DEEP RESEARCH · SAMJI ELECTRONICS / SAMSUNG SEMICONDUCTOR DISTRIBUTION

Samji Electronics: SAMT Volume Consolidation and Semiconductor Distribution Re-rating

Mujin Electronics distribution-right transfer, Samsung SCM change, 3Q25 earnings, and the double discount

0. Bottom line first

The core of Samji Electronics is no longer a simple telecom-equipment story. Through subsidiary SAMT, it has become a key Samsung Electronics semiconductor-distribution partner. 3Q25 revenue of about KRW 1.1605 trillion and operating profit of KRW 44.1 billion show that the structural change is now visible in the numbers.

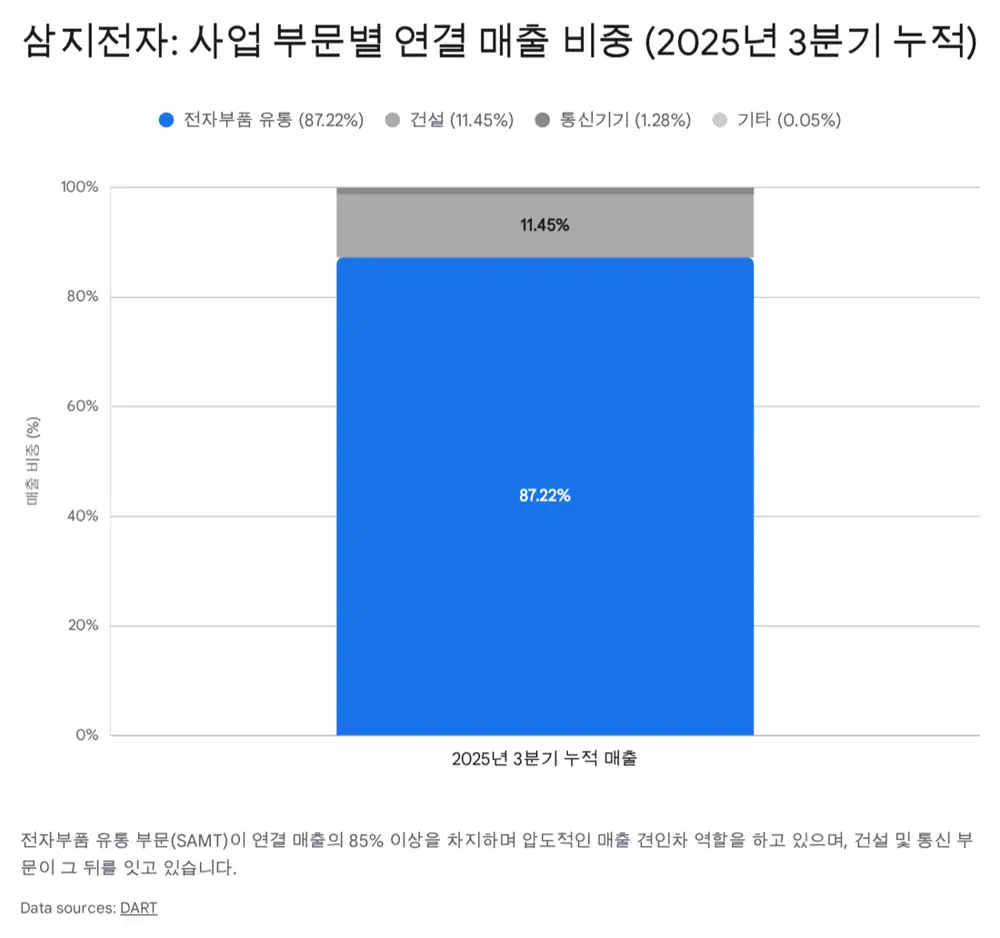

Official fact: The source says Samji Electronics started in 1981 as a telecom-equipment company and, by end-3Q25, had become a conglomerate-style business spanning semiconductor distribution, semiconductor clean-room construction, and energy-related new businesses. The key subsidiary is SAMT (031330.KQ).

Interpretation: The weakness of Samsung Electronics dependence and the strength of being a trusted Samsung supply-chain partner come from the same source. That is why the stock receives a low multiple, but also why operating leverage can expand sharply when the semiconductor cycle improves.

1. Portfolio: from telecom to semiconductor conglomerate

Samji began with wireless repeaters and network equipment, but diversified to reduce earnings volatility tied to carrier CAPEX cycles. The decisive step was acquiring SAMT, which originated from Samsung's semiconductor distribution business.

| Segment | Content | Meaning in the source |

|---|---|---|

| Electronic-parts distribution | SAMT, more than about 85% of consolidated revenue | Core cash cow supplying Samsung memory (DRAM, NAND), System LSI such as APs and image sensors, and OLED/LCD to Korean and overseas IT companies |

| Telecom | 5G/LTE repeaters, in-building DAS, Open RAN O-RU | LG Uplus is the main customer; Japan exports are expanding, and niche products such as OIDD can carry higher margins |

| Construction | Seil ENS semiconductor clean rooms, machinery, fire-safety, and electrical work | Linked to Samsung Electronics and SK hynix fab expansion, Pyeongtaek, Yongin cluster, and Taylor, Texas |

| Other/energy | Real estate leasing, solar, battery parts, battery recycling | Options for the next growth engine using cash resources |

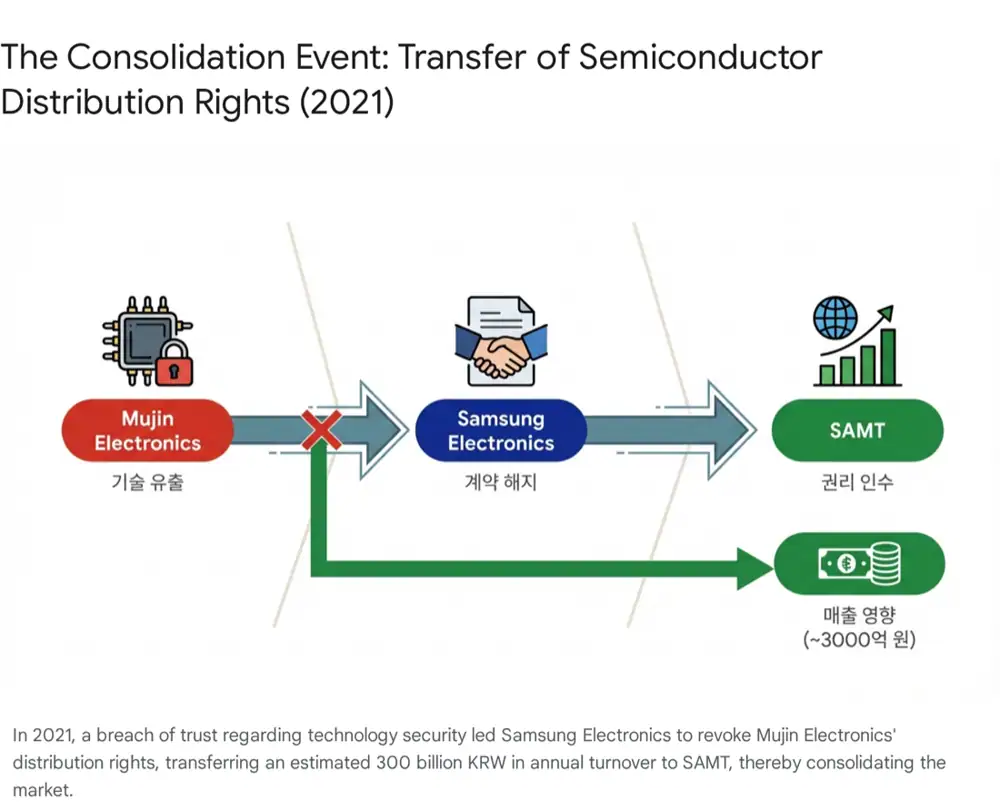

2. Game changer: Mujin Electronics volume transfer

The source treats the 2021 Mujin Electronics case as the most important inflection point in Samji/SAMT history. Mujin, once a major Samsung Electronics distributor, was indicted over allegations of leaking semiconductor cleaning-equipment technology to a Chinese competitor. Samsung terminated the dealership contract in June 2021, ending a relationship that had lasted since 1996.

Samsung then transferred about KRW 300 billion of annual distribution volume handled by Mujin to SAMT instead of splitting it among several dealers. The source reads this as a symbol of Samsung's SCM moving toward security, transparency, and a smaller group of trusted partners.

Structural stability

SAMT is a KOSDAQ-listed company with verified accounting transparency and internal controls, stronger than privately owned dealerships in risk management.

Origin in Samsung C&T distribution

The source says SAMT understood Samsung Electronics' culture and processes better because of its roots.

Working-capital capacity

Absorbing KRW 300 billion of annual volume requires inventory-financing capacity. SAMT had both its own capital and Samji as a parent.

Interpretation: The transfer did more than add revenue. It improved buying power, customer bargaining power, logistics efficiency, and market position. SAMT became a mega-distributor within Samsung's distribution channel.

3. Symbiotic structure with Samsung Electronics

As of 2025, Samsung is focused on regaining leadership in HBM and 3nm/2nm foundry processes. The source argues that this makes distributors like SAMT more important, not less. Samsung can focus internal resources on hyperscalers such as Google, Amazon, and Meta while relying on distributors for thousands of small and mid-sized IT customers.

- Long-tail customer management: Supports design-in of Samsung components for appliance, IoT, and automotive-parts customers.

- Inventory buffer: Pre-purchases and stores Samsung products, helping manufacturers reduce inventory burden and smooth cash flow.

- AI spillover: Even if SAMT does not directly distribute HBM, AI servers increase demand for DDR5 DRAM and high-capacity NAND eSSDs.

- System LSI expansion: AI TVs, robot vacuums, and automotive electronics expand demand for MCUs, PMICs, and image sensors.

Interpretation: SAMT's moat comes from Samsung's market power. The right to distribute products from the No. 1 DRAM and NAND supplier is a barrier that competing distributors cannot easily reproduce.

4. 3Q25 results: leverage in the numbers

| Item | Figure | Meaning |

|---|---|---|

| 3Q25 revenue | About KRW 1.1605 trillion | Up 39.9% from KRW 829.7 billion a year earlier, confirming quarterly revenue above KRW 1 trillion |

| 3Q25 operating profit | KRW 44.1 billion | Up 115.6% from KRW 20.4 billion a year earlier, showing operating leverage above revenue growth |

| Distribution segment | About 87% of consolidated revenue, more than KRW 1 trillion quarterly revenue, KRW 27.1 billion operating profit | Driven by memory ASP increases, IT-season volume, and possible inventory valuation gains |

| Telecom/construction | LG Uplus maintenance, Japan exports, Pyeongtaek finishing and maintenance work | Legacy and Seil ENS businesses add stable cash flow |

The source views Samji as maintaining a low debt ratio and abundant liquidity. Although distributors naturally hold large receivables and inventories, the Samsung supplier relationship and quality customer base are said to limit bad-debt risk.

5. Valuation: the double discount

The source estimates Samji's 2025 P/E at about 3.1-3.3x. That is far below the KOSDAQ IT-sector average of 15-20x and below subsidiary SAMT's about 6.6x P/E. P/B is also below 0.5x, implying an extreme discount to liquidation value.

| Discount factor | Content | Potential resolution |

|---|---|---|

| Holding-company discount | SAMT is already listed, so some investors prefer direct exposure to the operating subsidiary | The roughly 50% SAMT stake held by Samji may explain a large portion of Samji's market cap |

| Low distributor multiple | Semiconductor distribution is viewed as lower value-add than manufacturing or fabless design | If the Mujin volume transfer created a stronger exclusive position, a peer premium could be justified |

| Shareholder-return skepticism | Cash-rich undervalued company, but action is the variable | The source mentions 3-4% dividend yield and room for buybacks/cancellations |

Official fact: The source compares global semiconductor distributors Arrow Electronics and Avnet, saying they trade around 7-9x P/E. It also says Samji's valuation appeal is strong versus Korean peers such as Uniquest.

6. Risks

Single Samsung axis

If the Samsung relationship changes or direct sales expand, alternatives are limited. The source still sees near-term risk as low because Samsung appears to strengthen trusted partners.

Memory-price downturn

If memory prices fall, inventory valuation losses can occur, and oversupply concerns after 2026 could weaken profitability.

U.S.-China semiconductor conflict

U.S. restrictions on China can affect Samsung's China revenue and increase volatility for SAMT, which has some Greater China customers.

7. Overall view

The source concludes that Samji is an undervalued value stock with both stability from distribution and growth from the semiconductor super-cycle. The 2021 Mujin volume transfer was not a one-off headline; it structurally raised SAMT's and Samji's revenue baseline.

The three checkpoints I would track are: how much Samsung's semiconductor recovery flows into SAMT's operating margin, whether the market revalues Samji's SAMT stake and cash assets, and whether battery/energy new businesses and stronger shareholder returns become actual actions. If these align, Samji can move beyond the old “telecom-equipment stock” frame.

Sources

- Original blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224128106427

- Source 1: https://www.thelec.kr/news/articleView.html?idxno=13690

- Source 2: https://www.moneys.co.kr/article/2021080513408033331

- Source 3: http://thelec.net/news/articleView.html?idxno=3189

- Source 4: https://m.finance.daum.net/quotes/A037460/news/stock/20210805134257590

- Source 5: https://biz.chosun.com/stock/market_trend/2021/08/05/2TKDSJYBTNFIZN75E3WOUDU6SY/

- Source 6: http://www.newstomato.com/ReadNewspaper.aspx?epaper=1&no=1065187

- Source 7: https://v.daum.net/v/20210805133104194

- Source 8: https://sqmagazine.co.uk/samsung-statistics/

- Source 9: https://images.samsung.com/is/content/samsung/assets/global/ir/docs/2025_3Q_conference_eng.pdf

- Source 10: https://www.samsung.com/us/aboutsamsung/sustainability/supply-chain/supplier-list/

- Source 11: https://news.samsung.com/global/samsung-electronics-announces-third-quarter-2025-results

- Source 12: https://semiconductor.samsung.com/about-us/business-area/system-lsi/

- Source 13: https://www.astutegroup.com/news/industrial/samsungs-dram-and-nand-gains-reinstate-its-lead-in-the-global-memory-market/

- Source 14: https://evertiq.com/news/57190

- Source 15: https://www.techinsights.com/blog/analysis-samsung-maintained-largest-smartphone-vendor-2024

- Source 16: https://www.tossinvest.com/stocks/A037460/news?menu=disclosure&symbol-or-stock-code=A037460&contentType=disclosure&contentParams=%7B%22id%22%3A%22DART%3AA%3A037460-20251114002421%22%2C%22companyCode%22%3A%22037460%22%2C%22reportItem%22%3A%224.2.0%22%7D

- Source 17: https://www.tossinvest.com/disclosure?symbol-or-stock-code=A031330&contentType=disclosure&contentParams=%7B%22id%22%3A%22DART%3AA%3A031330-20251114001430%22%2C%22companyCode%22%3A%22031330%22%2C%22reportItem%22%3A%224.2.0%22%7D

- Source 18: https://www.investing.com/equities/samji-electronics-co-ltd

- Source 19: https://simplywall.st/stocks/kr/tech/kosdaq-a037460/samji-electronics-shares

- Source 20: https://www.judal.co.kr/?view=stockAI&shareToken=q24O6z1SIrFpFA8q

- Source 21: https://www.economidaily.com/view/20250821165924553

- Source 22: https://zdnet.co.kr/view/?no=20240131101010

- Source 23: https://simplywall.st/stocks/vn/tech/hnx-smt/sametel-shares/valuation

- Source 24: https://au.investing.com/pro/KOSDAQ:A037460/compare/KOSDAQ:A051390,KOSDAQ:A073490,KOSDAQ:A038950,KOSDAQ:A189300,KOSDAQ:A031330,KOSDAQ:A264450