DEEP RESEARCH · LOT VACUUM

LOT Vacuum: Samsung’s Strategic Stake, Dry Pump Localization, and the Turnaround Roadmap

A semiconductor-equipment view focused on HBM, GAA, service integration, and operating leverage after the downcycle

0. Bottom line first

Despite the 2025 loss, I do not read LOT Vacuum as structurally impaired. The key questions are whether its domestic dry-vacuum-pump position, Samsung Electronics’ 7.12% stake, and the August 2025 merger of LOT TS translate into leverage during the 2026 upcycle.

1. Technology roots

Official fact: LOT Vacuum was founded on March 23, 2002, acquired the Pittsburgh dry-pump business of Oerlikon Leybold Vacuum in June 2002, and listed on KOSDAQ on October 5, 2005.

Interpretation: The company’s advantage is not just the slogan of localization. It began with source technology, manufacturing know-how, and proven product lines such as Dura Dry.

2. Strategic alliance with Samsung

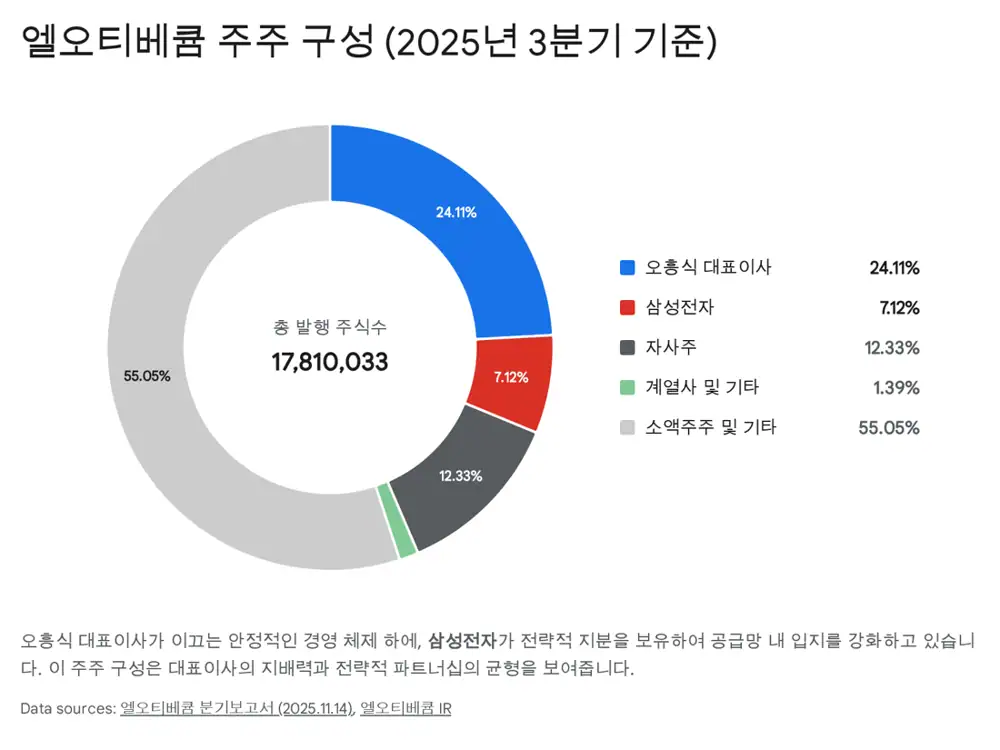

Official fact: In November 2020, LOT Vacuum raised about KRW 19.0bn from Samsung Electronics through a third-party allotment. As of September 30, 2025, Samsung is shown as holding 1,267,668 shares, or 7.12%.

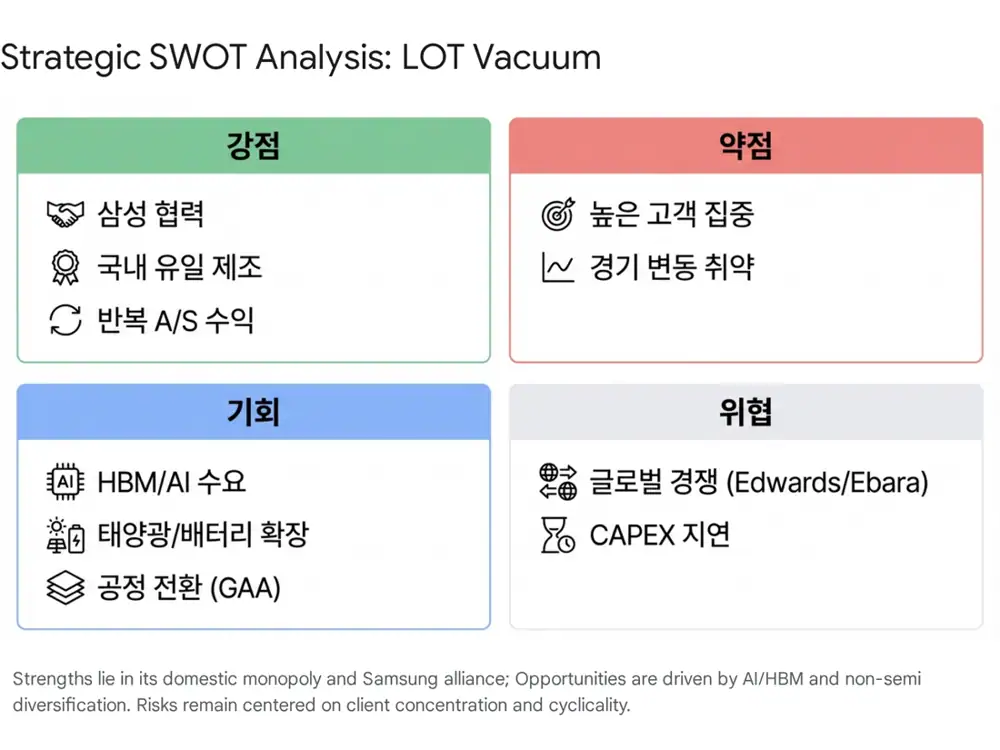

Interpretation: This stake creates a supply-chain lock-in effect. After Japan’s export controls, localization of critical materials, parts, and equipment became strategic, and vacuum pumps are line-availability infrastructure.

Oh Heung-sik

An engineer-manager with Leybold Korea experience. The source lists 24.11%, or 4,294,105 shares.

Samsung Electronics

A 7.12% shareholder. The source estimates Samsung-related revenue at about 77% as of 2025 3Q.

Treasury shares

The 12.33% treasury share ratio may support cancellation or strategic exchanges.

3. Business model and moat

Dry vacuum pumps evacuate gases from semiconductor chambers and remove toxic gases and process byproducts. LOT combines equipment sales with maintenance and overhaul services. Absorbing the wholly owned LOT TS on August 1, 2025 integrated manufacturing and service.

Interpretation: Field failure and wear data feeding back into R&D matters for high-end pumps. HBM TSV etch, sub-3nm GAA, and ALD raise the value of corrosion resistance, thermal control, and byproduct handling.

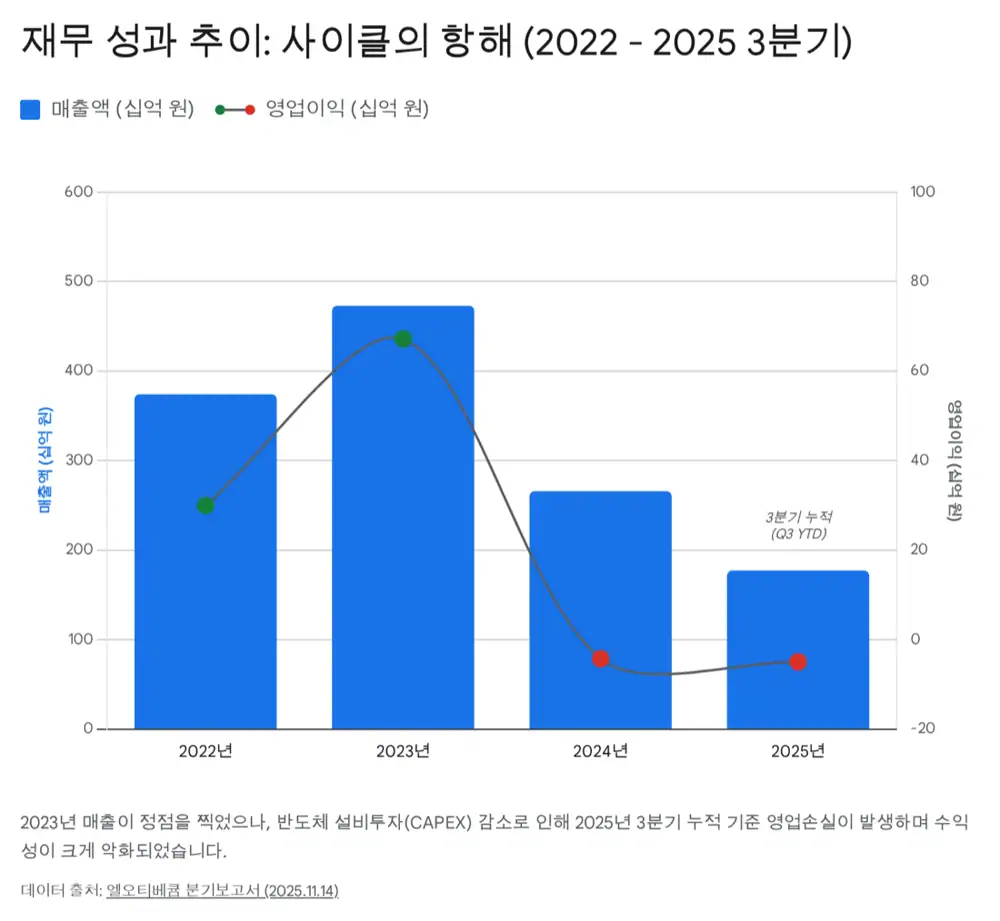

4. 2025 trough and balance sheet

| Item | Source figure | Read-through |

|---|---|---|

| 2025 3Q cumulative revenue | KRW 177.36bn | Down year on year |

| Operating profit | -KRW 4.88bn | Turned to loss |

| Net income | -KRW 5.53bn | Turned to loss |

| R&D expense | About KRW 9.2bn | More than 5% of revenue |

| Cash-like assets | About KRW 88.2bn | KRW 80.0bn cash plus KRW 8.2bn short-term financial assets |

| Debt ratio | About 30% | Liabilities KRW 74.6bn, equity KRW 246.0bn |

| Credit rating | A-, cash-flow grade B | eCredible, September 2025 |

5. 2026 upturn points

- HBM expansion: TSV processes require deep, precise etching and high-performance pumps.

- GAA: Sub-3nm ALD and etch complexity can lift high-end pump ASP.

- Non-semiconductor: solar TOPCon/HJT lines and battery drying/degassing are additional demand areas.

- Merger effect: LOT TS integration can reduce cost and improve service-data-driven R&D.

Official fact: The source expects revenue could recover to the 2022-2023 range of KRW 300bn-400bn if Samsung’s Pyeongtaek P4/P5 and Taylor fab equipment move-in accelerates in 2026.

6. Risks

- Samsung exposure above 70% is a double-edged sword.

- Global competitors such as Edwards and Chinese local players remain threats.

- Quarterly orders must confirm whether 2025 was a cyclical trough or demand erosion.

Sources

- 서울경제TV: 국내 유일 반도체 진공펌프 기업: https://www.sentv.co.kr/article/view/sentv202011020044

- 매일경제: 삼성전자 190억 유상증자: https://www.mk.co.kr/news/stock/9588086

- 서울경제: 오흥식 엘오티베큠 사장: https://www.sedaily.com/NewsView/1HSJIHT9AI

- 나무위키: 엘오티베큠: https://namu.wiki/w/%EC%97%98%EC%98%A4%ED%8B%B0%EB%B2%A0%ED%81%A0

- Busch: Dry Vacuum Technology: https://www.buschvacuum.com/us/en/success-stories/dry-vacuum-technology-for-chemical-and-pharmaceutical-processes.html

- AIChE: Vacuum Technology: https://www.aiche.org/resources/publications/cep/2025/august/vacuum-technology-chemical-and-pharmaceutical-processes

- 파이낸셜뉴스: 진공펌프 특허 취득: https://www.fnnews.com/news/200909241156080372

- 프라임경제: 복합건식진공펌프 특허: https://m.newsprime.co.kr/section_view.html?no=135529