DEEP RESEARCH · POSCO Future M (003670.KS)

POSCO Future M (003670) Deep Dive: Opening Act of a Structural Turnaround & the Value-Chain Hegemony Battle

Past the EV chasm into a "materials-security" fortress — at the intersection of 3Q 2025 swing-to-profit and the non-China anode super-cycle

0. Bottom line first

POSCO Future M sits at the crossroad of "near-term EV chasm pain" and "long-term value-chain dominance." 3Q 2025 revenue of KRW 874.8B (+32.4% QoQ), operating profit of KRW 66.7B (returning from BEP), and OPM of 7.6% are not pure base-effects — they reflect product-mix upgrade (N86 / NCA) + Gwangyang utilization lift + inventory-valuation reversal. The US's pending 93.5% tariff on Chinese graphite anodes is a powerful trigger for POSCO Future M — the only non-Chinese mass-producer of anodes. View: BUY.

Official fact: 3Q 2025 consolidated revenue KRW 874.8B (+32.4% QoQ, -5.2% YoY); operating profit KRW 66.7B (2Q: KRW 0.8B → +8,525% QoQ; up sharply from KRW 1.4B in 3Q 2024); OPM 7.6% (+7.5pp QoQ). Energy-materials revenue rose from KRW 315.4B to KRW 533.4B (+69% QoQ). Cash & equivalents KRW 836.6B (+KRW 426.9B QoQ); total liabilities KRW 4.65T (-KRW 235.9B QoQ); total debt KRW 3.82T (-KRW 196.8B QoQ); PP&E KRW 5.90T (+KRW 253.5B QoQ). POSCO Holdings holds 59.7%.

Interpretation: Of the KRW 66.7B operating profit, an estimated ~KRW 32B (~48%) is inventory-valuation reversal — but excluding that, recurring OP of ~KRW 34B (OPM ~3.9%) confirms BEP has stabilized. Revenue +32% with inventory only +2.3% means turnover sharply improved. Combine utilization recovery + US graphite tariff + POSCO group raw-material integration, and a 2026+ re-rating becomes natural.

1. 3Q 2025 financials — the quality of the turnaround

1.1 P&L — operating leverage returns

| Item | 3Q 2025 | 2Q 2025 | QoQ | 3Q 2024 | YoY |

|---|---|---|---|---|---|

| Revenue | KRW 874.8B | KRW 660.9B | +32.4% | — | -5.2% |

| Operating profit | KRW 66.7B | KRW 0.8B | +8,525% | KRW 1.4B | Sharp swing |

| OPM | 7.6% | 0.1% | +7.5pp | — | Improving |

| Energy materials revenue | KRW 533.4B | KRW 315.4B | +69% | — | — |

Decomposing the profit lift produces three drivers:

- Volume recovery + mix upgrade (Q · Mix): revenue lift comes from volume more than price. Strong N86 cathode (using Gwangyang precursor) and Samsung SDI–bound NCA improved the high-nickel mix.

- Inventory-valuation reversal: rebounding metal (Li, Ni) prices plus the burn-down of high-cost inventory drove ~KRW 32B of reversal — perhaps 48% of OP. Even excluding it, recurring OP ~KRW 34B (OPM ~3.9%) confirms BEP has stabilized.

- Operating leverage: Gwangyang utilization lift dilutes unit fixed costs (depreciation, labor) — the strongest turnaround signal in this capex-heavy industry.

1.2 Balance sheet & cash flow — investment / harvest balance

- Liquidity: cash & equivalents KRW 836.6B (+KRW 426.9B QoQ) — equity raise + improving OCF + paced CAPEX.

- Debt: total liabilities KRW 4.65T (-KRW 235.9B), total debt KRW 3.82T (-KRW 196.8B) — easing financial-expense burden under high rates.

- Inventory turnover: revenue +32.4% while inventory only +2.3% (KRW 847B) — turnover ~3.6x, sharply better than 2Q; bad-inventory burn complete.

- Investing activities: PP&E KRW 5.90T (+KRW 253.5B). Gwangyang/Pohang capacity expansion continues but pace has slowed vs. history — CAPEX consciously paced to chasm conditions.

2. Top-3 customer risk & response

2.1 LG Energy Solution & GM (Ultium Cells) — the shock of pacing

Ultium Cells (GM-LGES JV) is the single biggest demand source for the cathode business. GM's EV-production target cut + the Quebec Ultium CAM start-up delay to 2H 2026 is a clear near-term risk.

- Risk: Slow ramp at Ultium 1 / 2 caps the Gwangyang utilization recovery. The Ultium CAM phase-2 hold pushes out NA revenue → fixed-cost burden ↑ and payback period ↑.

- Paradoxical opportunity: The delay defers ramp-up cost. When GM eventually re-ramps after the destocking and new-model refresh, POSCO Future M's verified supply chain becomes more, not less, valuable. LGES's 3Q call hint at scale-up of NA ESS battery production opens a new lane.

2.2 Samsung SDI — NCA expansion as the masterstroke

The 2023–2032 10-year KRW 40T supply contract pivoted the portfolio from NCM (LGES-bound) into NCA (SDI-bound). SDI's conservative capex stance + strong premium-EV traction (BMW, Audi) limits its utilization decline.

The StarPlus Energy JV with Stellantis starts production in 2026 → the second quantum leap. SDI's expansion of LFP / NCA SBB (Samsung Battery Box) for the NA ESS market further diversifies the cathode demand channel.

2.3 Ford & SK On — the epicenter of uncertainty

Noise around SK On–Ford and Ford's EV-strategy reset (big SUVs first, hybrids parallel) is an indirect risk. POSCO Future M supplies Ford via SK On — Ford volumes and SK On yields are linked to its P&L. SK On's upcoming Hyundai Motor Group NA JV could partially offset Ford exposure.

Pacing shock

Ultium CAM start-up pushed to 2H 2026. Utilization cap vs. ESS expansion both alive.

NCA masterstroke

10-year KRW 40T contract. StarPlus Energy + SBB → 2nd quantum leap from 2026.

Strategy-reset risk

EV-strategy reset, some LGES order cancellation. Partially offset by Hyundai–SK On JV.

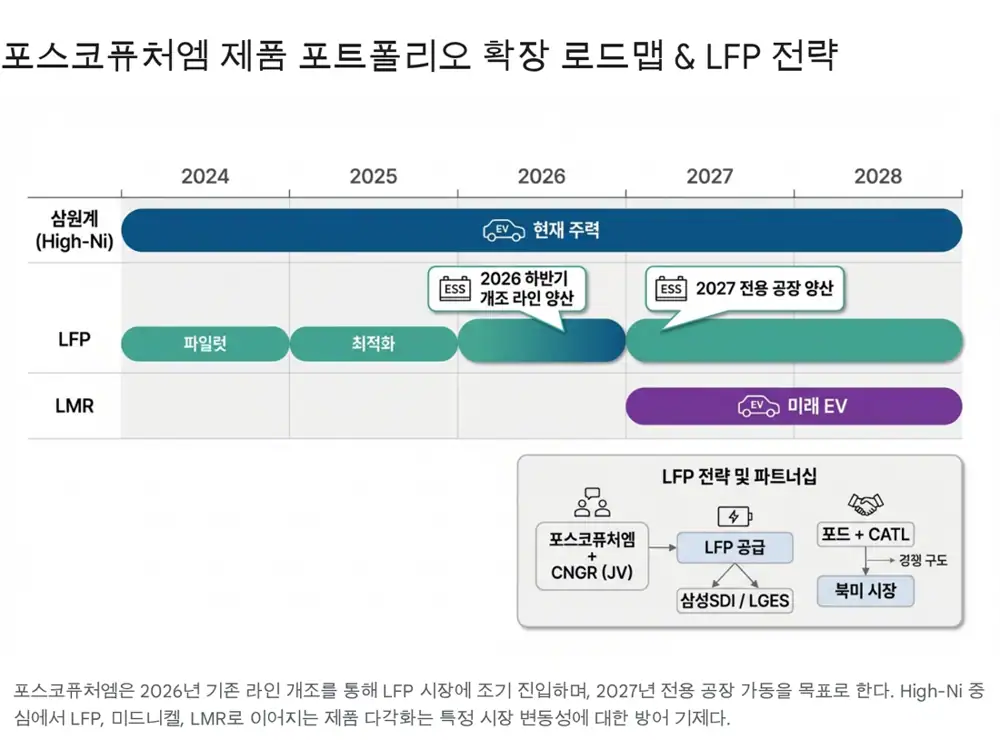

3. LFP market shifts & opportunity — surviving the Red Ocean

3.1 Ford–CATL implications

Ford running its Michigan LFP plant as a wholly-owned subsidiary while CATL only licenses technology is a sophisticated workaround for the IRA's FEOC rule. If China's cost competitiveness + proven LFP combines with US capital, Korean materials makers risk eroding their "non-China premium."

3.2 POSCO Future M's LFP response — speed + raw-material edge

- Line conversion for early entry: Portion of the Pohang NCM line will be converted to LFP → supply from 2H 2026. A timely asset-light tactic vs. 2–3 years and full cost of a greenfield.

- CNGR strategic alliance: JV "CNP Sinsojae Technology" with China's CNGR and its Korean affiliate FINO; 50,000 tonnes/yr LFP plant in Pohang Yeongil Bay industrial complex — a realistic way to close the tech gap quickly.

- FEOC risk: Chinese-capital share above 25% would forfeit IRA benefits. POSCO Future M is running a Plan B — adjust equity to secure management control, or prioritize markets less reliant on IRA subsidies (ESS, Europe).

- ESS first: The booming North American ESS market (AI data centers etc.) has shorter qualification than EV and a strong preference for LFP. POSCO Future M would enjoy a near-monopoly position as a "non-Chinese LFP supplier."

3.3 Next-gen materials — LMR & high-voltage mid-nickel

To counter LFP's price war, POSCO Future M has completed development of LMR (Lithium Manganese Rich) cathodes and is securing mass-production tech. Lower cobalt + higher manganese reduces cost — a strong LFP counter in entry-level EV. High-voltage mid-nickel cathodes further strengthen mass-market competitiveness.

4. Asset efficiency — crossing the Valley of Death

4.1 The utilization paradox and operating leverage

Sejong anode plant utilization is estimated to have fallen from 67% in 2022 to ~30% in 1H 2024 — the main margin culprit. Paradoxically, that low utilization implies high operating-leverage potential. Once revenue clears BEP, profit grows far faster than revenue.

Official fact: the planned US 93.5% tariff on Chinese graphite anodes phases in across 2025–2026. POSCO Future M is the only non-Chinese mass-producer of anodes.

Interpretation: When the tariff erases Chinese cost competitiveness, NA cell makers must diversify supply to POSCO Future M — a decisive trigger for Sejong utilization recovery.

4.2 CAPEX pacing & cash-flow defense

Holding Ultium CAM phase-2 and pushing back start-up may dent the growth narrative, but they protect FCF. Converting existing lines to LFP instead of building new ones is an "Asset-Light" tactic that minimizes CAPEX while defending ROIC.

5. Governance & subsidiary risk

5.1 POSCO Holdings support — vertical integration

Top shareholder POSCO Holdings (59.7%) is not just a controller but a raw-material partner. Lithium (Argentine brine, Australian mines), nickel, and graphite mining rights give POSCO Future M a vertical-integration edge EcoPro BM and L&F cannot replicate. This drives cost competitiveness and is decisive for IRA critical-mineral compliance. POSCO Holdings' participation in the recent rights issue confirms a financial backstop.

5.2 Subsidiary / JV risk

- Ultium CAM (Canada JV): wholly exposed to GM's EV volumes. The recent delay is the risk materializing — but also strengthens the GM alignment.

- FINO & CNP Sinsojae Technology (LFP JV): the project lives or dies by FEOC interpretation. If CNGR's Chinese-capital nature dominates the optics, NA entry may be blocked — requiring equity adjustment or workaround export paths.

- Overseas entities: Indonesia (tied to Hyundai-LGES JV), China (Zhejiang POSCO Huayou, etc.) — exposed to geopolitics, regulation, and Chinese domestic oversupply.

6. Conclusion & investment view

6.1 BUY — "Buy the Dip" remains valid

POSCO Future M is moving through industry and earnings troughs simultaneously. The 3Q 2025 swing to profit is not cost cutting — it is the start of a structural shift: mix upgrade (NCA) + customer diversification (Samsung SDI weight). Even with continued end-market chasm, three drivers —

- ESS-LFP portfolio diversification,

- collateral benefit from the China anode tariff,

- POSCO group's raw-material integration —

— should propel a 2026+ re-rating. Maintain a long-duration BUY.

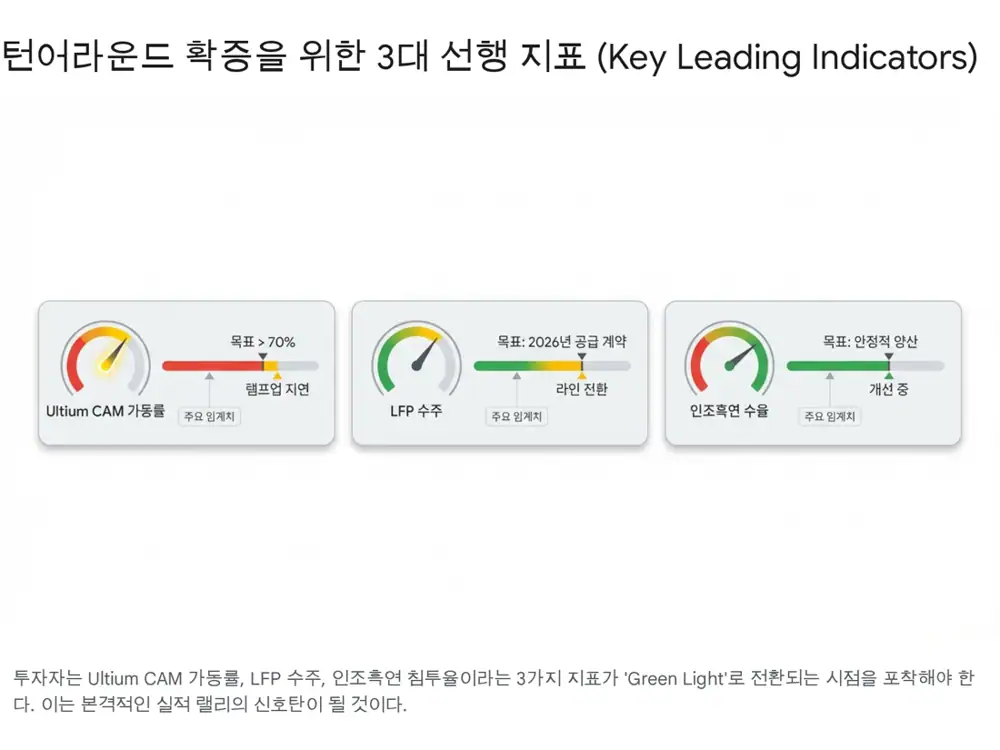

6.2 Three leading indicators to confirm turnaround

- ① Ultium CAM 1 utilization & shipment data: not the opening ceremony but how much commercial output actually flows into GM Ultium Cells = direct proxy for NA EV recovery.

- ② Large ESS LFP wins: moving beyond MOUs/development into a binding contract. A large NA contract is an immediate multiple-expansion catalyst.

- ③ Synthetic graphite anode yield & NA share: NA adoption as Chinese anodes are pushed out, plus initial yield stabilization and profit contribution — the final piece of margin recovery.

Sources

- Naver blog original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224129662459

- POSCO Future M to begin Quebec cathode plant operations in October 2026 — Korea Herald: article

- LGES cancels KRW 3.9T order with Freudenberg — Fidelity/Reuters: article

- US 93.5% tariff on Chinese anodes — Prime Economy: article

- US anti-dumping duties on Chinese graphite / POSCO Future M benefit — Newsis: article

- POSCO Future M 3Q 2025 Earnings Release: PDF

- 2026 secondary-battery annual outlook (Samsung SDI, POSCO Future M, EcoPro BM, etc.): Google Drive

- Samsung SDI & POSCO Future M boost investments — Chosunbiz: article

- GM and POSCO cancel battery material plant expansion — Battery-News: article

- LGES 3Q 2025 financial results — PR Newswire: press

- POSCO Chemical wins Samsung SDI KRW 40T cathode contract — Newsroom: press

- Samsung SDI US LFP-based deal expectations — Daum: article

- Stellantis-Samsung SDI Kokomo StarPlus Energy: press

- Samsung SDI 3Q 2025 results: press

- Samsung SDI KRW 2T+ ESS LFP deal: press

- The Ford-CATL Deal — The Diplomat: article

- Ford pushes ahead with Michigan EV battery plant — ev.com: article

- POSCO Future M ESS LFP plant — Etoday: article

- POSCO Future M JV with CNGR & FINO — Newsroom: press

- POSCO Future M & CNGR LFP cooperation — Battery-News: article

- POSCO Future M Pohang LFP plant — Chosunbiz: article

- FINO company analysis — Google Drive: material

- POSCO Future M LFP for ESS — Newsroom: press

- POSCO Future M LMR cathode — Newsroom: press

- POSCO Future M record W671B anode deal — Korea Herald: article

- POSCO Future M share analysis — Company Guide: site

- POSCO Future M positioning analysis — Google Drive: material

- POSCO Future M breaks with China in cathode supply chain — KED Global: article