DEEP RESEARCH · CELLOMAX SCIENCE (471820.KQ)

Cellromax Science: Governance Paradox and Regulatory Risk

A review of the pharmacy-membership supplement business, biotech investment, advertising regulation, and related-party risk

0. Bottom line first

Cellromax Science has a real distribution moat through more than 5,200 member pharmacies, but after listing, relational and policy flaws have become more visible. I would first treat it as a premium supplement distributor exposed to regulatory risk, not as a biotech growth stock.

1. Company Structure: Strengths and Limits of a Fabless Supplement Model

Official fact: Cellromax focuses on product planning, formulation research, marketing, and channel management, while outsourcing 100% of production to ODM/OEM partners such as Novarex, Kolmar BNH, RP Bio, and Naturetech.

- Advantage: it can avoid production CAPEX and depreciation while focusing resources on pharmacy-network expansion.

- Limit: raw-material prices, regulatory compliance costs, and Smart GMP investment by manufacturers can be passed through as higher outsourcing costs.

- Listing: it entered KOSDAQ on December 13, 2024 through a merger with Hanwha Plus No. 3 SPAC; the merger ratio was 1:0.2270405 and the source cites about KRW 11.9B in inflow.

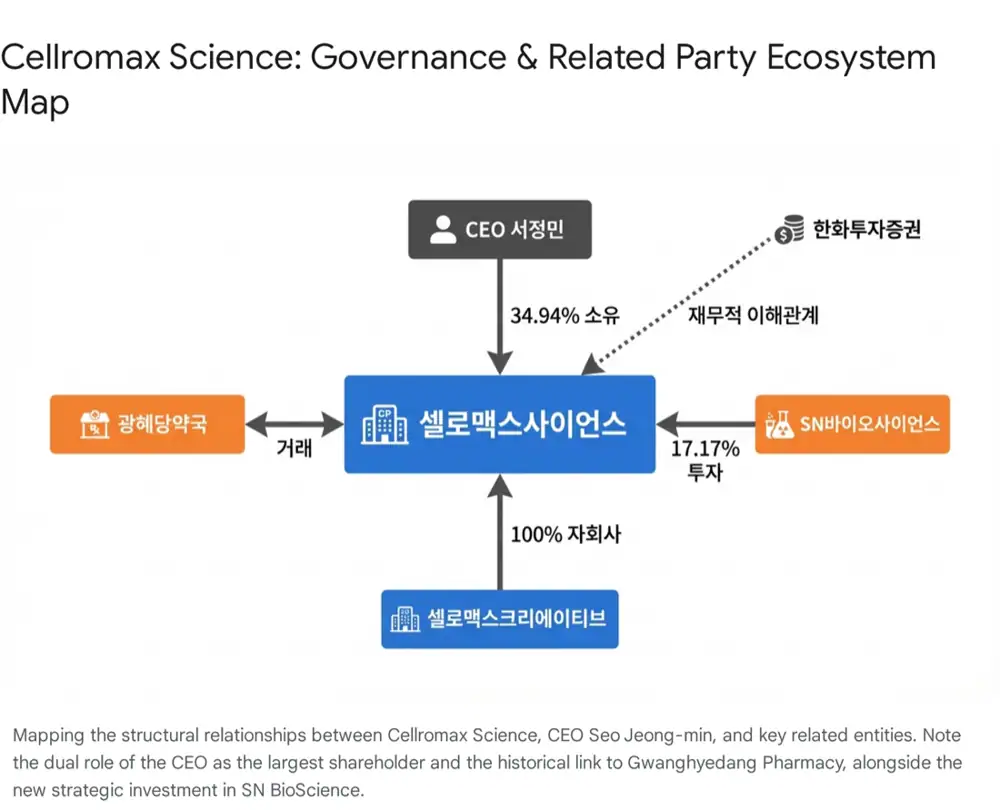

2. Relational Flaws: Related Parties and Capital Allocation

Sales source or conflict?

Gwanghyedang Pharmacy, where CEO Jeong-min Seo reportedly served as representative pharmacist from 1999 to 2014, remains one of the company’s trading partners. Fairness of terms matters.

17.17% stake acquisition

In September 2025, Cellromax acquired 17.17% of SN BioScience and became the second-largest shareholder. SNB-101’s FDA orphan-drug designation is positive, but synergy between supplements and oncology drug development remains unproven.

Cellromax Creative

Established in January 2025 as a wholly owned subsidiary. The stated rationale is internalizing marketing and design, but future ownership or internal-transaction changes could raise tunneling concerns.

Interpretation: Once core cash flow is allocated to unrelated biotech investment, investors should examine agency problems and potential impairment before pricing in growth optionality.

3. Policy Flaws: Smart GMP and Advertising Rules

- Smart GMP: stronger digitization and automated record-keeping in manufacturing can raise ODM/OEM partner costs and then Cellromax’s supply prices.

- Advertising regulation: health supplements cannot be advertised in ways that imply disease prevention or treatment. AI media-board marketing inside pharmacies may attract scrutiny because it uses pharmacy context and pharmacist credibility.

- Listing maintenance and overhang: a concentrated ownership structure near 70% for CEO Seo and related parties can reduce liquidity, while SPAC convertible bonds added 245,203 shares in Q3 2025 alone.

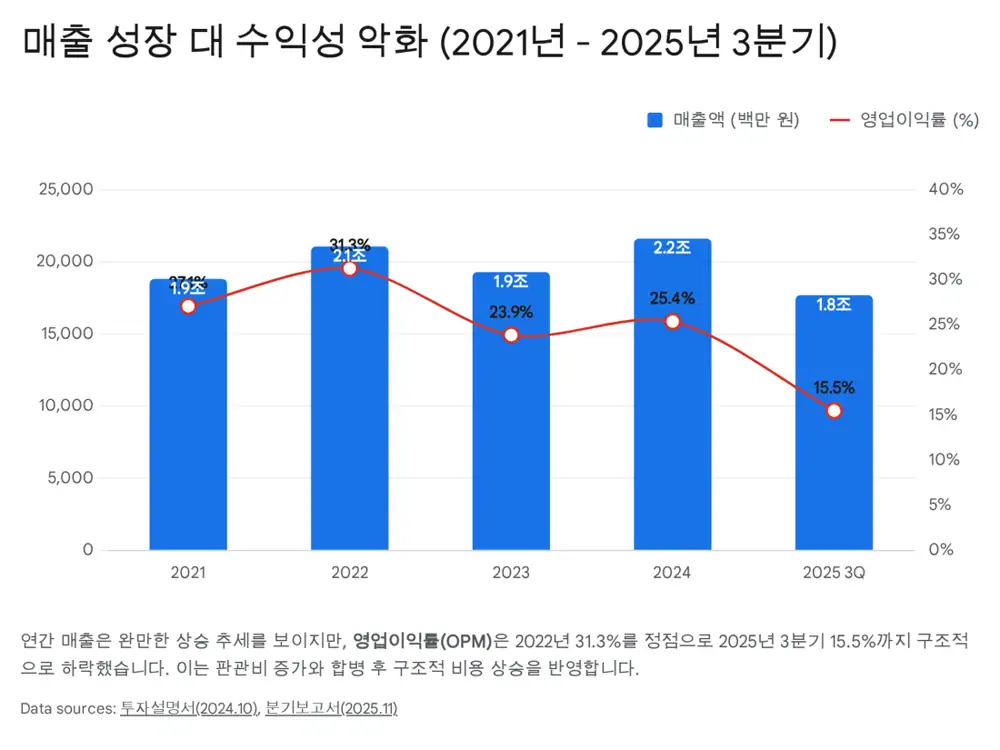

4. Financials: Revenue Growth Decoupled From Margin

| Item | 2021 | 2022 | 2023 | 2024 full year | Q3 2025 cumulative |

|---|---|---|---|---|---|

| Revenue (KRW mn) | 18,837 | 21,086 | 19,310 | 21,630 | 17,708 |

| Operating profit (KRW mn) | 5,110 | 6,610 | 4,619 | 5,501 | 2,749 |

| OPM | 27.1% | 31.3% | 23.9% | 25.4% | 15.5% |

| Net income (KRW mn) | 3,984 | 4,732 | 4,499 | - | 2,651 |

Interpretation: Cumulative Q3 2025 revenue of KRW 17.7B annualizes to about KRW 23.6B, suggesting roughly 9% growth from KRW 21.6B in 2024. But OPM fell from 31.3% in 2022 to 15.5% in Q3 2025. New subsidiary costs, customer-care hiring, listing costs, and outsourced-processing inflation are all suspected factors.

5. Growth Ceiling and Scenarios

Official fact: The source states that the company has about 5,200 member pharmacies, roughly 22% of Korea’s approximately 24,000 pharmacies. Exports currently account for less than 1% of total sales.

Best Case

- SNB-101 clinical progress leads to a licensing-out event, Cellromax’s stake value rises, and the core business restores OPM to the 20% range through higher-priced products.

Base Case

- The core business grows 5-10% per year, but cost increases keep OPM in a 10-15% band. Biotech investment may be reflected as losses or valuation losses.

Worst Case

- MFDS advertising enforcement stops AI media-board operation, SNB-101 clinical failure creates impairment, and related-party questions escalate into tax or regulatory review.

6. Final View

The company’s intrinsic value sits in its pharmacist network. But it is not yet proven whether that network is a structural company asset or a relationship network centered on the CEO. The checklist is 1) additional funding for SN BioScience, 2) operating-margin recovery, and 3) transparent disclosure of related-party transactions.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224128104973

- Article on FDA-recognized oncology drug: https://www.pinpointnews.co.kr/news/articleView.html?idxno=406609

- Cellromax pharmacist-and-health company page: https://www.cellromax.co.kr/bbs/board.php?bo_table=job&page=

- Dailypharm: Cellromax investment in SN BioScience: https://www.dailypharm.com/user/news/333895

- Daum: Cellromax acquires 17.17% of SN BioScience: https://v.daum.net/v/20250923181247898?f=p

- YouTube interview with Cellromax CEO Jeong-min Seo: https://www.youtube.com/watch?v=L4FLZgTTpSA