DEEP RESEARCH · KISWIRE

Kiswire: Where Deep Value Meets Superconducting Energy Optionality

A combined view of wire-rope cash flow and KAT/EnableFusion nuclear-fusion optionality

0. Bottom line first

Kiswire combines stable cash flow from traditional steel-wire processing with growth options in superconducting wire and fusion. The source’s 0.31x PBR and KRW 564.3bn market cap suggest that assets and KAT’s potential are not fully reflected.

Rope and wire

High-value products for offshore, long-span bridges, and tire reinforcement drive quality of earnings.

KAT

A wholly owned superconducting-wire subsidiary with Nb3Sn and fusion/accelerator track records.

EnableFusion

A KRW 6.0bn strategic investment pointing beyond materials toward fusion engineering platforms.

1. Manufacturing base

Official fact: Kiswire was founded on September 22, 1945, and produces wire rope and specialty wire. As of 2025 3Q it had 24 consolidated subsidiaries and production bases in the United States, Malaysia, China, Vietnam, and other regions.

Interpretation: The company is in mature industries, but it emphasizes quality-sensitive niches such as offshore rope, long-span bridge cables, and high-strength tire reinforcement.

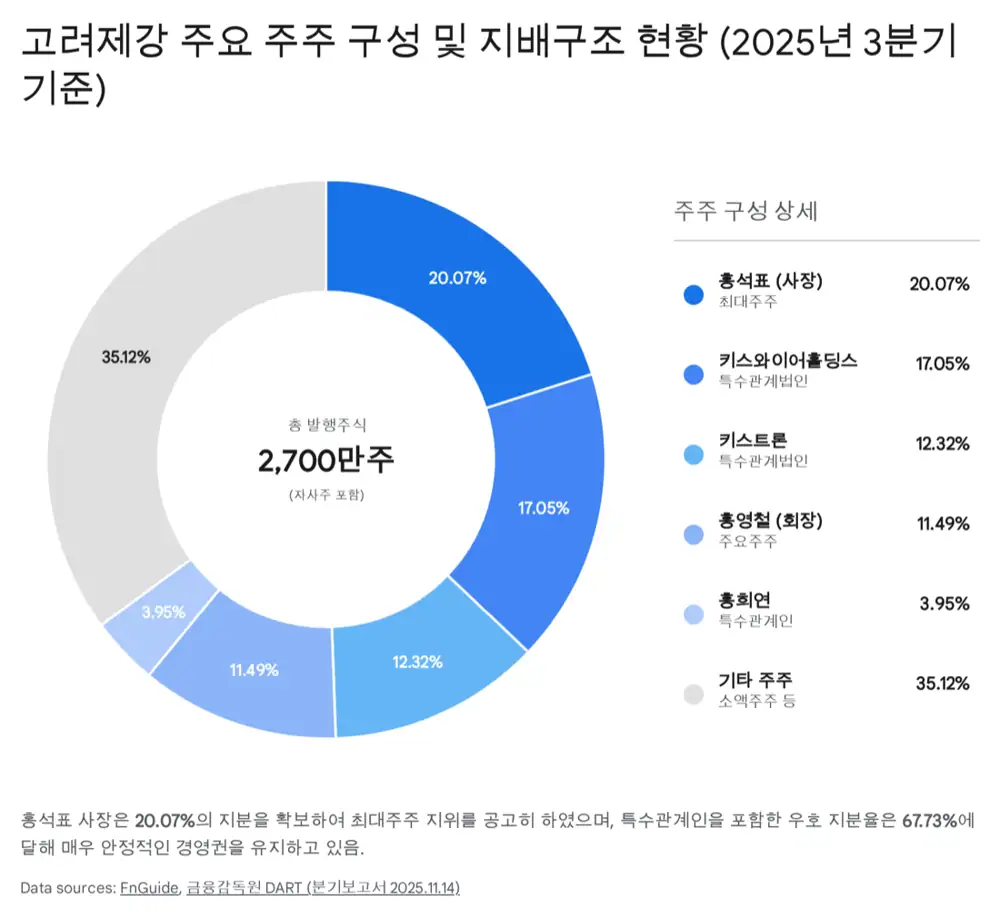

2. Governance and third-generation management

Official fact: President Hong Seok-pyo, born in 1979 and the eldest son of Chairman Hong Young-chul, is presented as the largest shareholder with 20.07% as of end-September 2025. Chairman Hong holds 11.49%, and related parties hold 67.73%.

Interpretation: With succession stabilized, shareholder returns and Korea’s value-up theme become more important.

3. Two industry cycles

Traditional demand faces high rates and China-property weakness, but special infrastructure and offshore projects remain quality-driven. EV transition reduces some engine-related demand while increasing need for stronger tire reinforcement.

Official fact: The source cites fusion-market scenarios of USD 40bn-80bn around 2035 and more than USD 350bn by 2050 if milestones are achieved. It also notes expected double-digit growth for superconducting wire.

4. KAT and fusion track record

Official fact: KAT was founded in 2004 as a wholly owned superconducting-wire subsidiary. The source says KAT supplied about 137 tons, around USD 150mn, of Nb3Sn wire for ITER TF and CS coils during 2009-2016. For DTT, it supplied 55 tons under the first contract and signed a second contract in April 2025 worth EUR 16mn, about KRW 24.0bn, for 18.4 tons of CS-coil wire.

Interpretation: KAT’s value rises if it expands from research-grade special materials into commercial fusion, MRI, and power equipment.

5. Earnings and margin of safety

| Item | Source figure | Meaning |

|---|---|---|

| 2025 3Q cumulative operating profit | Up about 99.8% YoY | Evidence of profitability-focused management |

| Rope segment | Revenue KRW 353.1bn, OP KRW 29.9bn | Main profit contributor |

| Wire segment | Revenue KRW 1.1228tn | Loss reduction is key |

| Debt ratio | About 35% | Presented as low versus manufacturing average |

| Total assets/equity | KRW 2.6306tn / KRW 1.9440tn | Asset-value character |

| Retained earnings | About KRW 1.6830tn | Capacity for investment, M&A, and returns |

6. Valuation and risks

The source gives a December 2025 market cap of about KRW 564.3bn, share price near KRW 20,900, PBR of 0.31x, and PER of about 10.7x. It compares DSR Steel at 0.31x PBR and 2.46x PER, and Manho Rope & Wire at 0.77x PBR and loss-making.

- KAT orders, FCC/private-fusion projects, and a possible long-term KAT IPO are re-rating triggers.

- EnableFusion must prove it can connect turnkey fusion projects to Korea’s supply chain.

- Without stronger shareholder returns, the low-PBR discount can persist.

- Steel, auto, offshore cyclicality and fusion commercialization delays are risks.

Sources

- Kiswire: Wire Connects the World: https://www.kiswire.com/english/cyberpr/down/KISWIRE_BRC_EN_spread.pdf

- MarketsandMarkets: Steel Wire Rope leading players: https://www.marketsandmarkets.com/ResearchInsight/steel-wire-rope-companies.asp

- KAT: Business overview: https://www.kiswire-kat.com/sub0101

- FnGuide: 고려제강 기업정보: https://comp.fnguide.com/SVO2/ASP/SVD_Main.asp?gicode=A002240&MenuYn=Y

- 뉴스웨이: 홍영철 회장 지배력: https://www.newsway.co.kr/news/view?ud=2018060409291499856

- Korea JoongAng Daily: No energy security: https://koreajoongangdaily.joins.com/news/2025-12-22/opinion/columns/No-energy-security-no-national-future/2482816

- 아시아경제: 홍석표 사장 승계자금: https://www.asiae.co.kr/article/2022020621440312157&mobile=Y

- KRX 공시: 최대주주변경: https://kind.krx.co.kr/common/disclsviewer.do?method=searchInitInfo&acptNo=20220126000579&docno=

- LCWS 2024: cavity materials: https://agenda.linearcollider.org/event/10134/contributions/54583/attachments/39657/62617/LCWS_2024_10_JUL__Han.pdf

- Intel Market Research: Steel Wire Rope Market: https://www.intelmarketresearch.com/steel-wire-rope-market-13592

- Google Drive: 핵융합 에너지 브리핑: https://drive.google.com/open?id=1gTSfITT-2ILX5ljzf95W5ZOPU88dQ2MksJ2Zp2BdZ4E

- GlobeNewswire: Fusion forecast 2025-2045: https://www.globenewswire.com/news-release/2025/04/30/3071147/28124/en/Nuclear-Fusion-Energy-Industry-Forecast-2025-2045-Unprecedented-Private-Capital-Technological-Breakthroughs-and-Climate-Urgency-are-Accelerating-Development-Timelines.html

- Business Wire: Fusion market report: https://www.businesswire.com/news/home/20250506013448/en/Global-Nuclear-Fusion-Energy-Market-Report-2025-2045-Fusion-Energy-Sector-to-Reach-%2440-80-Billion-by-2035-and-Exceed-%24350-Billion-by-2050-if-Technological-Milestones-are-Achieved---ResearchAndMarkets.com

- Market Research Future: Superconducting Wire: https://www.marketresearchfuture.com/reports/superconducting-wire-market-7307

- MarketsandMarkets: Superconducting Wire: https://www.marketsandmarkets.com/Market-Reports/superconducting-wire-market-226116096.html

- Technavio: Superconductor Market: https://www.technavio.com/report/superconductor-market-industry-analysis

- KAT: R&D: https://www.kiswire-kat.com/sub06

- ITER Newsline: https://www.iter.org/print/whatsnew/39

- DTT: KAT superconducting strands: https://www.dtt-project.it/index.php/news-events/dtt-partners-with-kat-for-the-production-of-superconducting-strands-for-the-central-solenoid-and-pf1-magnet.html

- 페로타임즈: KAT 300억 출자: https://www.ferrotimes.com/news/articleView.html?idxno=39866

- Google Drive: 인애이블퓨전 분석: https://drive.google.com/open?id=1yOpBdIb1i1huQn_9n_x8qdjyr6_J66wc-ifWkFKYYQk

- 딜사이트: AI 전력 소모 해결책 핵융합: https://dealsite.co.kr/articles/121089/025087

- EnableFusion Inc.: https://www.enablefusion.com/

- ITER: commercial fusion reactors: https://www.iter.org/node/20687/glimpse-future-commercial-fusion-reactors

- EnableFusion K-PPP: https://www.enablefusion.com/k-ppp

- Stock Analysis: Kiswire Revenue: https://stockanalysis.com/quote/krx/002240/revenue/

- 주달: 고려제강 투자분석 2025.12.21: https://www.judal.co.kr/?view=stockAI&shareToken=OwHRq8RQUcXXHaX8

- 주달: 고려제강 투자분석 2025.12.13: https://www.judal.co.kr/?view=stockAI&shareToken=6HnqcGwVayG2Ubyx

- 주달: 만호제강 투자분석: https://www.judal.co.kr/?view=stockAI&shareToken=LfbktzYBrMNiQU8U

- KRX: 기업지배구조 보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250529000239&docno=&viewerhost=&

- Simply Wall St: Kiswire: https://simplywall.st/stocks/kr/materials/kose-a002240/kiswire-shares