DEEP RESEARCH · DNF

DNF: A Precursor Platform in the Soulbrain-Samsung Triangle

A review of High-k, DPT, HCDS, hybrid bonding, and the Q3 2025 turnaround challenge.

0. Bottom line first

DNF carries the near-term burden of a Q3 2025 loss, but after Soulbrain's acquisition, raw materials, IP, and customer channels are combining in a way that could re-rate DNF as a next-generation ALD precursor platform. The key is whether 2026 HBM4, GAA, 3D DRAM, and high-layer V-NAND convert into actual mass-production material revenue.

1. Technology moat: precursor portfolio

DNF's core products are precursors for semiconductor deposition. The source frames High-k, DPT, and HCDS as the main technology pillars.

Cp-Zr family

Linked to demand for thin and uniform high-k films in DRAM capacitors and GAA processes.

DIPAS

Presented as a sacrificial-film material for fine patterns and a moat that survived the EUV era.

Low-temperature SiO/SiN

Targets low-temperature deposition demand in 300- and 400-layer V-NAND.

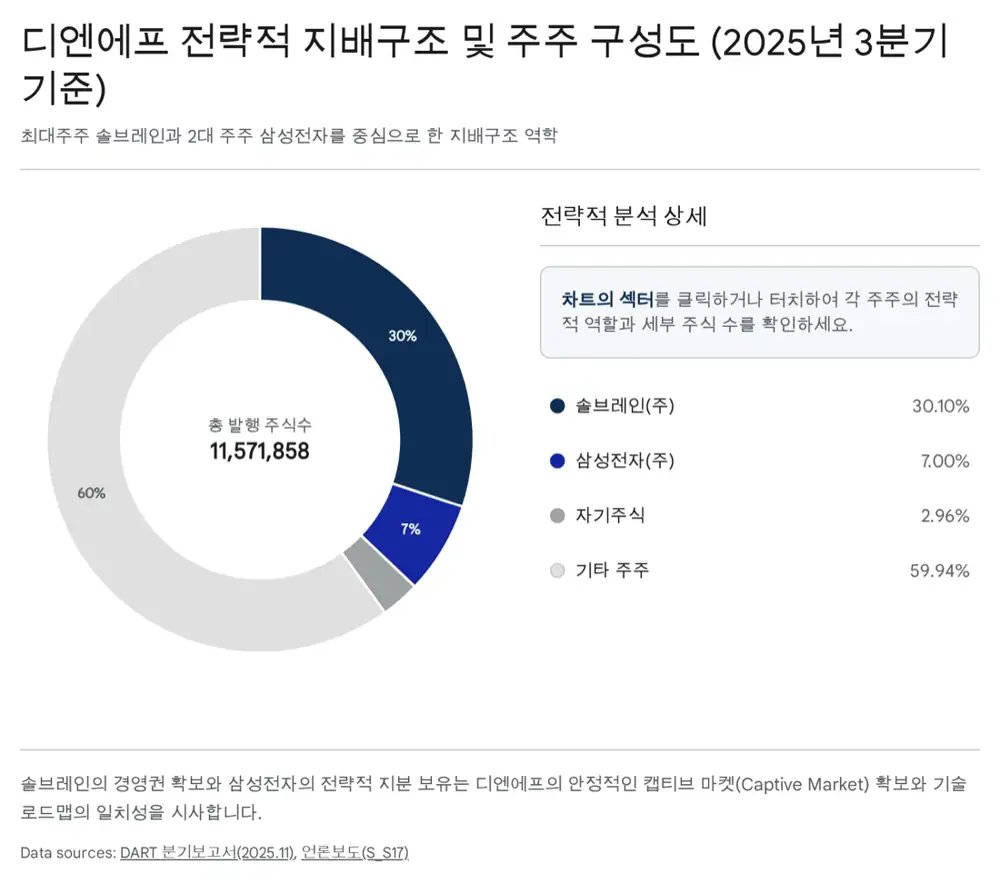

2. Relational moat: Samsung JDP and Soulbrain

The source views DNF's long history of joint development programs with Samsung Electronics as its strongest intangible asset. The mid-2000s Alpis-3 development and Samsung quality certification are presented as the starting point of customer trust.

3. Q3 2025: losses, but R&D maintained

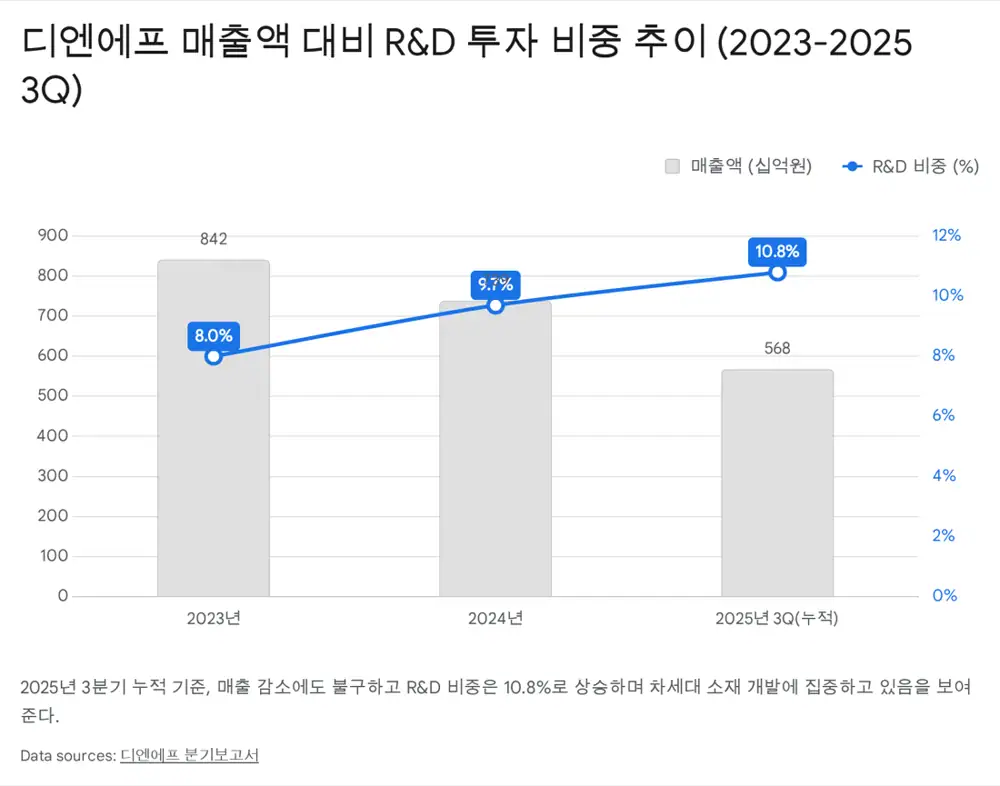

Official fact: The source reports Q3 2025 cumulative revenue of KRW 56.77bn, operating loss of KRW 2.74bn, and net loss of KRW 2.52bn.

| Item | Source figure | Meaning |

|---|---|---|

| Semiconductor materials | KRW 53.3bn, 93.86% | Main revenue base |

| Other | KRW 3.5bn, 6.14% | Pilot products such as next High-k, Low-k, and metal precursors |

| R&D | About KRW 6.1bn, 10.8% of revenue | Technology investment continued despite losses |

| CAPEX | About KRW 3.96bn | Manufacturing improvement and research equipment |

| Cash equivalents | KRW 12.1bn | Limited liquidity risk |

Interpretation: Current weakness is heavily affected by delayed semiconductor recovery and customer inventory policy. But pilot revenue in “other” can be read as a leading indicator of next-material tests.

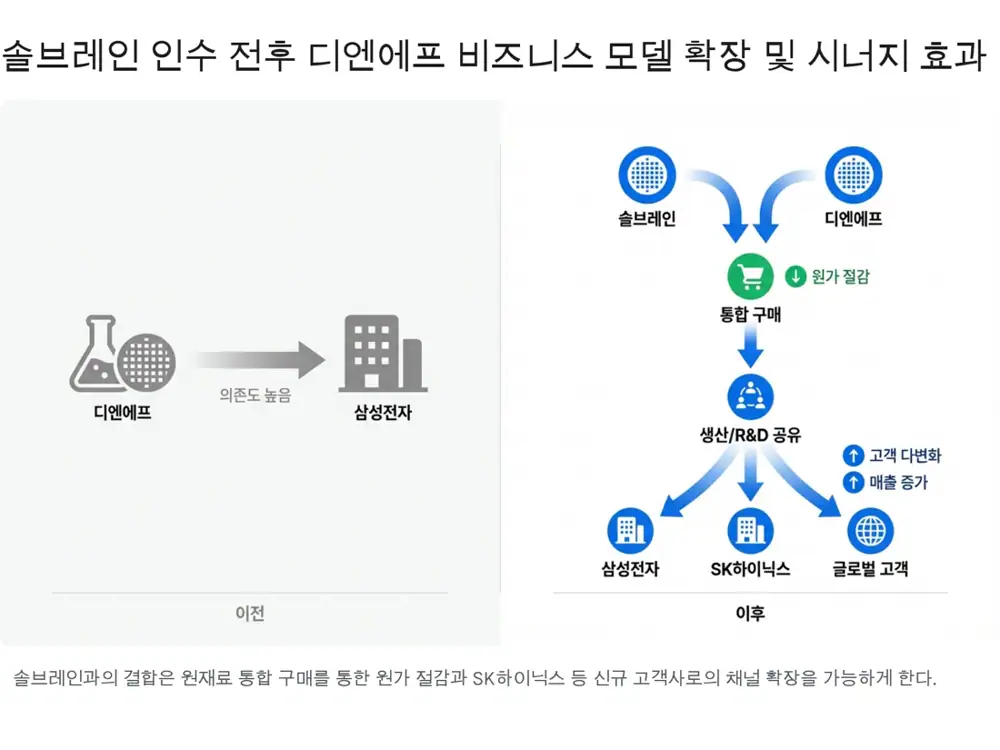

4. Soulbrain synergy

- R&D/IP: Soulbrain's source technology for High-k raw materials and DNF's synthesis and purification capabilities vertically integrate the precursor value chain.

- Buying power: joint purchasing of zirconium, hafnium, silicon, and other raw materials can improve cost competitiveness.

- Test infrastructure: access to 300mm wafer test infrastructure can reduce development delays.

- Customer expansion: Soulbrain's SK hynix network can reduce DNF's Samsung concentration risk.

5. 2026 roadmap

- HBM4/hybrid bonding: high-performance insulating-film materials are needed for direct copper-to-copper bonding.

- GAA: below 3nm, High-k insulating-film quality becomes a key to yield stability.

- 3D DRAM: vertical cell stacking can increase ALD precursor usage.

- V-NAND: 300-plus-layer scaling increases demand for low-temperature SiO/SiN precursor HCDS.

- OLED materials: low-temperature encapsulation and TFT High-k materials can transfer semiconductor know-how into displays.

6. Conclusion and risks

My conclusion is that DNF is in a run-up phase toward a higher position in the value chain. Risks include delayed IT-set demand recovery, customer price-reduction pressure, and delayed approval for next-generation materials. Conversely, if 2026 AI memory and hybrid-bonding localization becomes revenue, DNF could be revalued from a simple materials supplier into a Tech Enabler.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224125395397

- Source 2: https://plus.hankyung.com/apps/newsinside.view?aid=2023080982571&category=&sns=y

- Source 3: https://www.career.co.kr/board/Board_View.asp?brdSeq=161013&page=1&gubun=1

- Source 4: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250814003210&docno=&viewerhost=&

- Source 5: https://v.daum.net/v/20250722180619043

- Source 6: https://www.asiatoday.co.kr/kn/view.php?key=20200121010011822

- Source 7: https://www.etoday.co.kr/news/view/1847532

- Source 8: https://v.daum.net/v/20230809180302563?f=p

- Source 9: https://www.career.co.kr/board/Board_View.asp?brdSeq=158097&page=1&gubun=1

- Source 10: https://www.kedglobal.com/mergers-acquisitions/newsView/ked202308090019

- Source 11: https://plus.hankyung.com/apps/newsinside.view?aid=202402155851a&category=&sns=y

- Source 12: https://www.etnews.com/20231030000367

- Source 13: https://drive.google.com/open?id=1UpwSZmuR7zMAHnkO1EVijxH3gnkNMFufdrLrrM69j8E

- Source 14: https://biz.chosun.com/it-science/ict/2024/01/09/TNICLWD55FGSDA7Y3GYIT4EGXE/

- Source 15: http://sbox.thinkpool.com/bbs/read/s_pub.do?sn=471702&bbsSn=1010316&dbName=s_pub&code=&slt=&key=

- Source 16: https://kr.economy.ac/news/2025/05/20250546402

- Source 17: https://www.youtube.com/watch?v=MGQxNJIHFCs

- Source 18: https://ssl.pstatic.net/imgstock/upload/research/industry/1680498424053.pdf

- Source 19: https://www.theise.org/wp-content/uploads/2025/12/%EB%B0%98%EB%8F%84%EC%B2%B4%EA%B3%B5%ED%95%99%ED%9A%8C-%EB%B0%98%EB%8F%84%EC%B2%B4%EA%B8%B0%EC%88%A0%EB%A1%9C%EB%93%9C%EB%A7%B52026.pdf