm

A hard look at GM risk, Tesla 46-series optionality, ESS conversion, and parent-company overhang

0. Bottom line first

LGES remains a top-tier non-China battery alternative, but utilization and asset efficiency now matter more than growth. My stance is NEUTRAL, with Positive Watch if 46-series ramp and ESS conversion become visible.

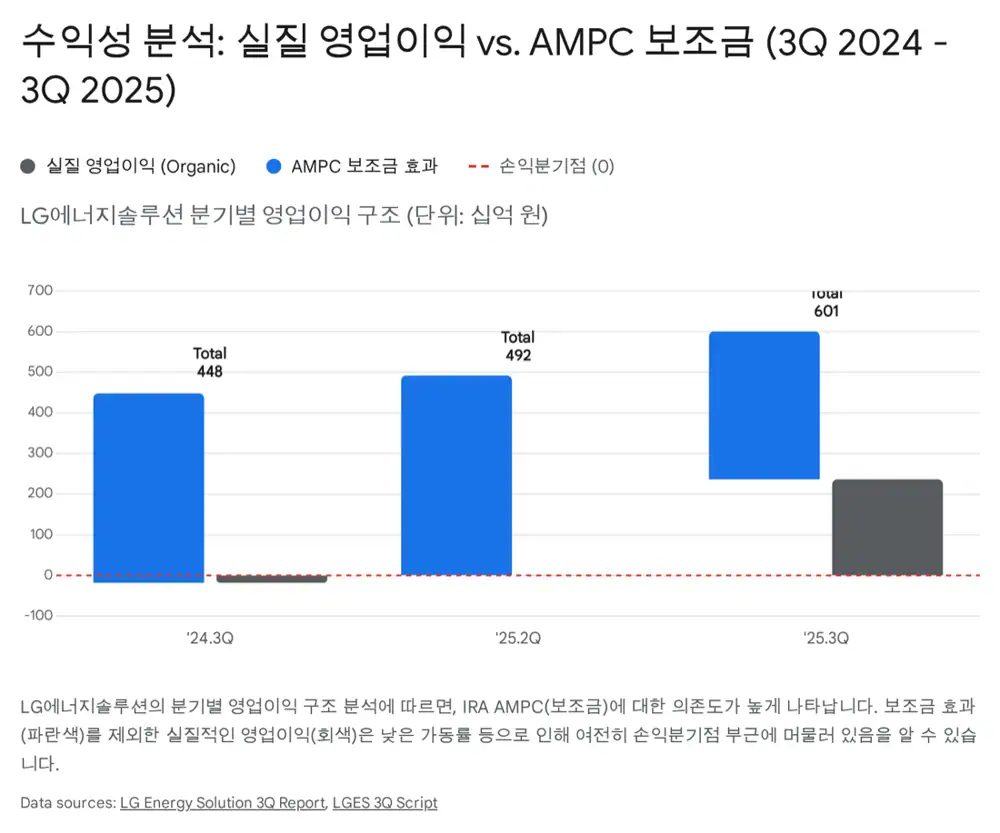

Official fact: Based on Q3 2025 performance and strategy, the source highlights AMPC dependence, GM Ultium Cells volume adjustments, Ford-CATL LFP licensing, and LG Chem stake overhang as core issues.

Interpretation: Even if the stock reflects much of the chasm fear, it is more rational to add after confirmation than to buy aggressively before operating leverage recovers.

1. Customer Risk: GM From Growth Engine to Volatility

The source views Ultium Cells, the LGES-GM joint venture, as the symbol of North American expansion but now reassesses it as the largest risk. Shutdowns or layoffs at Ohio and Tennessee plants and a halted Michigan third plant are interpreted as evidence of GM missing EV sales targets and carrying inventory pressure.

High dependence / high risk

Production cuts directly affect equity-method profit and fixed-cost burden.

High dependence / medium risk

Trouble with 4680 insourcing could benefit LGES if its 46-series ramp succeeds.

Medium dependence / low risk

Stable through EV and hybrid balancing, but explosive growth is limited.

Low dependence / high structural risk

CATL technology licensing could erode the non-China premium.

2. Tesla 46-Series: Opportunity Created by Insourcing Difficulty

Official fact: The source says Tesla's 4680 battery, especially dry-electrode versions, has faced yield issues and that related supply-chain contract reductions could raise LGES external-supply opportunity.

Interpretation: If LGES stabilizes 46-series mass production in Ochang and Arizona in late 2025 or early 2026, it could offset GM weakness. But Tesla business also carries pricing pressure.

3. Asset Efficiency: CAPEX Diet and ESS Conversion

| Item | Source figure/detail | Meaning |

|---|---|---|

| PP&E | About KRW 43 trillion as of Q3 2025 | High fixed cost and depreciation burden |

| Some-line utilization | Industry estimate around 60% | Below estimated 70% BEP creates reverse leverage |

| Core OPM ex-AMPC | 4.1% | Earnings power without policy support remains weak |

| 2025 CAPEX | 20-30% reduction YoY planned | Cash-flow defense and slower investment pace |

| Inventory | KRW 4.88 trillion vs KRW 4.55 trillion at 2024 year-end | Write-down risk if slowdown persists |

| Utilization trigger | 80% framed as profit-explosion threshold | Key operating-leverage indicator |

The source frames EV-to-ESS line conversion in Michigan and Canada as a survival strategy to avoid stranded idle assets. The key question is whether North American grid and data-center ESS demand can fill the capacity while EV demand is delayed.

4. Governance and Overhang

LG Chem is described as the largest shareholder with about 81.8% of LGES. The source says LG Chem has indicated a long-term plan to lower its stake to around 70% to improve its financial structure and fund new growth areas. Exchangeable bonds backed by LGES shares add another supply-pressure layer.

5. My Checklist

- Tesla 4680/46-series equipment installation and yield-stabilization news.

- Large ESS awards from North American utilities or big tech.

- Ultium Cells rehiring notices and local restart news.

- Lower IRA/AMPC uncertainty after the U.S. election cycle.

Interpretation: This is a confirmation-first setup, not a V-shaped rebound call. If 46-series, LFP production, and ESS conversion align after 2026, the structural-growth scenario reopens.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224129764458

- Reference: https://www.foxbusiness.com/lifestyle/gm-lays-off-over-1700-workers-indefinitely-ev-demand-slows

- Reference: https://www.just-auto.com/news/gm-cut-ev-battery-jobs/

- Reference: https://www.businesskorea.co.kr/news/articleView.html?idxno=221668

- Reference: https://millichronicle.com/2025/10/58382.html

- Reference: https://www.webpronews.com/tesla-supplier-slashes-2-9b-4680-battery-deal-99-amid-setbacks/

- Reference: https://electrek.co/2025/12/29/tesla-4680-battery-supply-chain-collapses-partner-writes-down-dea/

- Reference: https://s24.q4cdn.com/526396163/files/doc_earnings/2025/q3/earnings-result/ILMN-Q3-2025-Earnings-Release.pdf

- Reference: https://www.kedglobal.com/batteries/newsView/ked202512170012

- Reference: https://www.carscoops.com/2025/12/ford-michigan-battery-plant-catl-lfp-tech/

- Reference: https://www.trendforce.com/news/2025/01/02/news-korean-battery-makers-lg-energy-solution-samsung-sdi-and-sk-on-reportedly-hit-by-lower-utilization/

- Reference: https://news.lgensol.com/company-news/press-releases/3587/

- Reference: https://www.lgensol.com/upload/file/audit-report/2025_1Q_LGES_Audit_Report_FS_en.pdf

- Reference: https://www.channelnewsasia.com/business/lg-chem-plans-sell-lg-energy-solution-stake-shareholder-returns-5494836

- Reference: https://www.morningstar.com/news/dow-jones/202511281529/lg-energy-solution-shares-slump-after-parent-plans-to-cut-stake

- Reference: https://englishdart.fss.or.kr/dsbh001/main.do?rcpNo=20250520800255

- Reference: https://investor.gm.com/news-releases/news-release-details/gm-releases-2025-third-quarter-results

- Reference: https://www.energy-storage.news/energy-storage-demand-offsets-ev-slowdown-driving-lg-energy-solution-profit-increase/