DEEP RESEARCH · MOBIIS

Mobiis: Big-Science Control Technology Plus Smart-Factory Cash Flow

A view on EPICS, fusion/accelerator controls, smart factories, and the balance-sheet boost after the ADM Korea exit

0. Bottom line first

Mobiis should be read less as a generic IT-solutions company and more as a deep-tech firm in the narrow, high-barrier market for big-science control systems. The pillars are EPICS-based control technology, smart-factory revenue, and more than KRW 30bn of cash from the ADM Korea sale.

EPICS control

Middleware capability for ITER, synchrotron accelerators, and other big-science control systems.

Smart factory

Industrial AI/QRP solutions help buffer project-based big-science revenue volatility.

ADM Korea exit

After the 2024 sale, net-cash capacity for R&D and project execution improved.

1. Second founding and technology pivot

Official fact: Mobiis was founded in April 2000 and initially supplied communications devices and software solutions to Samsung Electronics, KT, and others. In 2010 it declared a second founding and shifted toward precision control for accelerators and fusion facilities. The source says it invested about KRW 3.0bn over two years from 2010 to develop an LLRF accelerator control system.

Interpretation: The pivot moved the company away from crowded SI markets into long-cycle national science infrastructure where reference and domain expertise matter.

2. Management and governance

Official fact: CEO Kim Ji-heon became co-CEO in 2005 and sole CEO in 2015. As of end-September 2025 he is presented as the largest shareholder with 26.02%, or 28.29% including related parties.

Interpretation: Big-science control requires both physics-domain knowledge and software engineering. The “learning organization” philosophy is a strategy for building a people-based moat.

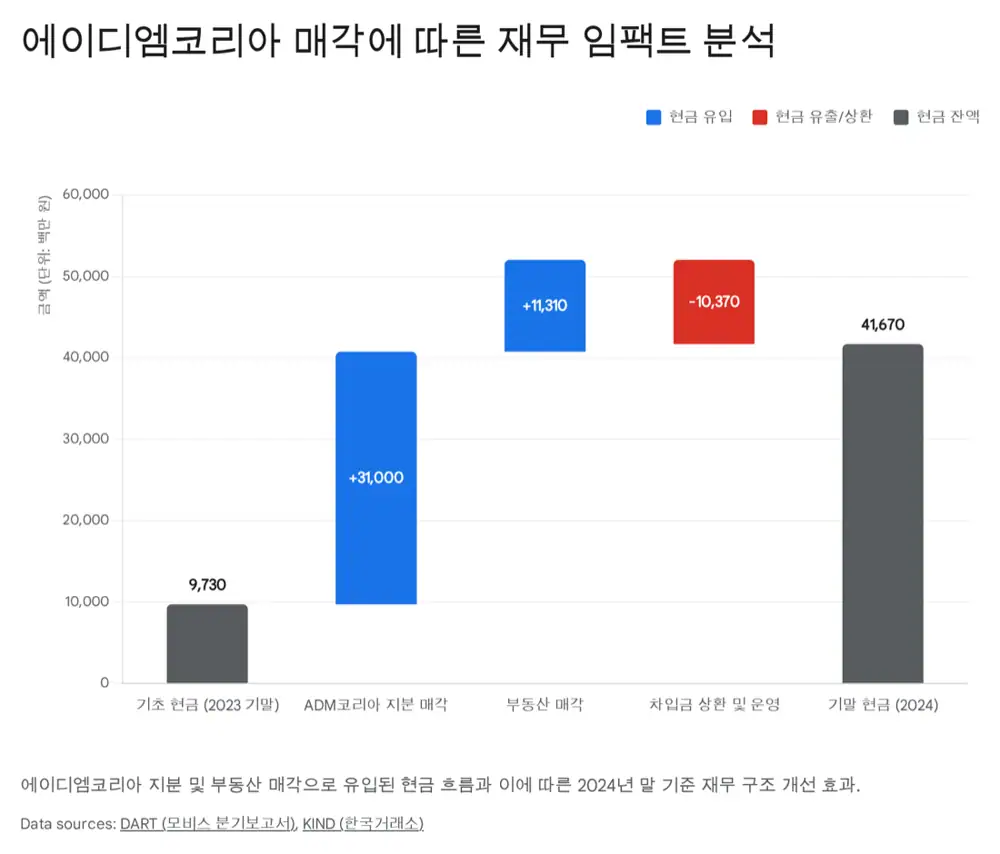

3. ADM Korea exit

Mobiis acquired ADM Korea, a bio CRO company, in January 2019, and proposed applying machine-learning and big-data technology to clinical data. On March 11, 2024, the board resolved to sell its stake and control, giving the company financial capacity to refocus on deep-tech controls.

Interpretation: This is better viewed as a capital-allocation exit than a simple retreat from bio. The cash can support fusion/accelerator R&D, project execution, and talent retention.

4. Business segments and 2025 3Q figures

| Item | 2024 3Q cumulative | 2025 3Q cumulative | Change/comment |

|---|---|---|---|

| Fusion/accelerator revenue | KRW 1.70bn | KRW 1.39bn | Slight decline due to large-project cycle |

| Smart-factory revenue | KRW 3.32bn | KRW 2.44bn | 63.7% of total revenue, now core business |

| Cash and equivalents | KRW 9.7bn at end-2023 | KRW 32.5bn | Up 235%, effect of ADM Korea sale |

| Net income | Loss | KRW 610mn | Turned profitable, helped by financial income |

Official fact: The table is reconstructed from Mobiis’ 10th and 9th quarterly reports as cited by the source.

5. Growth plans and risks

- AI controls: apply machine learning to fusion plasma instability and accelerator beam stabilization.

- Global orders: use ITER references for accelerator and fusion facilities in emerging countries, Europe, and China.

- New areas: smart farm and healthcare have no concrete revenue yet but are monitored as control-technology applications.

- Risks: government R&D budgets, retention of specialized engineers, and intense smart-factory competition.

6. Investment checkpoints

The source frames Mobiis as a hidden champion with scarce EPICS technology, net-cash safety, and a roadmap around the Ochang synchrotron and K-DEMO. Because big-science schedules can slip, the key is how much smart-factory and maintenance revenue can fill order gaps.

Sources

- 모비스 사업보고서 PDF: https://www.mobiis.com/user/attachment/uploads/2023/03/%EB%AA%A8%EB%B9%84%EC%8A%A4%EC%A0%9C7%EA%B8%B0-%EC%82%AC%EC%97%85%EB%B3%B4%EA%B3%A0%EC%84%9C-1.pdf1_.6M-1.pdf

- 조선비즈: 모비스 현장답사: https://biz.chosun.com/site/data/html_dir/2017/03/20/2017032001260.html

- KRX 공시: 모비스 사업보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250318001426&docno=&viewerhost=&

- ITER: Advancing the interlock system: https://www.iter.org/node/20687/advancing-iter-interlock-system

- 뉴시스: ITER 완공 지연: https://mobile.newsis.com/view/NISX20240705_0002799990

- YouTube: 2025년 핵융합의 현황과 전망: https://www.youtube.com/watch?v=V9quWTkyEZ0

- 파이낸셜포스트: 방사광 가속기 공급사: https://www.financialpost.co.kr/news/articleView.html?idxno=209357

- 머니S: 방사광가속기 초전도체 이슈: https://www.moneys.co.kr/article/2024101709232851117