DEEP RESEARCH · HLB

HLB: Integrated Company, Professional Management, and the Third FDA Attempt

A single investment narrative around the HLB Science merger, governance reset, rivoceranib CMC remediation, and LMR funding.

0. Bottom line first

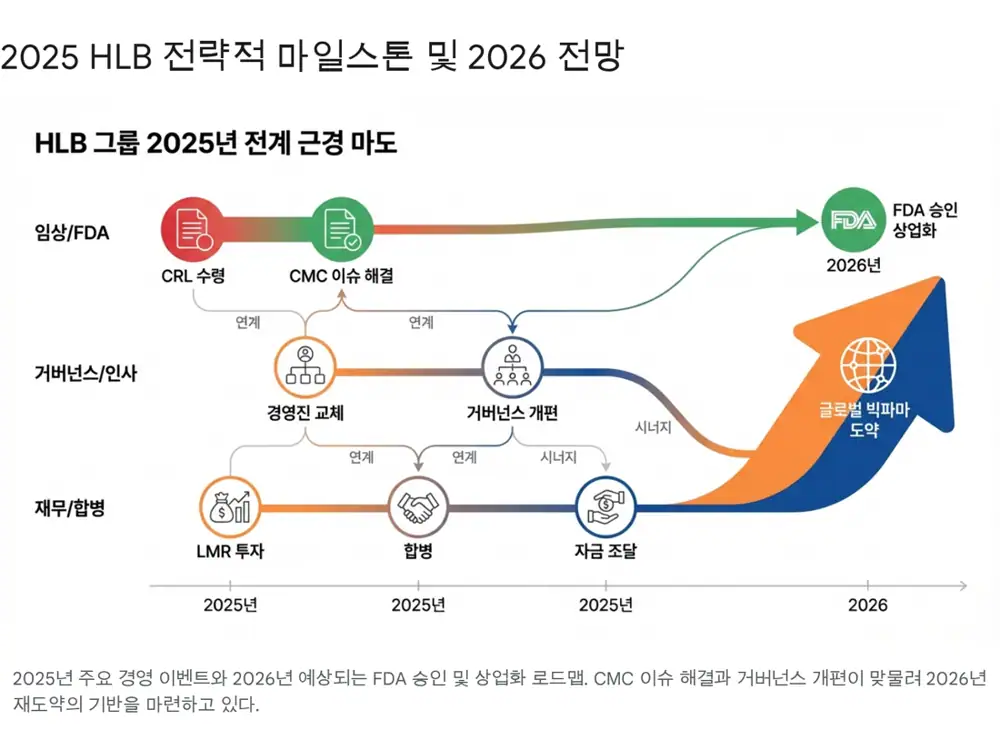

My conclusion is that HLB's late-2025 changes are not merely personnel and merger events. They are a redesign of the business structure before another FDA attempt. The HLB Science merger integrated pipeline and financial risk, while Jin Yang-gon's move to board chair and the professional management appointments distributed execution responsibility. The key variables are the planned January 2026 resubmission and the FDA decision expected around July.

1. Merger: combining R&D and finance into One HLB

Official fact: The source says that on December 31, 2025, HLB officially launched an integrated HLB by absorbing subsidiary HLB Science. The merger ratio is 1 : 0.0446318, and the source says a small-scale merger procedure was used because newly issued shares were about 0.6% of total shares.

The small-scale merger structure matters for speed and cash-flow control. Under Korean Commercial Act rules described in the source, if new shares issued by the surviving company after merger do not exceed 10% of total outstanding shares, board approval can replace a shareholders' meeting. HLB shareholders do not receive appraisal rights. HLB Science shareholders do, but the source expects the actual exercise scale to be limited.

| Category | Pre-merger HLB | Pre-merger HLB Science | Integrated HLB |

|---|---|---|---|

| Main field | Oncology, rivoceranib | Infectious disease, sepsis, degenerative brain disease | Oncology + CNS + Infectious Disease |

| Clinical stage | NDA preparation, near commercialization | Phase 1, preclinical | Full-cycle pipeline |

| Financial position | Can raise large capital, has liquidity | Capital impairment concerns, funding difficulty | Financial stability and investment efficiency |

| Organizational efficiency | Duplicate admin functions | Duplicate admin functions | Shared functions and fixed-cost reduction |

Interpretation: HLB Science's DD-S052P and DD-A279 provide options to reduce oncology concentration. Combined with HLB's global phase 3, NDA, and regulatory affairs experience, early-stage pipelines gain clinical and approval capability.

2. Portfolio: beyond oncology into infection and neurology

Core first-line liver cancer asset

The pipeline representing HLB's global commercialization possibility and the center of the FDA resubmission.

Sepsis and gram-negative bacteria therapy

The source describes it as a drug with a dual mechanism of bacterial killing and endotoxin neutralization, with phase 1 safety demonstrated.

Alzheimer's therapy

Presented as a non-oncology pipeline targeting brain endotoxin and neuroinflammation.

3. Governance: from owner leadership to system management

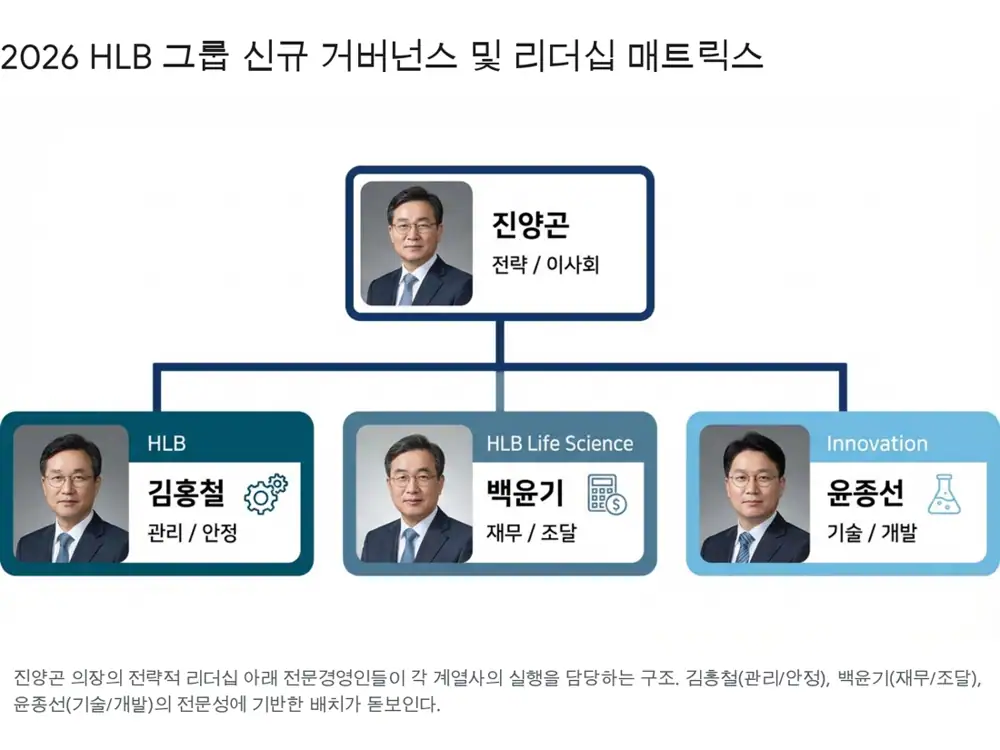

Official fact: The source says the December 2, 2025 executive reshuffle moved chairman Jin Yang-gon out of the CEO role and toward the board-chair function.

The source reads this not as withdrawal from management, but as a role reset focused on group strategy, M&A, affiliate synergy, and shareholder communication. Practical execution shifts to professional managers including Kim Hong-cheol, Baek Yoon-ki, and Yoon Jong-sun.

- Kim Hong-cheol: born in 1965, PhD in business from Soongsil University, and about 20 years at KOSDAQ Association supporting roughly 1,400 member companies.

- Baek Yoon-ki: a finance specialist with Daewoo Group, Daewoo Capital, and Aju Capital experience; the source credits him with four CB issuances and KRW 200bn of LMR investment.

- Yoon Jong-sun: a technology expert with a master's degree from La Trobe University and biomedical research training, positioned around Verismo CAR-T collaboration and HLB Innovation's technology strategy.

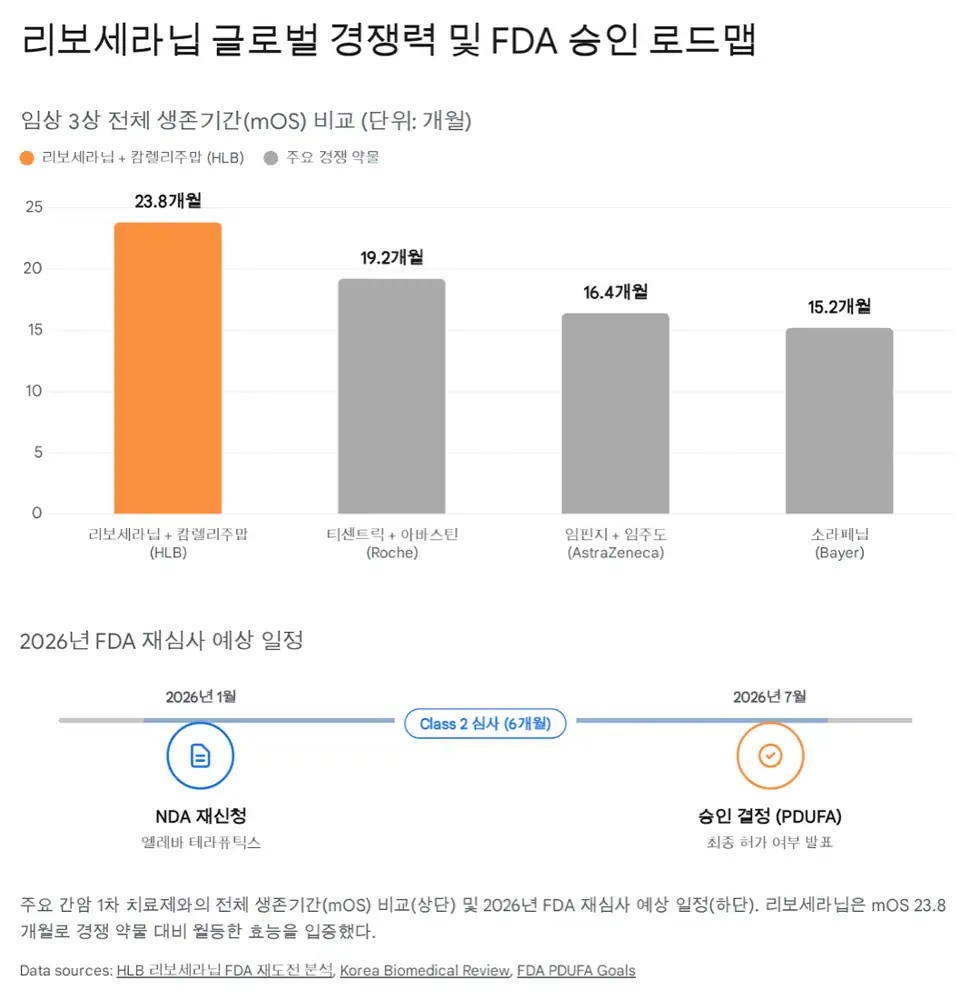

4. Third FDA attempt: CMC is the issue, not the clinical data

Official fact: The source says HLB received a first CRL in May 2024 and a second CRL in March 2025. It describes both as limited to CMC issues at partner Hengrui, with no FDA objection to clinical efficacy or safety.

| Item | Source figure/schedule | Meaning |

|---|---|---|

| First CRL | May 2024 | Facility deficiencies and COVID-19 travel restrictions delaying inspection |

| Second CRL | March 2025 | Three minor CMC items including sterilization process and visual inspection protocol |

| CARES-310 mOS | 23.8 months, HR 0.64, 36% lower risk of death | Key final-analysis data for rivoceranib + camrelizumab |

| Comparators | Sorafenib 15.2 months, Tecentriq + Avastin 19.2 months, Imfinzi + Imjudo 16.4 months | The source calls it the longest survival among existing first-line liver cancer therapies |

| Resubmission | Planned January 2026 | Likely Class 2 review if facility reinspection is needed, implying a six-month clock |

| Decision | Around July 2026 | Direct US launch readiness becomes critical immediately after approval |

Interpretation: The source treats the December 2025 publication in The Lancet Oncology as academic validation of the clinical data and frames the remaining issue as production and quality-control remediation. It also cites 89% approval after resubmission for CMC-related CRLs versus 24% for clinical-defect cases.

5. LMR Partners: capital to cross the death valley

Official fact: The source says HLB raised about KRW 200bn, or USD 145m, from LMR Partners. The structure is described as BW and EB.

The funding is expected to support US commercialization marketing for rivoceranib, nationwide distribution, and follow-on clinical development including Verismo CAR-T. The source's emphasis is that HLB secured enough runway to cross the post-approval period before revenue and cash flow stabilize.

6. My conclusion: 2026 is the proof year

- Governance: watch whether Jin's strategic leadership and professional managers' execution leadership actually fit together.

- Portfolio: the question is whether integrated HLB operates as a broader pharma-bio group across oncology, infectious disease, and dementia therapies.

- FDA: Lancet data and CMC remediation must translate into a January 2026 resubmission and a decision around July.

HLB's investment logic now has to be verified by schedules and data, not expectation alone. I would track the January 2026 resubmission, FDA Class 2 Review classification, Hengrui facility reinspection results, and Elevar's direct-sales readiness in that order.

Sources

- Source 1: Original Naver Blog post · https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224129446248

- Source 2: Chosunbiz: HLB merges with HLB Science · https://biz.chosun.com/en/en-finance/2025/09/22/L5QFP6TYF5DKHANEF3C23GL43I/

- Source 3: HLB Science analysis PDF · https://drive.google.com/open?id=1HaCmLMmL3BOF9TTFOlKWdWI8X9QozXgs

- Source 4: Yonhap: chairman Jin Yang-gon resigns as CEO · https://www.yna.co.kr/view/AKR20251202161900017

- Source 5: Daum Finance/Dailian: Jin Yang-gon resigns as CEO · https://m.finance.daum.net/quotes/A046210/news/stock/20251202155914220

- Source 6: Chosunbiz: HLB leadership change · https://biz.chosun.com/science-chosun/bio/2025/12/02/FLCSWNQRPZGJTB3MLLRG7Z24YI/

- Source 7: Dailypharm: Jin to focus on group chair role · https://www.dailypharm.com/user/news/333560?view_mode=pc

- Source 8: EBN: profile of HLB CEO nominee Kim Hong-cheol · https://www.ebn.co.kr/news/articleView.html?idxno=1689325

- Source 9: Newsway: HLB Innovation appoints Kim Hong-cheol · https://www.newsway.co.kr/news/view?ud=2023031316431457415

- Source 10: Business Post: Kim Hong-cheol named new HLB CEO · https://www.businesspost.co.kr/BP?command=article_view&num=422211

- Source 11: Toss Securities: integrated HLB and Baek Yoon-ki role · https://www.tossinvest.com/?contentType=news&contentParams=%7B%22id%22%3A%22dealsite_A00152229%22%7D

- Source 12: HLB Science leadership · https://hlbscience.com/leadership.php

- Source 13: Asia Economy: FDA CMC inspection completed · https://cm.asiae.co.kr/article/2025011416301499713

- Source 14: Pharm Edaily: rivoceranib FDA approval delayed again · https://pharm.edaily.co.kr/news/read?newsId=01971286642105616

- Source 15: HLB rivoceranib FDA retry analysis · https://drive.google.com/open?id=1VTjQ7Bd51gvq6kp91-Wq81fM7opG2-peRtlFWv1X9WY

- Source 16: CancerNetwork: FDA second CRL in HCC · https://www.cancernetwork.com/view/fda-issues-second-camrelizumab-rivoceranib-crl-in-hepatocellular-carcinoma

- Source 17: Korea Biomedical Review: Elevar resubmission interview · https://www.koreabiomed.com/news/articleView.html?idxno=29439

- Source 18: FDA: PDUFA FY 2023-2027 goals · https://www.fda.gov/media/151712/download

- Source 19: Elevar Therapeutics commercialization license news · https://elevartherapeutics.com/2023/06/01/elevar-therapeutics-to-participate-in-asco-2023-and-bio-2023-new-jersey-based-company-secures-state-license-as-it-builds-toward-commercialization/

- Source 20: Chosunbiz: LMR Partners invests $145 million · https://biz.chosun.com/en/en-science/2025/11/03/UBEXPNTF25B47BTG3ZGHAGT32M/

- Source 21: Asia Economy: HLB Group shares surge on strategic investment · https://cm.asiae.co.kr/en/article/2025110409255672017