DEEP RESEARCH · CHA BIOTECH / CGT CDMO

CHA Biotech: 2025 Capital Restructuring and Global CDMO Infrastructure Expansion

Rights offering, Pangyo CGB, Matica, and CBT101/CordSTEM-DD pipeline review

0. Bottom line first

CHA Biotech has entered a phase where it is trying to build healthcare cash flow, CGT CDMO growth optionality, and cell-therapy pipelines at the same time through a large 2025 rights offering and the Pangyo CGB investment. The near-term overhang is heavy: roughly 20 million new shares, CB/BW refixing risk, facility completion risk, and clinical-execution risk.

Official fact: The source frames the roughly KRW 151.6 billion rights offering completed in June 2025 and the December 29, 2025 correction disclosure on Pangyo CGB as core events in the company's long-term roadmap. It cites the global CGT CDMO market growing from USD 9.59 billion in 2025 to USD 88.84 billion in 2034, about KRW 118 trillion, at a 28.1% CAGR.

Interpretation: This is closer to a regenerative-medicine platform than a conventional biotech venture. Hospitals, overseas healthcare services, CDMO, and cell-therapy development are combined. That gives both stability and growth, but the model is capital-intensive, so dilution is part of the analysis.

1. Governance and business architecture

CHA Biotech's structural moat is its industry-university-research-hospital ecosystem. CHA Biotech, CMG Pharmaceutical, CHA Vaccine Institute, and Matica Biotechnology handle commercialization and production; CHA University provides basic research and talent; the research institute leads preclinical work; and the CHA hospital network supports patient recruitment and real-world clinical feedback.

Commercialization and production

Group companies divide roles across drug development, manufacturing, vaccines, and CDMO.

Basic and preclinical work

CHA University and the research institute form the base of the R&D pipeline.

Clinical network

The hospital network can connect patient recruitment, sample collection, administration, and real-world-data feedback under internal control.

| Axis | Content | Role in the source |

|---|---|---|

| Healthcare services | CHA Healthcare, HPMC, City Fertility, SMG, and more than 90 medical sites across seven countries | Surpassed KRW 1 trillion consolidated revenue in 2024 and acts as a cash-flow buffer against biotech R&D risk |

| R&D/CDMO | CHA Biotech parent, U.S. Matica, and Pangyo CGB | Growth engine targeting high-margin, high-growth cell and gene therapy development and contract manufacturing |

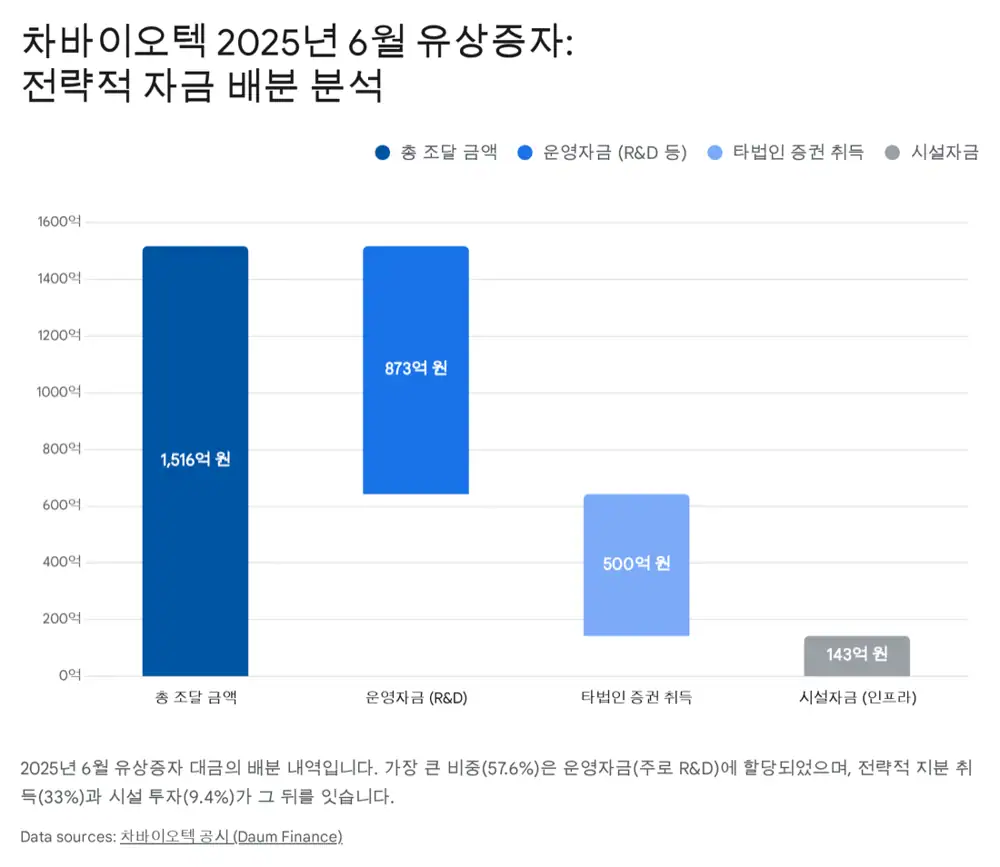

2. June 2025 rights offering

CHA Biotech completed a rights offering followed by a public offering of forfeited shares in June 2025. The source views the financing not as simple working capital but as capital for executing the growth strategy.

| Item | Figure/schedule | Meaning |

|---|---|---|

| New shares | 20,111,740 common shares | About 35% of existing shares outstanding, a large dilution burden |

| Issue price | KRW 7,540 per share | The source notes possible final-price variation |

| Total proceeds | About KRW 151.64251 billion | Funding for large-scale clinical, equity, and facility investment |

| Subscription/payment | Existing shareholders June 4-5, public offering June 10-11, payment June 13, 2025 | Capital raise completed in June 2025 |

| Use of proceeds | Amount/share | Strategic meaning |

|---|---|---|

| Operating/R&D funds | About KRW 87.3 billion, 57.6% | Accelerates CBT101 and CordSTEM-DD trials, new pipeline discovery, and research hiring |

| Investment in other companies | About KRW 50.0 billion, 33.0% | The source interprets this as likely for additional CHA Healthcare shares. CHA Healthcare/CHA Cares merger is targeted for June 2026 and domestic listing by end-2027. |

| Facility funds | About KRW 14.3 billion, 9.4% | Finishes Pangyo second Techno Valley facilities and brings in equipment |

Interpretation: This is growth capital, but existing shareholders pay through EPS dilution and overhang. The source is especially cautious that stock-price weakness after the rights offering could trigger CB/BW conversion-price refixing and increase potential shares.

3. Pangyo CGB: global CDMO hub

The Pangyo second Techno Valley CGB combines a global cell and gene therapy CDMO manufacturing facility with a biobank. The source sees it as the core of CHA Biotech's CDMO globalization.

| Item | Content |

|---|---|

| Location | Pangyo Second Techno Valley industrial sites E11-1 and E11-2 in Seongnam, Gyeonggi-do |

| Purpose | Global CGT CDMO manufacturing facility and biobank |

| Total investment | Consortium total KRW 116.025 billion, excluding VAT; increased by about 5%, or KRW 5.525 billion, from the original KRW 110.5 billion |

| Consortium structure | CHA Biotech 50% (KRW 58.0125 billion), CMG Pharmaceutical 40% (KRW 46.410 billion), CHA Cares 10% (KRW 11.6025 billion) |

| CHA Biotech funding | Internal funds about KRW 13.8 billion (23.8%) and long-term bank borrowings about KRW 44.2 billion (76.2%) |

| Correction disclosure | On December 29, 2025, investment end date was extended three months from December 31, 2025 to March 31, 2026. Contractor: Shindonga Engineering & Construction, CEO Kim Se-joon |

Interpretation: The source reads the extension not merely as construction delay but as a possible strategic pause to meet global cGMP standards, FDA/EMA-level quality systems, and validation steps such as IQ/OQ/PQ. For global customers, the quality system matters more than physical completion alone.

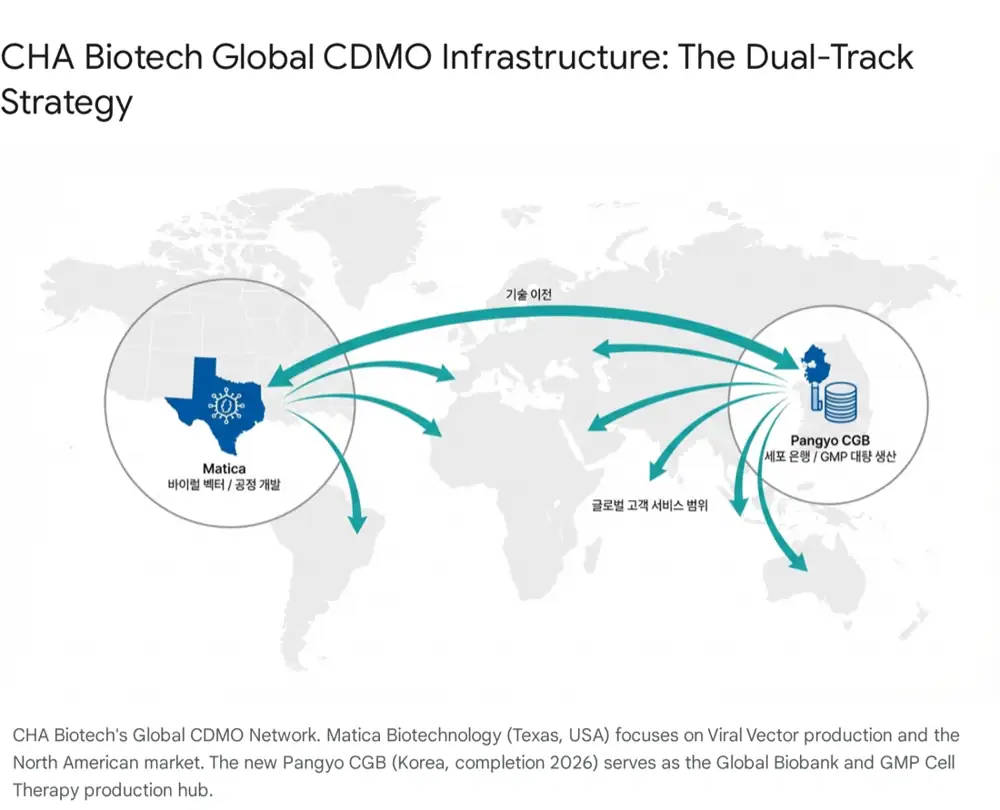

4. U.S. Matica plus Korea Pangyo dual track

CHA Biotech's CDMO strategy splits roles between the U.S. and Korea. Matica Biotechnology in Texas focuses on viral-vector production and early process development for Western markets. Pangyo CGB handles cell-line storage and large-scale GMP manufacturing for Asia and global production.

Customers can use a one-stop option: development in the U.S. and production in Korea. The source views this as a geopolitical-risk hedge for global pharmaceutical companies seeking supply-chain diversification.

5. R&D pipeline

The pipeline funded by about KRW 87.3 billion of rights-offering proceeds is the key to CHA Biotech's value re-rating. The source focuses on CBT101 and CordSTEM-DD for clinical progress and licensing potential.

| Pipeline | Technology/indication | Status and meaning |

|---|---|---|

| CBT101 | Autologous NK cell therapy targeting solid tumors | Proprietary culture technology is described as increasing NK-cell expansion by about 2,000x and activity above 90%. Phase 1 in solid tumors showed no dose-limiting toxicity, confirming safety and tolerability. |

| CBT101 | Regulatory achievement | Received FDA orphan drug designation for malignant glioma, with benefits such as tax credits, fee waivers, and seven years of market exclusivity after approval. |

| CBT101 | Competition | Fate Therapeutics (iPSC-derived NK) and Nkarta (CAR-NK) focus mainly on blood cancers, while CBT101 differentiates by targeting solid tumors such as liver cancer, gastric cancer, and glioblastoma. |

| CordSTEM-DD | Umbilical-cord-derived MSC therapy for degenerative lumbar disc disease | Completed Phase 1/2a in April 2022 and confirmed safety in 36 patients. It aims to regenerate disc tissue and reduce inflammation as a disease-modifying drug, not just relieve pain. |

| CordSTEM-POI | Premature ovarian insufficiency therapy | Phase 1 IND approved; the source sees synergy with the CHA hospital group's fertility-treatment strengths. |

6. Financial risk and overhang

R&D and early CDMO investment

Operating cash flow is pressured by R&D spending and early CDMO investment, while investing cash flow sees large outflows for Pangyo facilities and subsidiary stakes.

CB/BW/EB and rights issue

The company has relied on convertible bonds, bonds with warrants, exchangeable bonds, and equity issuance to fund growth investment.

New shares and refixing

About 20 million new shares were listed through the June 2025 rights offering, and outstanding 8th CB and 9th BW instruments can become selling pressure if the stock rises.

Interpretation: CHA Biotech has a large growth blueprint, but also high capital-market dependence. New CDMO orders, CGB utilization, and CBT101 Phase 2 entry need to arrive fast enough to outweigh dilution.

7. Bull / Bear

Bull Case

- Pangyo CGB completion in March 2026 starts global CDMO orders linked with Matica in the U.S.

- CBT101 and CordSTEM-DD Phase 2 entry and data improve licensing potential.

- CHA Healthcare IPO targeted for 2027 crystallizes subsidiary value for the parent.

Bear Case

- Shareholder dilution continues through the rights offering and mezzanine instruments.

- Clinical failure, facility delay, or weak CDMO orders remain operating risks.

- High long-term borrowing share can raise interest-cost sensitivity.

8. Overall view

CHA Biotech is a regenerative-medicine platform with both hospital-business stability and drug-development upside. As the source puts it, it has characteristics similar to a “regenerative-medicine sector ETF.” The 2025 capital raise and infrastructure investment were necessary for long-term growth, but they carried near-term shareholder-cost.

The indicators I would watch are Pangyo CGB completion and validation, new CDMO orders, CBT101 Phase 2 entry, CordSTEM-DD late-stage trial planning, and the CHA Healthcare IPO timetable. If execution follows, the overhang can be interpreted as the cost of growth; if delayed, dilution pressure can weigh first.

Sources

- Original blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224128731774

- Source 1: https://www.novaoneadvisor.com/report/cell-and-gene-therapy-cdmo-market

- Source 2: https://www.kedglobal.com/mergers-acquisitions/newsView/ked202502260007

- Source 3: https://www.koreabiomed.com/news/articleView.html?idxno=26820

- Source 4: https://m.finance.daum.net/quotes/A085660/news/disclosure/20250415037779

- Source 5: http://www.chamc.co.kr/media/press_detail.cha?seq=10284

- Source 6: https://www.medigatenews.com/news/1666409145

- Source 7: https://ir.fatetherapeutics.com/news-releases/news-release-details/fate-therapeutics-reports-third-quarter-2025-financial-results

- Source 8: https://ir.nkartatx.com/news-releases/news-release-details/nkarta-reports-second-quarter-2025-financial-results-and

- Source 9: http://www.kmedinfo.co.kr/news/articleView.html?idxno=80509

- Source 10: https://delta.larvol.com/Products/?ProductId=4bd88e9b-3d9c-4932-9476-7a183a776d61

- Source 11: http://en.chabio.com/company/history1.cha