DEEP RESEARCH · NEOOTO/212560

NeoOto (212560): Where the Hybrid Supercycle Meets EV Reduction Gears

A review of how hybrid production growth, EV reduction gears, and the Yesan Plant 4 expansion could reshape earnings and valuation.

0. Bottom line first

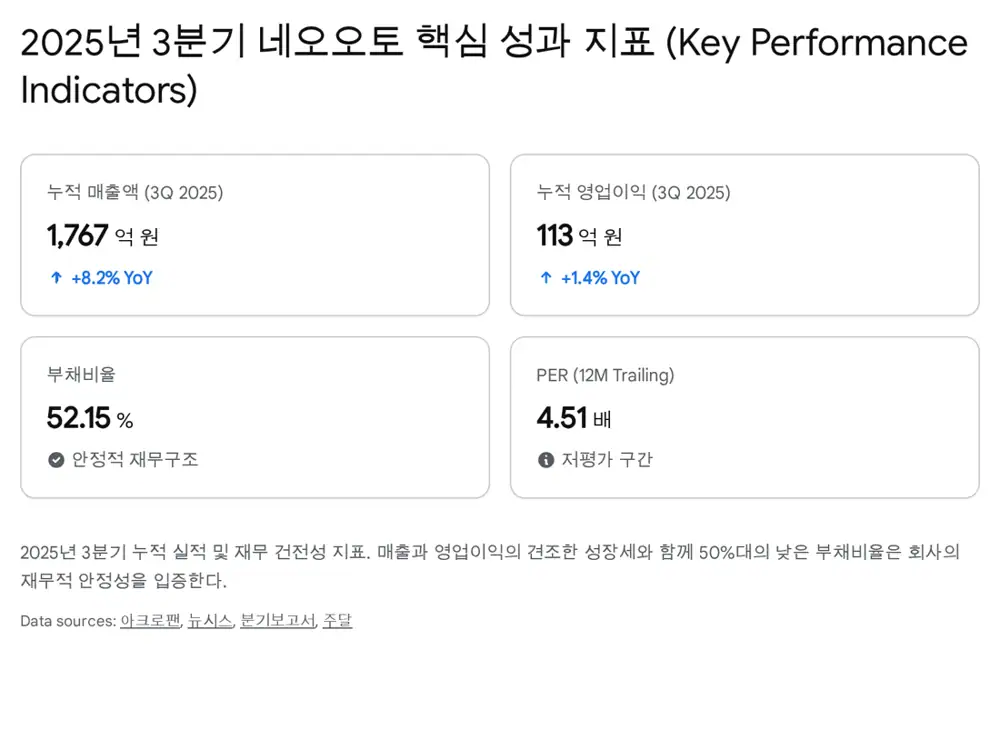

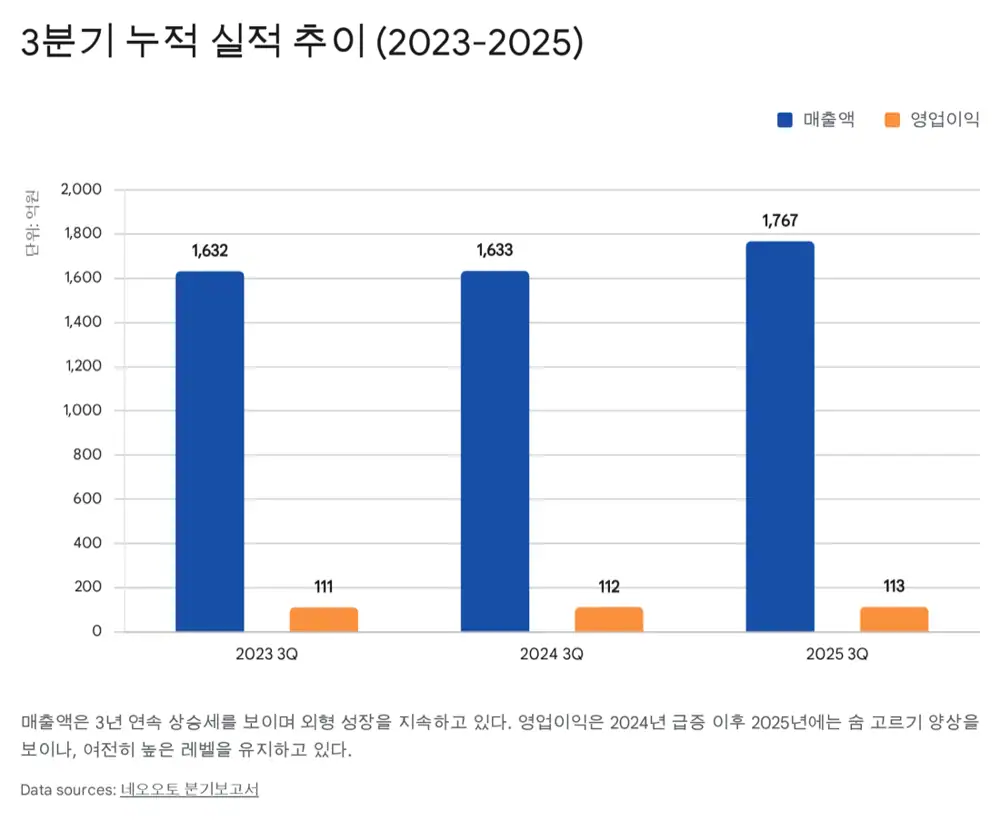

My core view on NeoOto is the gap between the market’s “legacy internal-combustion parts supplier” discount and the company’s actual business mix. In the source, cumulative Q3 2025 revenue was KRW 176.7B and operating profit was KRW 11.3B, up 8.2% and 1.4% YoY, while hybrid transmission gears and EV reduction gears are both creating demand.

Hybrid re-rating

After the EV chasm, Hyundai Motor Group’s hybrid production push supports demand for pinion gears, large gears, and differential assemblies.

Reduction-gear upside

EVs may not need multi-speed ICE transmissions, but they do need reduction gears to convert motor speed into wheel torque. The source highlights E-GMP supply and next-generation eM development participation.

Yesan Plant 4

The roughly 5,000-pyeong fourth plant is presented as a 2026 growth trigger with up to KRW 94B in annual incremental revenue potential.

1. Corporate structure and edge

Official fact: NeoOto was established on January 6, 2010 through the physical split-off of Auto Industry’s transmission gear manufacturing business and listed on KOSDAQ on November 18, 2015. It established a Mexico entity in 2016 and an India entity in 2018 to follow customer overseas production expansion.

Official fact: As of Q3 2025, NeoOto is run by co-CEOs Hyun-cheol Jung and Sun-hyun Kim. The source states that Kim and related parties own 51.2%, and describes an affiliate network that includes Auto Industry, Neo Steel, OTO VINA, OTO CZECH, OTO AUTOTECH INDIA, and GLOBAL OTO across procurement, processing, and overseas supply.

Interpretation: NeoOto’s edge is not simply “making gears”; it is making ultra-precision gears at consistent mass-production quality. Transmission gears face thousands to tens of thousands of RPM and high torque, so tiny dimensional errors can become NVH and durability issues. Automated complex-dimension inspection, shaving/honing, and in-house heat treatment are therefore central.

2. Market shift: EV chasm, HEV comeback, reduction-gear growth

The source attributes the hybrid comeback to the EV chasm that began in 2024, charging-infrastructure gaps, high vehicle prices, battery-fire concerns, and subsidy reductions. Hybrids still require 6-speed or 8-speed automatic transmissions and precision gears to coordinate engine and motor power.

Official fact: The source places NeoOto’s sales dependence on Hyundai Transys at about 76.8%. It treats this as both customer-concentration risk and a moat backed by Hyundai Motor Group’s global Top 3 sales position, joint R&D, and strict quality standards.

Interpretation: The old worry was that a rapid BEV transition would reduce gear demand. But if the actual bridge is a longer hybrid cycle, NeoOto gets more time. And because EVs need reduction gears, the part is better understood as changing role rather than disappearing.

3. Product portfolio and Plant 4 expansion

| Product | Source metric | Investment point |

|---|---|---|

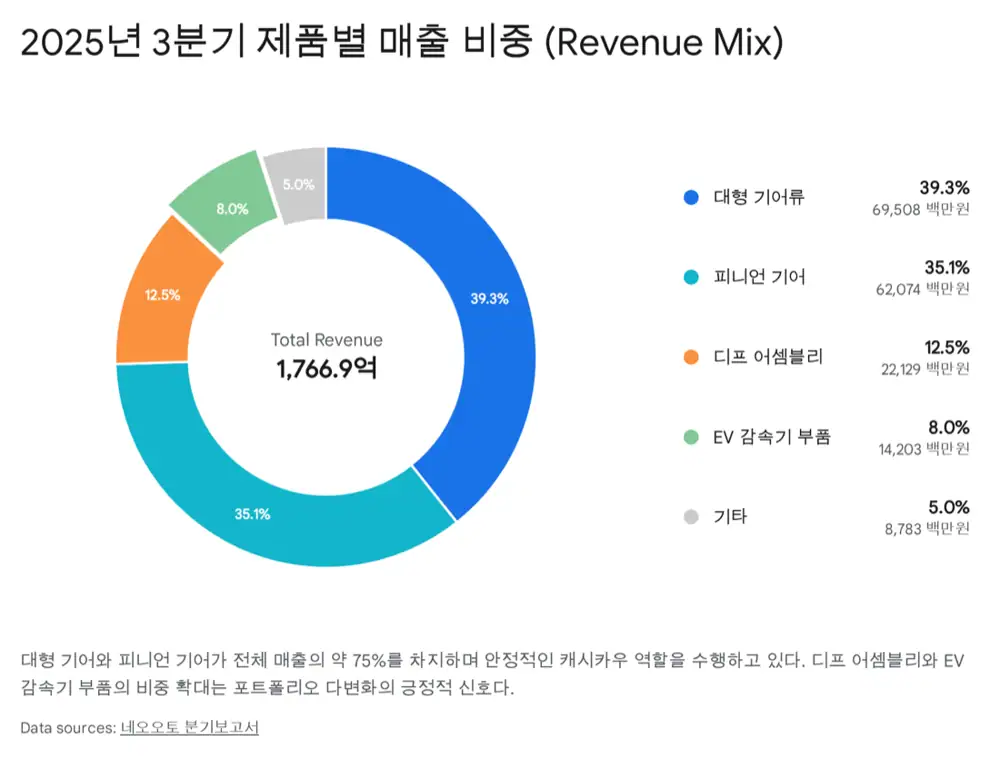

| Large gears | KRW 69.5B cumulative Q3 2025 revenue; about 40% of total sales | Main product family that transfers engine power inside automatic transmissions |

| Pinion gears | KRW 62.0B cumulative Q3 revenue | High-precision planetary gear component with durability and qualification barriers |

| Differential assembly | KRW 22.1B cumulative Q3 revenue | Rising need to withstand high EV torque |

| EV reduction gear parts | KRW 14.2B cumulative Q3 revenue; about 8% of total sales | Growth option tied to Ioniq, EV6, EV9, and broader electrification |

Official fact: Yesan Plant 4 is described as roughly 16,505㎡ of land, or 5,000 pyeong, and 7,452㎡ of building area, or 2,254 pyeong. The source states an October 2025 completion target, full-scale operation in 2026, about KRW 94B in potential annual incremental revenue at full utilization, and a scale equal to about 43% of 2024 revenue of KRW 217.9B.

Interpretation: Plant 4 matters because it is not just capacity. It is positioned for next-generation hybrid transmissions such as TMED-II and EV reduction gears. It is the bridge from a KRW 200B revenue company toward a KRW 300B-plus specialist.

4. R&D and the move toward ODM

Two-speed EV transmission

The source states that NeoOto is developing this through a government project and validating durability and performance in vehicle tests.

Reducer with parking system

A niche portfolio item developed and under validation for ultra-compact EVs and commercial vehicles.

Heavy commercial e-axle

The source says NeoOto is jointly developing an integrated motor, reducer, and inverter drive module for commercial vehicles above 8 tons with Hyundai Transys.

What I watch most is the potential shift from OEM to ODM. If NeoOto moves from build-to-print parts to customer-facing design and system proposals, the valuation framework can change.

5. Financials and valuation

| Item | Source figure | Read-through |

|---|---|---|

| Q3 2025 cumulative revenue | KRW 176.7B, +8.2% YoY | Hybrid sales and component volume were the main drivers |

| Operating profit | KRW 11.3B, +1.4% YoY; operating margin about 6.4% | Above the 3~4% auto-parts average despite Plant 4 start-up costs, labor, and R&D |

| Net income | KRW 12.7B | Positive non-operating effects such as FX translation and financial income helped |

| Financial stability | Debt ratio 52.15%, current assets KRW 91.4B, cash equivalents KRW 24.8B | Near debt-free stability for a capital-intensive manufacturer |

| Capital events | KRW 9B CB in Feb. 2024; 0.5 bonus share per share in July 2025; capital KRW 3.9B→KRW 5.9B | Funding for facilities and improved trading liquidity |

Official fact: The source presents late-December 2025 market capitalization at roughly KRW 80~100B, PER at 4.5~5.5x, the KOSDAQ transportation equipment/parts average PER at 10~15x, and PBR at 0.6~0.74x. It also states an expected 2024 dividend of KRW 200 per share and an estimated 2025 dividend yield of roughly 2.5~3%.

Interpretation: The discount comes from Hyundai Motor Group concentration, a legacy-ICE image, and limited institutional flow due to small market cap. The offsetting catalysts are 2026 Plant 4 ramp-up, non-Hyundai customer wins such as Stellantis and Toyota, and commercialization of a two-speed EV transmission.

6. Risks and final view

| Risk | Source mitigation/offset |

|---|---|

| Hyundai Transys dependence above 70% | Customer diversification toward Stellantis and Toyota plus Mexico/India local supply routes |

| Uncertain EV transition speed | Hybrid and EV part lines plus flexible manufacturing systems |

| Special-steel and raw-material volatility | Raw-material price surcharge system with major customers |

The source’s scenario mentions a short-term three-month zone of KRW 6,500~7,000, a short-term target of KRW 9,200, and, over a one-year-plus horizon, the possibility of KRW 150~200B market capitalization and more than KRW 13,000 per share if Plant 4 drives 2026 growth and annual revenue moves beyond KRW 300B. I record this as the source’s investment scenario, not as a recommendation.

Interpretation: The checklist is straightforward: how long the hybrid cycle lasts, whether EV reduction-gear revenue becomes meaningful in the mix, and whether Plant 4 contributes visibly to 2026 numbers.

Sources

- Original post: Naver Blog original

- NeoOto Q3 2025 cumulative revenue report: https://kr.acrofan.com/detail.php?number=411141

- Newsis Q3 cumulative revenue report: https://mobile.newsis.com/view/NISX20251113_0003401566

- KRX annual report filing: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240321002192&docno=&viewerhost=&

- eMoneyNews fourth-plant expansion: http://m.emoneynews.co.kr/news/articleView.html?idxno=118732

- Wide Daily fourth-plant expansion: https://www.widedaily.com/news/articleView.html?idxno=263185

- Judal investment analysis, 2025.12.17: https://www.judal.co.kr/?view=stockAI&shareToken=wuylTO4ixp4elJTC

- NeoOto company news on plant expansion: https://neooto.kr/kr/sub/contact/news.php?mode=view&bid=2&idx=138

- FnGuide NeoOto snapshot: https://comp.fnguide.com/SVO2/ASP/SVD_Main.asp?pGB=1&gicode=A212560&cID=&MenuYn=Y&ReportGB=D&NewMenuID=Y&stkGb=701

- Judal investment analysis, 2025.12.25: https://www.judal.co.kr/?view=stockAI&shareToken=BKo56vi3Xod4SuHs

- KRX quarterly report filing: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240516001510&docno=&viewerhost=&