DEEP RESEARCH · ITCEN GLOBAL

ITCEN Global: The Re-rating Case Around RWA and Digital Finance Infrastructure

A research view that connects gold distribution, public/financial IT, and BDAN into one digital finance infrastructure holding company

0. Bottom line first

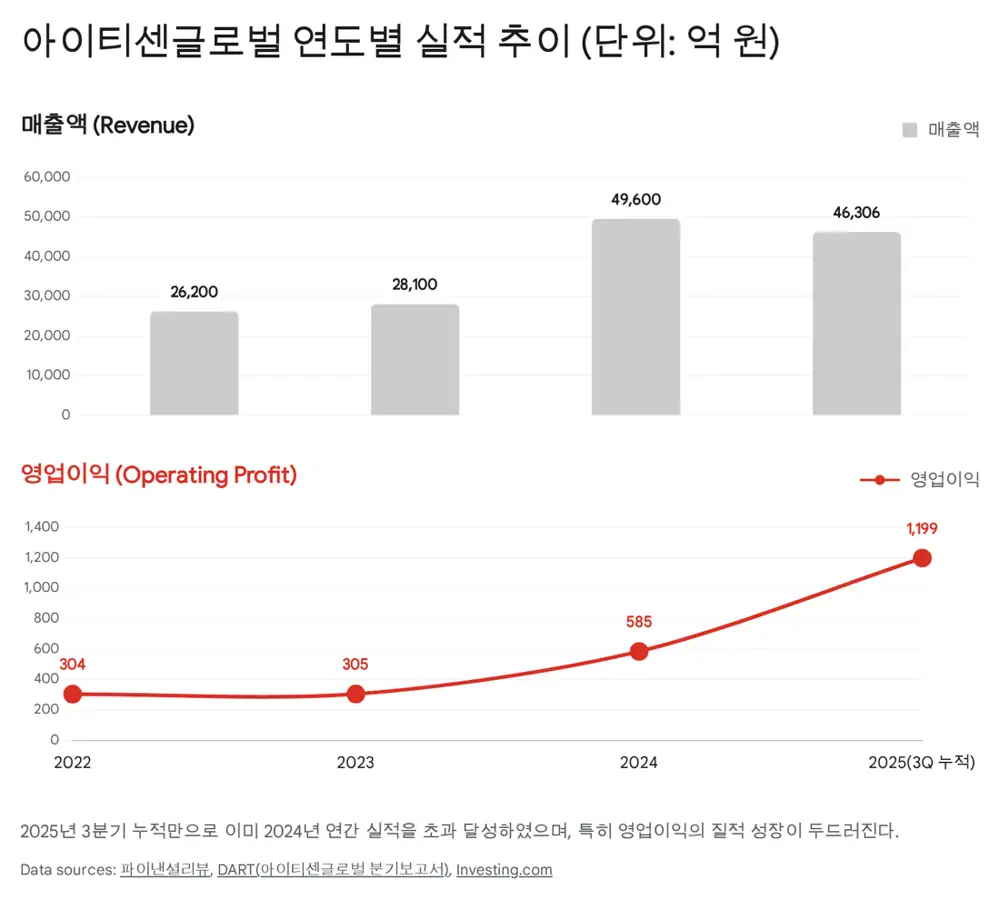

My core view is that ITCEN Global should no longer be read as a plain SI company. The source cites 2025 3Q cumulative consolidated revenue of KRW 4.6306 trillion and operating profit of KRW 119.9 billion, reflecting gold price leverage, IT-service improvement, and Web3/RWA optionality.

Korea Gold Exchange

Physical gold distribution and inventory effects can lift both revenue volume and margin.

IT service group

Public SI, network, cloud, and security capabilities provide the operating base for Web3 platforms.

BDAN

Busan Digital Asset Exchange and RWA tokenization are the key valuation options.

1. Redefining the company

Official fact: ITCEN Global started in public informatization, hardware resale, and maintenance, then expanded into software, cloud, and precious-metal distribution. The recent name change is framed as a move toward global Web3 markets.

Interpretation: I read the company less as a conventional IT-service vendor and more as a holding-style platform combining real-world assets with digital infrastructure.

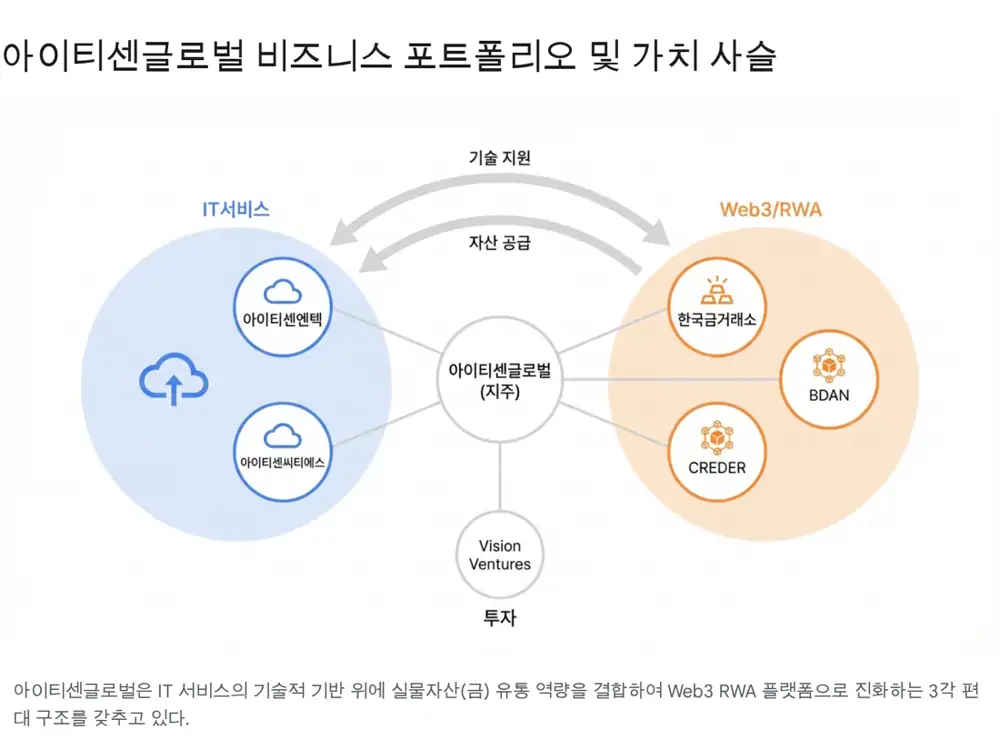

2. Group structure

The IT-service group covers network integration, public/defense/sports SI, biometric authentication, and security. The Web3 and precious-metal group centers on Korea Gold Exchange, Korea Gold Exchange Digital Asset, CREDER, and BPMG. Vision Ventures adds future options through AI semiconductor investments such as FuriosaAI.

Interpretation: Stability and growth are separated but complementary: gold cash flow funds Web3 investment, while IT affiliates provide the operating technology for exchange, wallet, and security layers.

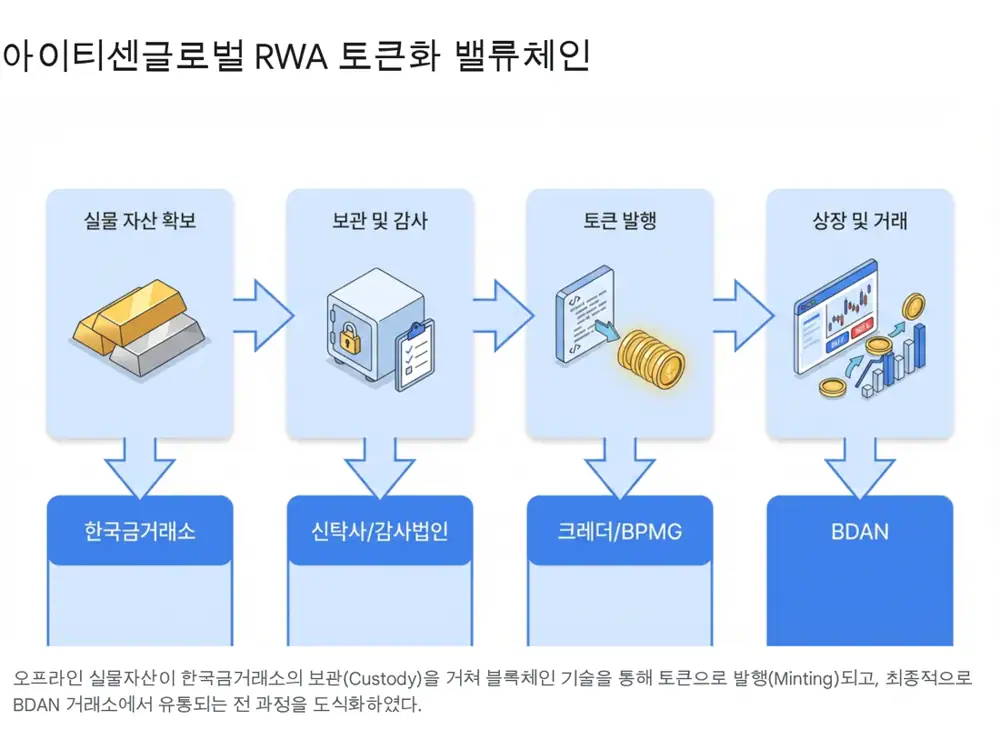

3. RWA and BDAN

Official fact: BDAN announced the Bidan brand in October 2024 and is described as expanding services from 2025. Unlike conventional crypto exchanges, it aims at digital products backed by real-world assets such as gold, silver, commodities, and cultural content.

Interpretation: The differentiator is that ITCEN already controls potential underlying assets for tokenization through the group.

4. Gold cycle and operating leverage

Gold price increases affect ITCEN through unit-price revenue expansion, inventory gains, and higher investment demand. The source attributes the 293% year-on-year jump in cumulative operating profit partly to this inventory effect.

Official fact: The source says Goldman Sachs presented a scenario in which gold could rise toward USD 4,900 per ounce by 2026.

5. IT services and financials

Behind gold and RWA, the IT-service business is moving toward cloud-native, MSP, SaaS, and AI infrastructure. The source gives IT services at about 16.35% of 2025 3Q revenue, while noting potential benefit from public-cloud migration and digital-platform-government policy.

| Item | Source figure | Read-through |

|---|---|---|

| 2025 3Q cumulative revenue | KRW 4.6306tn | Scale from gold distribution plus IT |

| 2025 3Q cumulative operating profit | KRW 119.9bn | Presented as +293% YoY |

| Total assets | KRW 1.2524tn | Current assets of KRW 922.4bn |

| Inventory | KRW 254.0bn | Up 117% from KRW 116.9bn at prior year-end |

| Market cap/PER | KRW 770.3bn, about 32x PER | Source figure as of 2025-12-24 |

6. Risks and checkpoints

- STO legislation delays could slow RWA expansion.

- A sharp gold-price decline could hurt inventory value and trading volume.

- Convertible bonds and other mezzanine instruments may create overhang.

- A 32x PER is demanding for a simple SI peer set, so Web3/RWA premium must become operating evidence.

Sources

- 파이낸셜리뷰: 3분기 누계 매출액 4조6306억: http://www.financialreview.co.kr/news/articleView.html?idxno=38282

- BNT뉴스: 금시세 27일: https://www.bntnews.co.kr/article/view/bnt202512270057

- LiteFinance: 금 가격 전망: https://www.litefinance.org/ko/blog/analysts-opinions/geum-gagyeog-jeonmang-yecheug/

- 머니S: STO 법안 법제화 본격화: https://www.moneys.co.kr/article/2025122411203680757

- 토스증권 뉴스: 예탁결제원 토큰증권 시스템: https://www.tossinvest.com/stocks/A016610/news?symbol-or-stock-code=A016610&contentType=news&contentParams=%7B%22id%22%3A%22ajukyung_20251210152344966%22%7D

- Daum: 비단주머니 청사진 공개: https://v.daum.net/v/20251222153608880

- KB의 생각: 아이티센 글로벌 주가전망: https://kbthink.com/securities-view.html?docId=20250429111016413K

- 부산일보: 부산디지털자산거래소 비단 공식 출범: https://www.busan.com/view/election/view.php?code=2024102814033657911

- Bloter: 금·은값 사상 최고치: https://www.bloter.net/news/articleView.html?idxno=650191

- 주달: 아이티센글로벌 투자분석: https://www.judal.co.kr/?view=stockAI&shareToken=XtkNSRgOracWwBHw

- Investing.com IN: ITCen P/E Ratio: https://in.investing.com/pro/KOSDAQ:A124500/explorer/pe_ltm