DEEP RESEARCH · YEST/HPA/HBM EQUIPMENT

YEST: Structural Opportunity in High-Pressure Hydrogen Annealing and HBM Process Transition

A combined review of the HPSP patent dispute, high-pressure hydrogen annealing, HBM pressure curing, and the Q·P·C framework.

0. Bottom line first

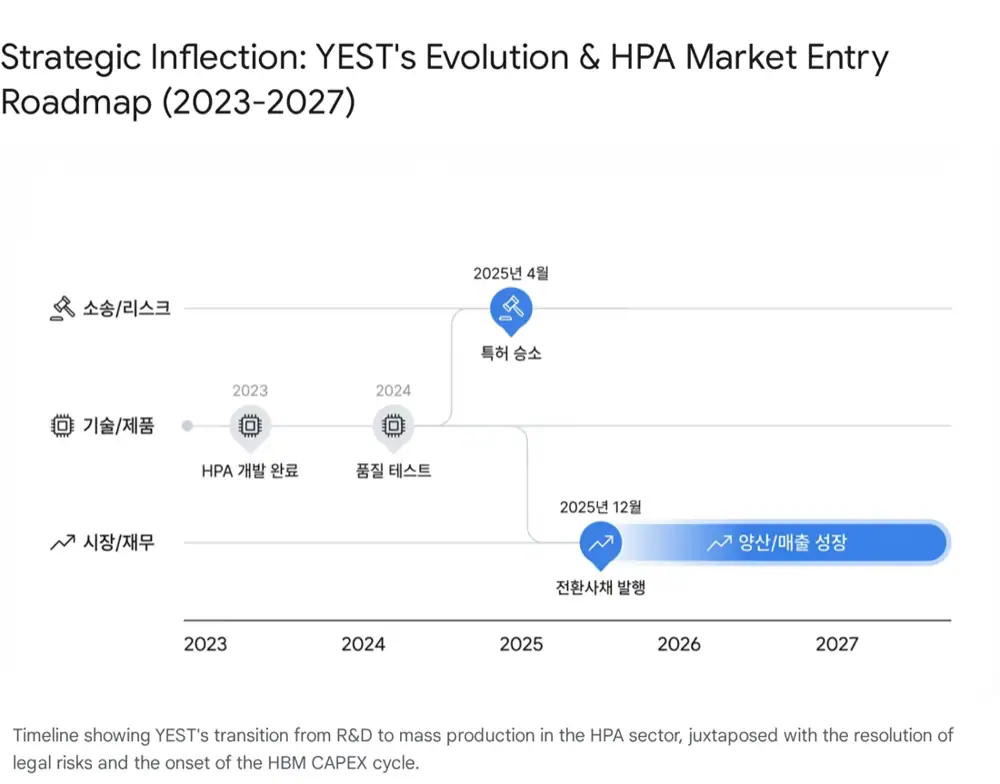

YEST’s core story is that the April 2025 negative scope confirmation win materially reduced legal uncertainty around HPA, while HBM, GAA, and high-layer 3D NAND processes are opening demand for both high-pressure hydrogen annealing and pressure-curing equipment.

Official fact: The source cites SMIC Research and also provides a Naver-attached PDF.

April 2025 non-infringement view

The patent tribunal distinguished YEST’s rotary locking mechanism and internal chamber structure from HPSP’s claims.

20~30 atm process

Pressure substitutes for heat, allowing hydrogen to penetrate deeply and passivate defects below 400°C.

2026 big cycle

The source forecasts revenue of KRW 101.3B in 2025, KRW 145.3B in 2026, and KRW 172.1B in 2027.

1. 2025 inflection: legal uncertainty down, growth visibility up

In 2025, semiconductor capital equipment is split between the traditional silicon cycle and the AI supercycle. YEST used to be viewed as a display-equipment and legacy thermal-processing supplier, but it is being re-rated through entry into HPSP’s de facto high-pressure annealing market and expansion of pressure-curing equipment for HBM manufacturing.

Interpretation: I frame YEST’s second-half 2025 story as “uncertainty removal” plus “visible growth.” The April negative scope confirmation win gave customers justification to consider YEST as a second vendor, and the commercial meaning of that decision remains despite mixed invalidation-trial outcomes in October.

2. HPSP dispute: commercial meaning of patent risk

Official fact: The HPA market’s entry barrier was not only handling high-pressure hydrogen gas, but also maintaining more than 25 bar below 450°C while controlling explosion risk. HPSP’s Patent No. 1553027 covers high-pressure chamber opening/closing and safety interlock systems and had functioned as a barrier to late entrants.

In 2023, after YEST disclosed its own HPA equipment and began qualification testing with major IDMs, HPSP filed a patent-infringement injunction suit. The source interprets this as a strategic move to defend a monopoly position with operating margins above 50%.

| Legal track | 2025 result | Meaning |

|---|---|---|

| Negative scope confirmation | YEST win in April 2025 | Rotary locking and internal chamber structure were distinguished from HPSP’s pin-based fastening and safety device claims |

| Invalidation trial | Partial rejection/dismissal in October 2025 | HPSP’s patent was not invalidated, but the source sees limited impact on YEST equipment sales |

| Commercial effect | Injunction risk materially reduced | Customers can consider second-vendor designation with less legal burden |

Interpretation: The legal win matters more for customer purchasing than for the share multiple alone. Customers such as Samsung Electronics and SK Hynix are reluctant to place disputed equipment into production lines. A non-infringement view lowers the psychological barrier from qualification to order.

3. HPA technology: solving the scaling paradox with pressure

In sub-10nm logic, 200-plus-layer 3D NAND, and 1c-nm DRAM, the key challenge is thermal budget. Advanced structures such as GAA and high-k metal gate are vulnerable to temperatures above 450°C, but hydrogen annealing is needed to repair silicon-interface defects.

Official fact: High-pressure hydrogen annealing uses pressure as a substitute for temperature. Raising hydrogen or deuterium gas pressure to 20~30 atm allows hydrogen atoms to penetrate deeply and passivate defects below 400°C.

125 wafers per batch

The source says this is about 67% higher than the competitor’s standard 75-wafer specification and lowers cost of ownership.

Up to 900°C heat resistance

Supports future high-temperature applications beyond current low-temperature annealing.

Up to 30 bar

Provides more process margin than standard 25-bar equipment and improves penetration in high-aspect-ratio 3D structures.

Direct heating/cooling

Direct gas heating and chiller circulation can improve ramp-up, cool-down, and temperature uniformity.

YEST’s strategic weapon is in-house pressure-vessel manufacturing. Know-how accumulated in display equipment and component sourcing through affiliates can shorten lead times, enable customized chamber specifications, reduce BOM cost, and improve pricing competitiveness.

4. End markets: HBM, GAA, and high-layer 3D NAND

Official fact: HBM stacks multiple DRAM dies vertically and connects them through TSVs. To control warpage during wafer thinning and stacking, pressure-curing equipment is used to cure underfill material with uniform heat and pressure.

Interpretation: If HPA is the future growth engine, pressure curing, chillers, and furnaces have been the cash cows supporting 2024~2025 results. YEST’s role in Samsung’s HBM line and expansion into SK Hynix’s supply chain matter because they start customer diversification.

| End process | Demand logic | YEST opportunity |

|---|---|---|

| HBM | AI demand expands stacked DRAM and pressure-curing needs | TC-NCF support plus chiller, furnace, and pressure-cure supply |

| GAA 3nm/2nm | Interface-trap removal deep in 3D nanosheet structures | High-pressure hydrogen process can support advanced logic yield stability |

| 3D NAND 300~400+ layers | Higher channel-hole aspect ratios make uniform annealing difficult | 30-bar pressure technology can improve penetration into deep structures |

5. Earnings outlook: Q, P, C framework

| Axis | Source outlook | Key variable |

|---|---|---|

| Q: volume | Estimated KRW 101.3B revenue in 2025, KRW 145.3B in 2026 (+43% YoY), KRW 172.1B in 2027 | Samsung/SK Hynix HBM capacity, 1c-nm DRAM, V9 NAND transition, and HPA production orders |

| P: price | Estimated ASP around KRW 4.0B for foundry HPA and KRW 4.5B for memory HPA | ASP improvement from higher HPA and pressure-curing mix |

| C: cost | OPM forecast: about 7% in 2025 → 18.5% in 2026 → 26.7% in 2027 | Pressure-vessel internalization and fixed-cost leverage after R&D/legal expenses |

Official fact: The source says the KRW 15.4B exchangeable bond issued in December 2025 will be used to expand production facilities. It interprets this as a signal of preparation for large production orders.

Interpretation: To secure a 30~40% target share in a market previously dominated by HPSP, YEST needs repeated orders inside customer dual-vendor policies, not just technical validation. More important than revenue growth is whether the high-margin HPA mix actually rises enough to sustain 20%-plus operating margins.

6. Customer expansion strategy

Anchor partner

The source cites HPA for GAA yield stabilization, pressure curing for HBM TC-NCF, and collaboration across furnaces, chillers, and NEOCON.

HBM alliance expansion

Government HPA localization project experience and HBM infrastructure equipment supply can support early adoption.

Kioxia/WD

Japanese fabs value high-throughput 125-wafer batch tools, and the source sees opportunity because HPSP lacks related HPA patents in Japan.

Micron/Intel

These are presented as customers looking for alternatives to HPSP amid supply-chain diversification and HBM competitiveness needs.

7. Conclusion and checkpoints

YEST is framed as both a turnaround and structural-growth company. In 2023~2024, HPA development and litigation costs weighed on fixed costs, but from 2026 onward, higher revenue volume could amplify operating leverage.

- Legal risk: the April 2025 negative scope confirmation win gave customers a clearer reason to order.

- Structural growth: YEST supplies critical equipment to both HBM and advanced processes such as GAA/3D NAND.

- Financial leverage: the source assumes HPA mix can lift OPM from the 7% range to the 26% range.

- Execution signal: the KRW 15.4B EB issuance and facility-investment purpose are read as preparation for production orders.

Interpretation: The issue now moves from courtrooms to global fab production lines. Technical validation, reduced legal uncertainty, and cycle timing are in place; the remaining evidence must come from orders, delivery, and margin.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224125100271

- SMIC Research: http://snusmic.com/research/

- Attached PDF: 25_2_4주차_수정보고서_3팀_예스티_251228_092752.pdf

- YES COMPANY NEWS: https://yest.co.kr/Jsource/Jboard/content.asp?ji_num=9&jb_idx=42