DEEP RESEARCH · TERRAPOWER AND SMR

TerraPower-Centered SMR Analysis: AI Power Demand and the Advanced Nuclear Value Chain

A comparison of TerraPower, NuScale, X-energy, and Holtec across technology, capital, licensing, and Korean supply chains

0. Bottom line first

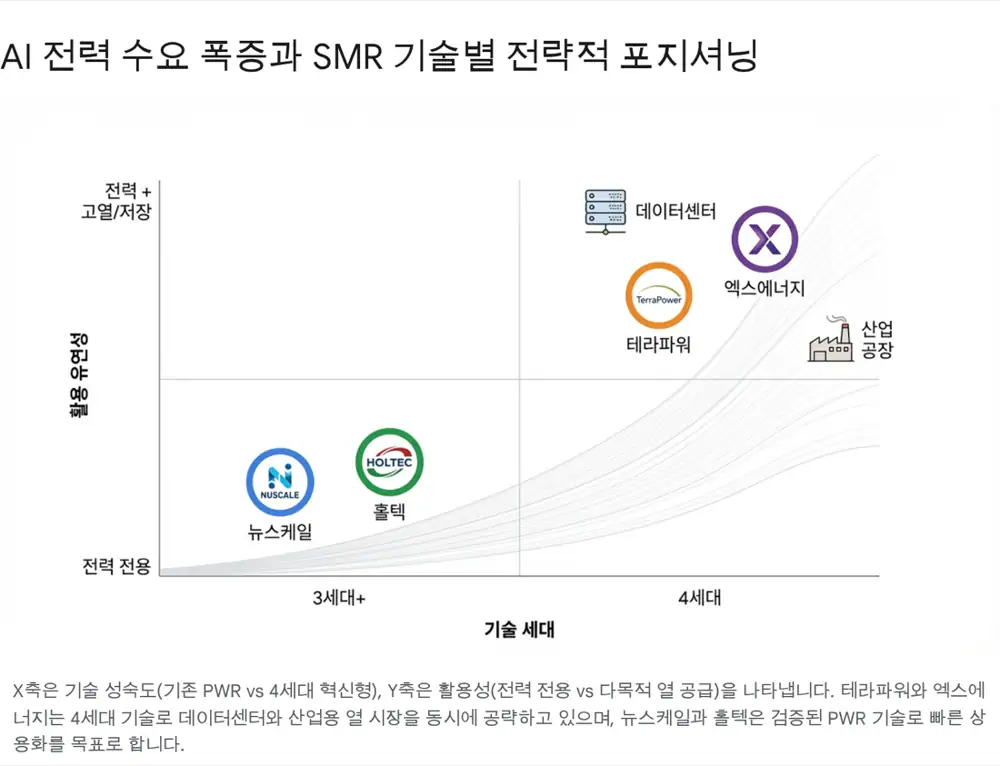

SMR is being re-rated from a long-duration energy theme into a technology-infrastructure theme for AI data-center power. My read is that TerraPower is the flexible baseload complement to renewables, X-energy owns industrial heat optionality, Holtec has brownfield realism and cash flow, and NuScale has public-market and regulatory-first-mover premium.

Natrium 345MWe + storage

A sodium-cooled fast reactor paired with molten-salt storage, able to provide 500MWe for 5.5 hours when needed.

Public SMR leader

NRC design approval and NYSE listing are advantages, but project economics must be rebuilt after UAMPS cancellation.

HTGR industrial heat

Xe-100 targets not only power but 565-750°C steam for petrochemical and industrial heat markets.

Cash-flow funded development

Dry-cask spent-fuel storage cash flow and the Palisades brownfield strategy are the differentiators.

1. Macro: AI power demand and nuclear renaissance

Official fact: The source frames late 2025 energy markets as a structural inflection where net-zero requirements and AI data-center power demand meet. It cites forecasts that data-center power consumption could more than double by 2030.

Official fact: The source says training and inference for generative AI models can use more than 10 times the power of a traditional Google search. Microsoft, Amazon, and Google are pursuing 24/7 carbon-free energy through SMR PPAs or equity investments.

Interpretation: The market is recognizing that intermittent solar and wind alone cannot carry around-the-clock data-center loads. Nuclear is re-emerging as carbon-free baseload, with IRA credits and technology-neutral clean-power support improving LCOE.

2. Supply chain: HALEU and Korean manufacturing dependence

Official fact: The source says HALEU fuel for fourth-generation reactors used by TerraPower and X-energy has been commercially dominated by Russia's Tenex. After the Ukraine war, the U.S. has been pushing diversification through Centrus Energy and others.

Official fact: The source argues that Western nuclear manufacturing capacity weakened during decades of stagnation, while Korea's Doosan Enerbility, Hyundai E&C, and HD Hyundai Heavy Industries maintained manufacturing and construction capability through domestic builds and the UAE Barakah export project.

Interpretation: For SMR investors, Korean companies are not just theme exposure. They can become the global SMR foundry, because equipment slots and EPC execution are commercialization bottlenecks.

3. TerraPower: Natrium technology moat and demonstration progress

Official fact: TerraPower is a nuclear innovation company founded in 2006 by Bill Gates and based in Bellevue, Washington. It initially focused on traveling-wave reactors, then shifted to the sodium-cooled fast reactor Natrium after U.S.-China trade tensions blocked the China demonstration path.

Official fact: CEO Chris Levesque is a former U.S. Navy nuclear submarine officer with large nuclear-project management experience at Westinghouse and Areva. Bill Gates serves as chairman and provides technology vision, policy connectivity, and capital-market influence.

Official fact: Natrium is a 345MWe sodium-cooled fast reactor combined with molten-salt energy storage. It can boost output to 500MWe for 5.5 hours. Liquid sodium has a boiling point around 880°C, allowing low-pressure operation and passive-safety design goals.

Official fact: The first demonstration plant is being built at the retired coal site in Kemmerer, Wyoming. In June 2024, TerraPower started non-nuclear construction before NRC construction-permit approval, and in August 2025 began work on the Kemmerer Training Center.

- In March 2024, TerraPower submitted its Part 50 construction permit application.

- In October 2025, the NRC environmental impact statement concluded no adverse environmental impact, according to the source.

- In December 2025, the NRC completed the safety review one month ahead of schedule, as summarized in the source.

- The current schedule points to fuel loading in 2030 and commercial operation in 2031.

4. TerraPower capital and Team Korea linkage

Official fact: TerraPower raised USD 650 million, about KRW 900 billion, in a Series D round closed in June 2025. The source says cumulative funding is about USD 1.7 billion, or roughly KRW 2.3 trillion.

Official fact: Investors include Bill Gates, NVIDIA's NVentures, SK Group, and HD Hyundai. SK invested USD 250 million in 2022 as a co-lead investor and is described as a strategic partner with Asian business rights and a board seat.

Official fact: HD Hyundai Heavy Industries is tied to reactor-vessel manufacturing, Doosan Enerbility to steam generators and heat exchangers, Bechtel to EPC, and GE Hitachi to technology partnership. The source says DOE ARDP matching support of about USD 2 billion reduces near-term IPO pressure.

Interpretation: NVentures' participation supports re-rating TerraPower from an energy company into an AI-infrastructure power supplier. The source estimates pre-money valuation around USD 3-4 billion, while noting no official valuation disclosure.

5. Peer due diligence: NuScale, X-energy, Holtec

| Company | Technology | Key facts | Main risk |

|---|---|---|---|

| NuScale Power | VOYGR PWR-based SMR | SPAC listed in 2022; NRC 50MWe design approval in 2020; 77MWe uprated design approval in May 2025. About USD 753M cash equivalents at Q3 2025. | Project economics and customer execution after the 2023 UAMPS cancellation. |

| X-energy | Xe-100, 80MWe HTGR | Helium cooled, 565-750°C steam. Dow Seadrift CPA in progress. USD 700M financing in November 2025 with Jane Street and Amazon participation. | HALEU supply and first-of-a-kind construction cost. |

| Holtec | SMR-300 PWR | Cash cow in dry-cask spent-fuel storage. Two SMRs planned at Palisades. USD 1.52B DOE loan guarantee and Hyundai E&C partnership. | Palisades restart and NRC review speed. |

Official fact: NuScale is pursuing a data-center pivot through Standard Power and Entra1, including 24 modules and about 2GW of potential capacity. The Romania Doicesti project is described as FEED Phase 2, expected to finish by end-2025.

Official fact: X-energy is working with Amazon toward 5GW of SMR deployment by 2039. Doosan Enerbility has reserved equipment for 16 units, while DL E&C participates as EPC and equity partner.

Official fact: Holtec CEO Kris Singh has discussed a late-2025 or early-2026 IPO, and the source says the market estimates valuation above USD 10 billion. The source table says Holtec generates more than USD 500 million in annual profit.

6. Four-company comparison

| Category | TerraPower | NuScale | X-energy | Holtec |

|---|---|---|---|---|

| Reactor type | SFR + molten-salt storage | PWR natural circulation | HTGR, TRISO fuel | PWR forced circulation |

| Output | 345MWe, 500MWe with storage | 77MWe/module, 462MWe for six | 80MWe/module, 320MWe for four | 300MWe single/combined |

| Use case | Grid stability, AI data centers | Power generation, AI data centers | Industrial heat, Dow, Amazon | Baseload, retired nuclear sites |

| NRC status | CPA review, safety review completed Dec. 2025 | SDA for 50MWe and 77MWe | CPA review in progress | CPA planned by end-2025 |

| Korean partners | SK, HD Hyundai, Doosan Enerbility | Doosan Enerbility, Samsung C&T, GS Energy | Doosan Enerbility, DL E&C | Hyundai E&C, K-SURE |

| Main risk | HALEU, liquid sodium complexity | Project economics | HALEU, first-unit cost | Regulatory speed, Palisades restart |

7. Investment-strategy view

TerraPower

Direct access is difficult because it is private, so supply-chain exposure through SK, HD Hyundai, and Doosan Enerbility is more practical.

X-energy

Industrial heat and Amazon demand are strengths, with Doosan Enerbility and DL E&C as key value-chain names.

Holtec

It is the most financially stable candidate; the IPO and Hyundai E&C order momentum should be watched together.

NuScale

Public-market and regulatory-approval premiums remain, but data-center orders must turn into actual construction.

SMR investing is a long-duration game. I would track CPA approvals, construction starts, HALEU supply, and equipment-slot reservations rather than short-term headlines. The favorable angle for Korean investors is that Korean companies control important manufacturing and EPC bottlenecks in the global SMR value chain.

Sources

- Naver Blog original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224129679514

- Meritz Securities 2026 utilities/construction outlook PDF: https://drive.google.com/open?id=131SxldTl6uVTn7P2TgR-eWvHNX9oV2qf

- SMR nuclear power research overview: https://drive.google.com/open?id=1-d597ognobkmQtUJ0XUkeBQunlluUncget_1aG-pUFw

- TerraPower announces $650 million fundraise: https://www.terrapower.com/terrapower-announces-650-million-fundraise

- TerraPower begins construction in Wyoming: https://www.terrapower.com/terrapower-begins-construction-in-wyoming

- Nasdaq - NuScale 6GW push: https://www.nasdaq.com/articles/nuscale-powers-6gw-push-advances-2030-target-achievable

- American Nuclear Society - X-energy raises $700M: https://www.ans.org/news/article-7581/xenergy-raises-700m-in-latest-funding-round/

- X-energy $700M Series C-1 financing: https://x-energy.com/media/news-releases/x-energy-closes-upsized-700-million-series-c-1-financing-round-to-accelerate-the-development-of-advanced-small-modular-nuclear-technology

- Holtec International SMR investment memo: https://drive.google.com/open?id=1sg8J3xM5s1LMGW_vaE7WAw4I-aXf-rR87fBDbMsok6k

- DOE Holtec Palisades: https://www.energy.gov/edf/holtec-palisades

- SMR company due diligence report: https://drive.google.com/open?id=1PMP6hZWdFzBhaUAaCn83e8D7ebk4hJYKjCwiJHlAhzw

- DOE HALEU distribution to advanced reactor developers: https://www.energy.gov/articles/us-department-energy-distribute-first-amounts-haleu-us-advanced-reactor-developers

- TerraPower about: https://www.terrapower.com/about/

- TerraPower - Wikipedia: https://en.wikipedia.org/wiki/TerraPower

- Chris Levesque - Atlantic Council: https://www.atlanticcouncil.org/events/flagship-event/global-energy-forum/chris-levesque/

- Chris Levesque congressional testimony PDF: https://www.congress.gov/116/meeting/house/110640/witnesses/HHRG-116-IF03-Wstate-LevesqueC-20200303.pdf

- Bill Gates notes on Wyoming TerraPower groundbreaking: https://www.gatesnotes.com/work/accelerate-energy-innovation/reader/wyoming-terrapower-groundbreaking

- TerraPower Natrium: https://www.terrapower.com/natrium/

- TerraPower Natrium technology PDF: https://www.terrapower.com/downloads/Natrium_Technology.pdf

- TerraPower process heat one-pager PDF: https://www.terrapower.com/downloads/Process-Heat-one-pager.pdf

- TerraPower Kemmerer Training Center: https://www.terrapower.com/terrapower-begins-construction-on-state-of-the-art-kemmerer-training-center

- ANS - NRC completes safety review for Kemmerer: https://www.ans.org/news/2025-12-03/article-7590/nrc-completes-safety-review-for-terrapowers-kemmerer-project/

- TerraPower Natrium project environmental impact statement: https://www.terrapower.com/natrium-project-receives-first-nrc-issued-environmental-impact-statement-for-a-commercial-advanced-nuclear-power-plant

- NRC safety review press release PDF: https://www.nrc.gov/sites/default/files/cdn/doc-collection-news/2025/25-063.pdf

- IPO Club TerraPower: https://www.ipo.club/deals/terrapower

- World Nuclear News - SK invests in TerraPower: https://www.world-nuclear-news.org/Articles/South-Koreas-SK-Group-invests-in-TerraPower

- SK and TerraPower strategic partnership: https://eng.sk.com/news/sk-group-and-terrapower-strengthen-strategic-partnership-to-commercialize-advanced-nuclear-energy-technology

- World Nuclear News - HD Hyundai TerraPower SMR: https://world-nuclear-news.org/articles/hd-hyundai-to-help-commercialise-terrapower-smr

- Motley Fool - how to invest in TerraPower stock: https://www.fool.com/investing/how-to-invest/stocks/how-to-invest-in-terrapower-stock/

- StockAnalysis - invest in TerraPower: https://stockanalysis.com/article/invest-in-terrapower-stock/

- Korea Times - SK TerraPower Natrium partnership: https://www.koreatimes.co.kr/business/companies/20250825/sk-deepens-partnership-with-terrapower-to-advance-natrium-smrs

- PR Newswire - HD Hyundai Chung Kisun meets TerraPower: https://www.prnewswire.com/news-releases/hd-hyundai-executive-vice-chairman-chung-kisun-meets-terrapower-including-chairman-bill-gates-to-discuss-nuclear-supply-chain-cooperation-302536514.html

- Bechtel - America next nuclear plant begins construction: https://www.bechtel.com/press-releases/americas-next-nuclear-power-plant-begins-construction/

- DOE - NRC approves NuScale uprated design: https://www.energy.gov/ne/articles/nrc-approves-nuscale-powers-uprated-small-modular-reactor-design

- NuScale 77 MWe standard design approval: https://www.nuscalepower.com/press-releases/2025/nuscale-powers-small-modular-reactor-smr-achieves-standard-design-approval-from-us-nuclear-regulatory-commission-for-77-mwe

- NuScale and RoPower FEED phase 1: https://www.nuscalepower.com/press-releases/2023/nuscale-and-ropower-announce-signing-of-the-contract-for-phase-1-engineering-and-design-work

- NuScale supports ENTRA1 $25B agreement: https://www.nuscalepower.com/press-releases/2025/nuscale-power-proudly-supports-entra1-energys-25-billion-agreement-to-deploy-large-scale-power-infrastructure-assets-across-the-united-states

- NuScale Q3 2025 results: https://www.nuscalepower.com/press-releases/2025/nuscale-power-reports-third-quarter-2025-results

- MarketBeat NuScale stock chart: https://www.marketbeat.com/stocks/NYSE/SMR/chart/

- X-energy news releases: https://x-energy.com/media/news-releases

- Holtec Tier 1 First Mover Award: https://holtecinternational.com/hh-40-24/

- Holtec SMR products: https://holtecinternational.com/products-and-services/smr/

- Capital.com Holtec IPO guide: https://capital.com/en-int/learn/ipo/holtec-international-ipo

- Futunn/Barrons - Holtec IPO news: https://news.futunn.com/en/post/58446110/nuclear-power-s-biggest-ipo-in-years-is-on-the

- Crunchbase - TerraPower raises $650M from Nvidia VC arm: https://news.crunchbase.com/venture/nuclear-terrapower-raise-nvda-gates/

- X-energy $700M Series D financing: https://x-energy.com/media/news-releases/x-energy-closes-oversubscribed-700-million-series-d-financing-round-to-continue-expansion-to-meet-global-energy-demand

- Robinhood NuScale stock quote: https://robinhood.com/us/en/stocks/SMR/