DEEP RESEARCH · SMR SECTOR

Small Modular Reactor Sector Due Diligence

A diligence view of AI power demand, policy support, and execution risk across leading SMR companies

0. Bottom line first

My central read is that the SMR sector has moved beyond the 2024 phase of concept design and licensing preparation and into a 2025 phase of deployment capital and supply-chain buildout. The investment question is less about the label on the reactor and more about execution capability, balance-sheet capacity, and confirmed demand.

Official fact: The source highlights NuScale Power's 6GW TVA collaboration, X-energy's more than $1.2 billion of cumulative private capital, Holtec's Palisades restart approval, and Iljin Power's 2025 third-quarter cumulative revenue of KRW 193.1 billion and operating profit of KRW 10.3 billion.

Interpretation: AI data-center power demand and carbon-neutrality constraints are putting nuclear power back on the investment agenda because it can provide dense 24/7 baseload power. SMR, however, still has to pass tests around FOAK cost, fuel supply, and regulatory timelines.

1. Macro: AI power demand and policy support

In 2025, the global energy market sits at the collision point between AI data-center electricity demand and net-zero targets. The source emphasizes that this is not merely a government slogan cycle; hyperscalers such as Amazon, Google, and Microsoft are committing capital because dependable power has become a business requirement.

Data-center electricity consumption is expected to increase by more than 160% by 2030 versus current levels. Generative AI training and inference need uninterrupted high-density power, and intermittent renewables alone cannot guarantee the 99.999% uptime that data centers require.

Official fact: Microsoft's 20-year PPA with Constellation Energy to restart the Three Mile Island nuclear site is used in the source as a directional example of market urgency. Related source links include Constellation announcement and Fox News article.

On policy, the U.S. ADVANCE Act is framed as an effort to modernize advanced-reactor licensing and shorten reviews toward an 18- to 24-month range. The White House and DOE's Genesis Mission is presented as a plan to use AI to optimize reactor design and accelerate commercialization. Korea's 11th Basic Electricity Plan supports the domestic ecosystem with plans to build three large reactors and one SMR by 2038 and raise nuclear's power mix share to 35.6%.

| Demand/policy axis | Meaning in the source | Investor checkpoint |

|---|---|---|

| AI data centers | Power consumption forecast to rise more than 160% by 2030 | Track actual PPAs and power offtakers |

| Big Tech capital | More investment and construction funding for SMR developers | Separate interest from signed contracts and funded commitments |

| U.S. policy | ADVANCE Act and Genesis Mission | Watch whether licensing timelines actually shorten |

| Korean policy | Three large reactors, one SMR, and 35.6% nuclear share by 2038 | Assess Team Korea supply-chain participation |

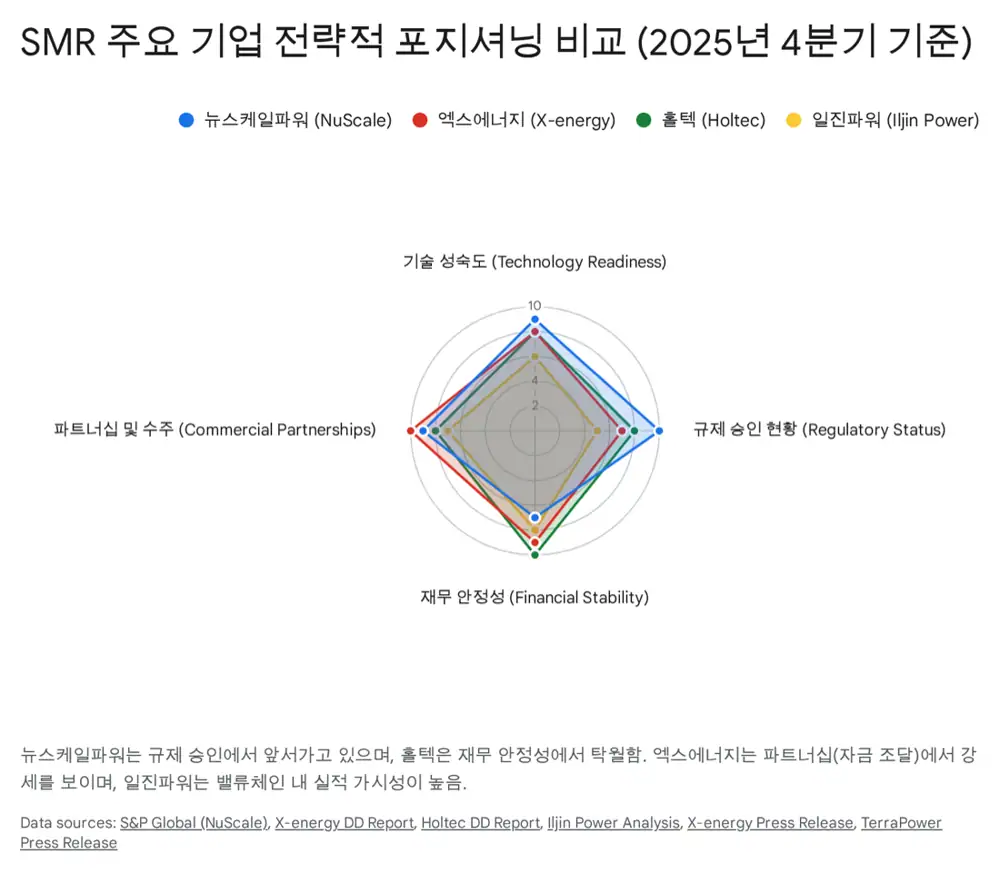

2. Company positioning

The source compares NuScale Power, X-energy, Holtec International, and Iljin Power across technology maturity, financial stability, regulatory risk, and partnerships. My read is that these names should not be treated as one homogeneous SMR basket; each has a different risk profile.

NuScale Power

Presented as the only SMR technology holder with NRC design certification. The ENTRA1-led TVA 6GW collaboration and Romania RoPower FEED 2 improve commercialization visibility.

X-energy

Built around the 80MWe Xe-100 HTGR and TRISO-X fuel integration. It has secured more than $1.2 billion of cumulative private capital from Amazon and Jane Street-led rounds.

Holtec International

Dry-cask spent-fuel storage and decommissioning cash flow support SMR-300 development. Mission 2030 at Palisades is the key speed advantage.

Iljin Power

It is extending from power-plant maintenance into i-SMR test equipment and tritium-related nuclear-fusion supply chains.

NuScale Power: the regulatory first mover

NuScale is described as the only SMR technology holder with NRC Standard Design Approval. Its 77MWe NuScale Power Module uses passive safety systems that can cool the reactor without operator intervention during loss of power, tying the technology to the safety demands of data-center-adjacent power.

Official fact: As of the end of Q3 2025, cash and equivalents were about $753.8 million, up from $489.9 million in the prior quarter. Roughly $475.2 million of ATM equity issuance helped fund liquidity. Third-quarter revenue was $8.24 million, EPS was -$1.85, and $128.5 million of ENTRA1 partnership milestone costs were reflected.

The TVA collaboration is a 6GW SMR deployment agreement through ENTRA1 with the Tennessee Valley Authority. The source describes this as roughly 72 NuScale power modules and the largest SMR project in U.S. history, with the first plant expected to deliver power around 2030. Romania's RoPower project, which would convert the Doicesti coal plant to SMR generation, is in FEED Phase 2 and targets an FID in 2026-2027.

Interpretation: NuScale's strengths are regulatory first-mover status and utility-scale demand such as TVA. The offsetting risks are cost inflation, as shown by the cancelled UAMPS project, and share overhang from Fluor's stake-sale agreement.

X-energy: HTGR backed by Big Tech capital

X-energy is developing the 80MWe Xe-100 high-temperature gas reactor. Using helium coolant, it can produce heat above 750°C, which expands the market beyond electricity into hydrogen production and petrochemical process heat. Its TRISO-X subsidiary internalizes TRISO fuel manufacturing, which the source treats as an important differentiator.

Official fact: X-energy raised about $700 million in a Jane Street-led Series D and, including Amazon's earlier $500 million Series C-1 round, has secured more than $1.2 billion of cumulative private capital. Amazon, with Energy Northwest in Washington state, is pursuing an initial 320MW and up to 960MW of Xe-100 deployment. Source links: Amazon investment release, X-energy Series D release, and ANS Amazon update.

Korea is central to the execution plan. Doosan Enerbility is a main-equipment manufacturing partner and DL E&C is an EPC partner. The source frames this Team Korea strategy as a way to offset the weakened manufacturing and supply-chain base of Western nuclear companies. Related link: X-energy, Amazon, KHNP, Doosan partnership release.

Holtec and Iljin Power: cash flow and the Korean value chain

Holtec is presented as different from many SMR start-ups because it already generates cash from dry-cask spent-fuel storage and decommissioning. The shift from SMR-160 to a forced-circulation PWR-based SMR-300 is read as a pragmatic choice favoring licensing familiarity and existing component leverage.

Official fact: Holtec received approval to return the Palisades nuclear plant in Michigan to operations and is pursuing Mission 2030 to add two SMR-300 units at the site. The source argues that starting with land, grid access, cooling water, and local acceptance already addressed gives it a speed advantage versus greenfield projects. Links: Holtec Mission 2030 and Palisades operations status.

Iljin Power is extending from routine maintenance for Korean standard nuclear plants and thermal plants into SMR equipment and fusion-tritium supply chains. For Q3 2025 cumulative results, revenue was KRW 193.1 billion, up 22.8% year over year, and operating profit was KRW 10.3 billion, up 88.1%. The source also cites a KRW 16.32 billion order for KAERI's innovative SMR integrated effects test facility and a KRW 23.8 billion TRF equipment contract for Romania's Cernavoda nuclear plant.

3. Competitors and risks: SMR remains an industry to prove

The competitive section separately covers TerraPower and Oklo. TerraPower, founded by Bill Gates, is developing the Natrium sodium-cooled fast reactor at Kemmerer, Wyoming. Completion of the NRC final safety evaluation for the construction permit review ahead of schedule in December 2025 is positive, but HALEU fuel supply remains the major bottleneck. Links: NRC PDF, ANS TerraPower article, and NucNet article.

Oklo, chaired by Sam Altman, is developing the Aurora micro fast reactor. It received DOE safety-design approval for a fuel fabrication facility and selected Kiewit as lead constructor for the Idaho National Laboratory site. The source still flags regulatory work before its 2027-2028 commercialization goal, plus short-seller and valuation controversy. Links: Oklo NRC readiness assessment, Oklo Kiewit selection, and Investing.com article.

| Risk | Source detail | Relative impact |

|---|---|---|

| HALEU supply | Gen IV reactors need 5-20% enriched HALEU while commercial supply is described as heavily dependent on Russia's TENEX | Pressure on Xe-100 and Natrium; potential relative benefit for LEU users NuScale and Holtec |

| FOAK cost | First-of-a-kind builds can face design changes, supply disruptions, and regulatory response costs | Check whether contracts are fixed-price and who bears overruns |

| Overhang | NuScale's Fluor stake-sale agreement and future stake sales around private or restructured names | Equity supply risk |

| Licensing | Policy support does not automatically shorten real review timelines | Wider gap between regulatory first movers and laggards |

4. Investment strategy: prioritize execution over technology labels

The source concludes that SMR has moved from a sector of expectations into a sector of actual orders and construction. I agree that the investment framework should emphasize execution, capital capacity, and confirmed offtakers over reactor novelty alone.

Aggressive investors

NuScale Power and X-energy are the candidates. NuScale's TVA project is the key trigger, while X-energy combines Amazon-backed data-center power opportunity with HALEU supply risk.

Value and growth investors

Iljin Power is framed as a company with a core business supporting downside while SMR and fusion momentum add upside. 2025 earnings strength and pro-nuclear policy support re-rating potential.

Strategic investors

Holtec is presented as an IPO-time candidate with infrastructure-like characteristics from spent-fuel management and decommissioning cash cows.

The monitoring list is straightforward: actual Big Tech PPAs, licensing, construction start, fuel loading, fixed-price contract terms, and HALEU supply-chain expansion. The source's proposed hedge is to avoid single-name concentration and diversify across light-water versus non-light-water designs and U.S. versus Korean supply chains.

Sources

- 네이버 블로그 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224129693403

- SMR 기업 듀 딜리전스 보고서: https://drive.google.com/open?id=1PMP6hZWdFzBhaUAaCn83e8D7ebk4hJYKjCwiJHlAhzw

- Amazon Invests in X-energy: https://x-energy.com/media/news-releases/amazon-invests-in-x-energy-to-support-advanced-small-modular-nuclear-reactors-and-expand-carbon-free-power

- Google and Kairos Power Partner: https://kairospower.com/external_updates/google-and-kairos-power-partner-to-deploy-500-mw-of-clean-electricity-generation/

- Microsoft, Constellation Energy restart Three Mile Island nuclear reactor: https://www.foxnews.com/media/three-mile-island-nuclear-plant-makes-dramatic-comeback-1b-federal-backing-ai-power

- X-energy $700 Million Series D: https://x-energy.com/media/news-releases/x-energy-closes-oversubscribed-700-million-series-d-financing-round-to-continue-expansion-to-meet-global-energy-demand

- 홀텍인터내셔널 SMR 투자 심사 보고서: https://drive.google.com/open?id=1sg8J3xM5s1LMGW_vaE7WAw4I-aXf-rR87fBDbMsok6k

- Holtec Mission 2030: https://holtecinternational.com/hh-40-05/

- 일진파워 기업 분석 프롬프트: https://drive.google.com/open?id=1Br8YXRtO8LYCXRzmUJa9PpH5pt6MrZgXsWRUM4scIEo

- Constellation Crane Clean Energy Center: https://www.constellationenergy.com/newsroom/2024/Constellation-to-Launch-Crane-Clean-Energy-Center-Restoring-Jobs-and-Carbon-Free-Power-to-The-Grid.html

- NRC Kemmerer safety review PDF: https://www.nrc.gov/sites/default/files/cdn/doc-collection-news/2025/25-063.pdf

- ANS Amazon update with X-energy: https://www.ans.org/news/2025-10-20/article-7473/amazon-provides-update-on-its-washington-project-with-xenergy/

- X-energy, Amazon, KHNP, Doosan partnership: https://x-energy.com/media/news-releases/x-energy-amazon-korea-hydro-amp-nuclear-power-and-doosan-enerbility-announce-partnership-to-scale-advanced-nuclear-energy-for-ai-infrastructure

- Holtec Palisades operations status: https://holtecinternational.com/hh-40-18/

- ANS TerraPower Kemmerer review: https://www.ans.org/news/2025-12-03/article-7590/nrc-completes-safety-review-for-terrapowers-kemmerer-project/

- NucNet TerraPower construction work: https://www.nucnet.org/news/terrapower-to-begin-preparatory-construction-work-for-wyoming-nuclear-plant-in-coming-months-3-2-2024

- Oklo NRC readiness assessment: https://oklo.com/newsroom/news-details/2025/Oklo-Advances-Licensing-with-Completion-of-NRC-Readiness-Assessment/default.aspx

- Oklo selects Kiewit: https://oklo.com/newsroom/news-details/2025/Oklo-Selects-Kiewit-as-the-Lead-Constructor-for-First-Aurora-Powerhouse-in-Idaho/default.aspx

- Investing.com Oklo fair value model: https://www.investing.com/news/investment-ideas/investingpros-fair-value-model-predicted-oklos-42-stock-decline-93CH-4423312

- SMR 원자력 발전 조사 개요: https://drive.google.com/open?id=1-d597ognobkmQtUJ0XUkeBQunlluUncget_1aG-pUFw